As affordability pressures rise, leaders are proposing the idea of ultra-long mortgages, including 50-year terms, to entice buyers. The pitch sounds intuitive: stretch the loan longer and lower the monthly payment. However, at today’s interest rates, the reduction in the monthly payment is marginal, and this strategy may be more of a debt trap than an affordability solution while pushing home prices to ever higher levels. The minimal short-term savings come with a long-term cost, which becomes much clearer when you compare the math directly.

30-Year vs 50-Year: What the Numbers Actually Look Like

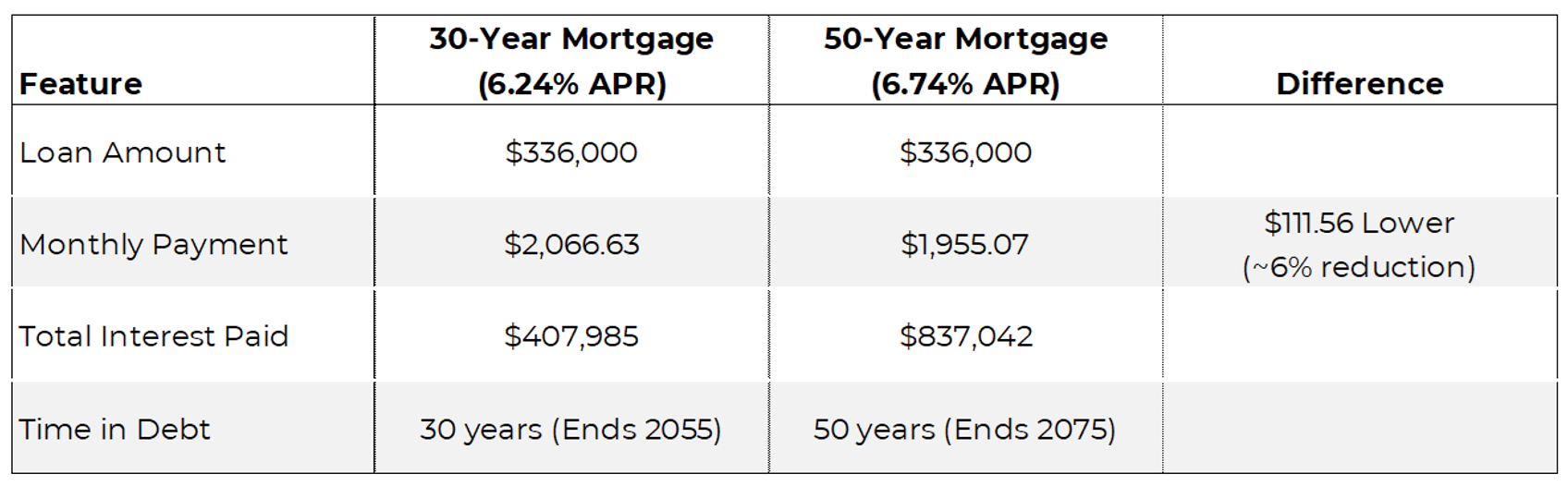

As Charlie Bilello shows, a $420,000 home with 20% down results in a $336,000 mortgage with the following monthly payments and total interest paid.

The reality is that a 50-year mortgage at current rates only reduces the monthly payment by a little over $100 (roughly 6%) but more than doubles the total interest paid and keeps the borrower in debt for an additional two decades.

Equity Builds Much More Slowly

The structure of amortization matters. In both cases, the early years are overwhelmingly interest rather than principal. On a traditional 30-year mortgage, the homeowner builds enough equity to fully own the home after three decades. On a 50-year mortgage, after that same 30-year period, the homeowner still has more than $280,000 of principal remaining to be paid off over the remaining 20 years of the loan. The cost savings feel meaningful only in the short run, but the financial burden may expand dramatically over the long run into retirement, when the homeowner may have less cash flow available.

Is This Really Making Housing More Affordable?

This raises a bigger question about the direction of housing policy and lending innovation. A longer mortgage technically reduces the monthly payment, but does that make the home more affordable, or simply make the cost easier to mask?

There is a parallel to the world of higher education. Government-backed student loans were originally introduced to make college cheaper and more accessible for more people. Instead, colleges adapted by raising tuition. The growth of subsidized loans increased the capacity to pay, and prices rose to absorb it. Housing risks repeating the pattern. If the solution to high home prices becomes longer mortgages, the result is unlikely to be cheaper housing. It is just expensive housing stretched across more years.

The Scenario Where a 50-Year Mortgage Changes the Equation

If we want to subsidize homeowners, there is an explicit situation in which 50-year loans become more interesting…when interest rates fall materially. In a low-rate world, the longer maturity can dramatically reduce monthly payments without the tail remaining for homeowners 30 years into the future. A 3% 30-year mortgage reduces the monthly payment from $2066 to $1419, while a 3.5% 50-year mortgage lowers the monthly payment by another 16% to $1185. At those levels, this is inexpensive leverage that frees up meaningful monthly cash for saving, investing, childcare, or retirement contributions.

The benefit simply does not exist at today’s rates.

Bottom Line

A 50-year mortgage in today’s rate environment barely improves the monthly payment while dramatically increasing the total cost and slowing the pace of equity building. It does not fundamentally solve the affordability challenge. It makes the mortgage feel cheaper while making the house far more expensive over time.

Until rates decline significantly or lenders price 50-year loans much more attractively, traditional 15-year and 30-year mortgages may remain the stronger choice for most homebuyers.

Disclosures

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

*Conceptual/Illustrative: Information presented in the above charts are for illustrative purposes only and should not be interpreted as actual performance of any investor’s account. As these are not actual results and completely assumed, they should not be relied upon for investment decisions. Actual results of individual investors will differ due to many factors, including individual investments and fees, client restrictions, and the timing of investments and cash flows.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2512-3.