Over the past two decades, ETFs have become the vehicle of choice for investors. They are liquid, transparent, low-cost, and viewed (often correctly) as highly tax-efficient compared to mutual funds. The secret has always been the in-kind creation and redemption process, which allows ETFs to defer capital gains that mutual funds routinely distribute to shareholders.

That structure is why ETFs have gained trillions in inflows while mutual funds have steadily lost ground. Investors appreciate being able to control when and how they realize capital gains.

But here is the reality. While ETFs solved the capital gains problem that plagued mutual funds, they had done little to solve the bigger tax issue in fixed income until now.

Bonds Have a Tax Problem

Here is the catch. ETFs do not eliminate all taxes. Even though capital gains can be deferred, ETFs must still distribute most of the income generated each year by underlying components. For equity ETFs, that primarily means dividends. For bond ETFs, it means coupon interest.

And those distributions matter. Whether as an investor you take the cash or reinvest it, you owe taxes in the year they are paid and in the case of fixed income, at the short-term (i.e., higher) tax rate. That creates a tax drag on long-term returns, especially when the underlying portfolio is income-heavy.

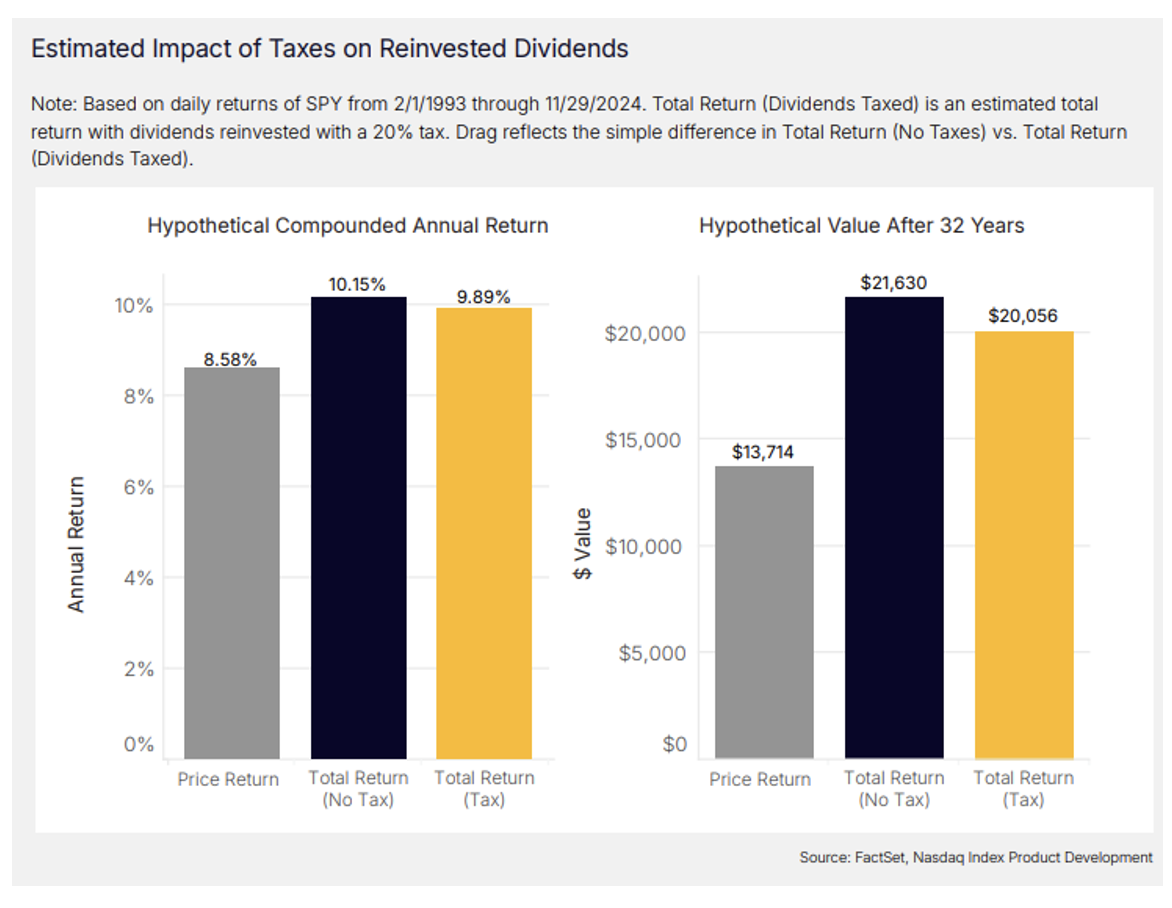

The math bears it out. A recent white paper by Nasdaq uses the S&P 500 to show that reinvesting dividends after a modest 20% tax cut annual returns by only 26 basis points over three decades, yet that seemingly small drag reduced total asset growth by 7% over a ~30-year window. In higher-yielding assets, such as fixed income, the drag can climb to 1-2% annually, whether in the form of an ETF or mutual fund. That compounding tax cost is the “residual burden” fixed ETFs have never solved.

Why Bonds Are Different

In equities, the ability to defer capital gains makes a meaningful difference because distributions are a relatively small piece of the total return equation.

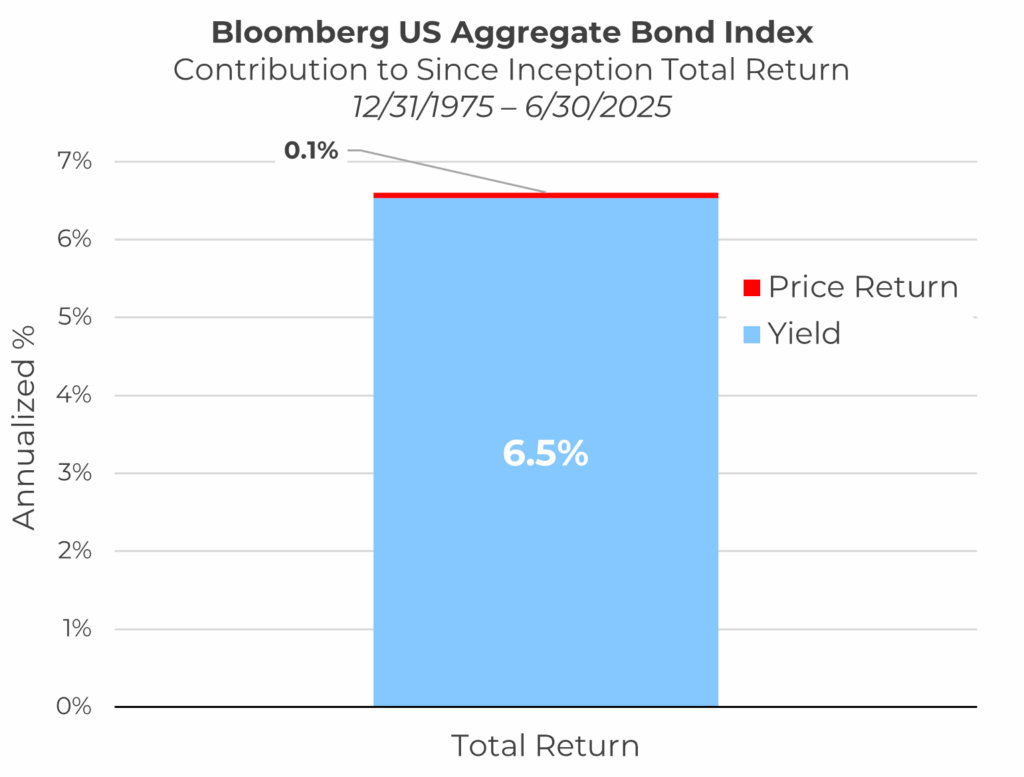

In fixed income, the opposite tends to be typically true as bond returns are overwhelmingly coupon-driven. A past study we performed showed that 99%+ of all returns from the Bloomberg Aggregate Bond Index since its 1976 inception were in the form of coupons. That happened whether in a mutual fund or an ETF.

Source: Aptus via Bloomberg

Unlike their equity counterparts, fixed income ETFs traditionally offered very little tax advantage over fixed income mutual funds. Investors still face a steady stream of taxable income year after year.

Put simply, the ETF wrapper helps defer capital gains, but in bonds, there are not many capital gains to defer.

Here’s How to Fix It

The good news is that investors are not limited to the traditional tradeoff in fixed income. There are practical ways to improve the after-tax experience:

→ Seek strategies where capital gains are a larger driver of return rather than relying almost entirely on coupons.

→ Use funds with more tax efficient tools such as swaps or derivatives, to deliver bond and return-seeking exposure without constant income payouts.

→ Explore structures that convert what had been income into capital gains, which are taxed more favorably and often can be deferred.

→ Own more stocks (less bonds) with direct hedges, giving investors the ability to participate in long-term equity growth while managing downside risk and reducing taxable distributions.

Each of these approaches has the same goal. Keep more of the return compounding by reducing or eliminating inefficient taxable distributions.

Final Thoughts

Fixed income funds have a tax problem. While ETFs solved the capital gains issue that hurt mutual funds, they did not fix the flow of taxable income that can drag on long-term results.

For investors focused on after-tax outcomes, the opportunity is not simply choosing ETFs over mutual funds. It is embracing new ETF solutions and structures designed to minimize distributions altogether. These innovations address the last mile of tax inefficiency and give investors the chance to keep more of what markets deliver, which is the whole point.

Please reach out for more about our push for higher after-tax returns.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2509-11.