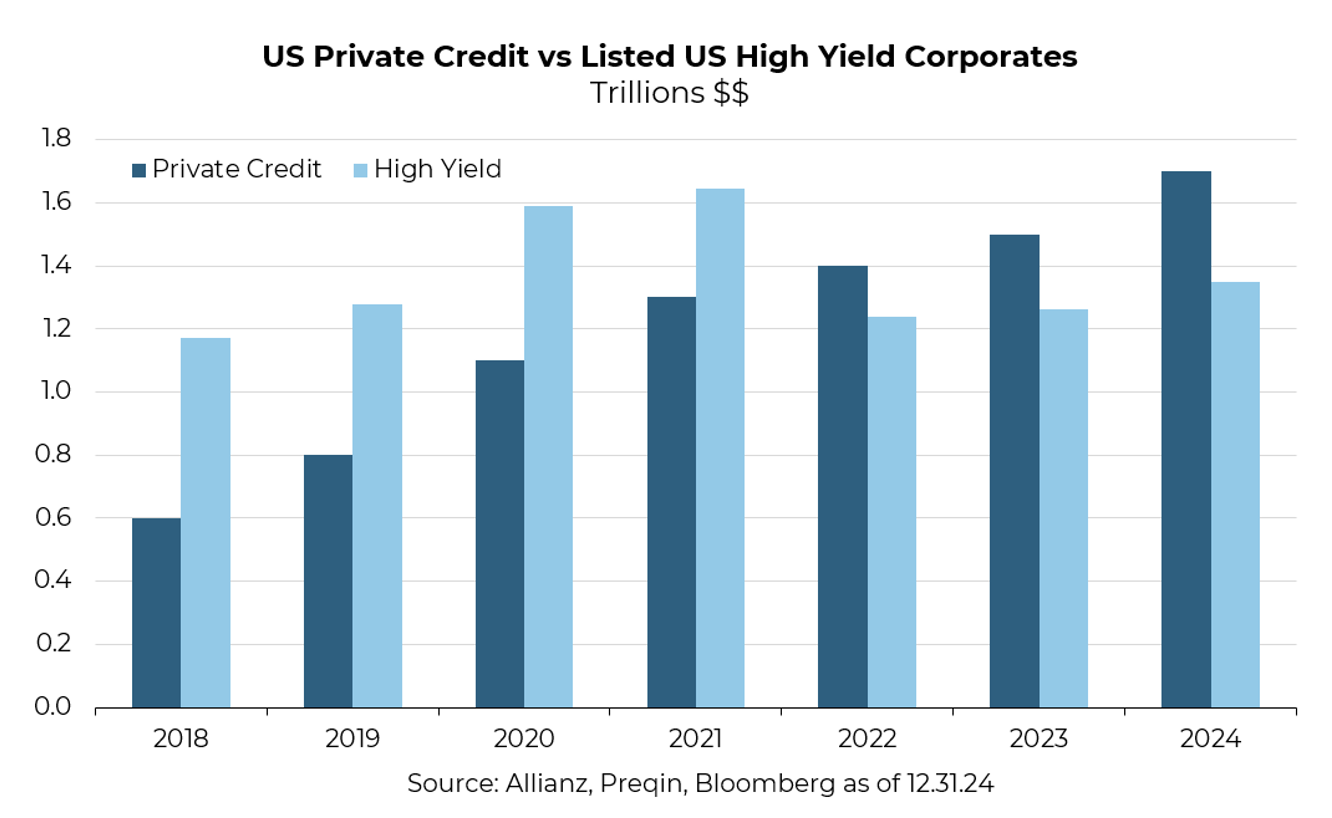

Private credit has become the industry’s favorite shiny object, recently surpassing the entire market for listed high-yield corporate bonds with $1.7 trillion in assets per Preqin. The yield looks great, the line on the chart looks smooth, and the marketing is persuasive. And to be clear, private credit is not all the same. We evaluate private credit offerings regularly, and we’ve seen a lot. There are parts of the market where loans are secured by hard collateral, such as income-producing real estate with real equity beneath it. Those structures can often justify lower volatility because recoveries tend to be anchored in something tangible.

But what has driven most of the recent boom is a very different segment of private credit: unsecured or lightly-secured corporate lending packaged inside diversified funds, often enhanced with fund-level leverage, and increasingly positioned as a “low volatility” replacement for traditional public bonds. This version is now showing up in retail accounts with strong lobbying to be pushed into 401(k) plans.

This is where concerns begin to emerge because the smooth line on the chart is not evidence of lower volatility, but rather unreported volatility tied to assets that are a) not listed, b) rarely revalued, and c) often priced in ways that depend heavily on incentives.

And real-world challenges are starting to pile up.

Bloomberg recently highlighted a stark case. A position in Renovo Home Partners was marked at 100 cents on the dollar a month ago and marked at zero a few weeks ago. It looked stable right up until the moment the new valuation had to reflect reality.

We think the pricing inconsistencies may run even deeper. Bloomberg separately showed two major private credit managers marking the same loan at materially different levels. One at 91 cents. Another at 77. Same borrower. Same collateral. Two different realities. If the largest firms in the world cannot agree on a price, it raises questions for daily-priced retail funds to claim they can.

And then came the news in the FT that Blue Owl, one of the largest private credit managers in the world, would block all redemptions from their existing retail fund after redemptions climbed to 6% of NAV in the most recent quarter. Instead, the fund manager proposed a merger into a fund trading 20% below its marked asset value, along with a permanent loss of redemption rights to investors. A structure marketed as stable income became illiquid the moment investors tried to access their money, suggesting the reported NAV is not realistic for the liquidity demanded by investors.

Private asset firms understand these dynamics well. They also understand liquidity can be slow and exits challenging. That seems to be why, as noted in a recent discussion on The Economist podcast, private asset managers have lobbied to push these strategies into 401 (k) plans and 1940 Act wrappers like the above. Traditional LP commitments have slowed, fundraising has become more difficult, and new pockets of capital are needed. The hope appears to be that if institutions are pulling back, retirement plans that default investors into target date funds appear to be asked to fill the gap.

In our view, retail savers should not be the liquidity source for opaque assets that they cannot evaluate or see pricing. Fund managers may benefit, but we do not see the upside as commensurate with the risk for participants when asked to absorb the downside as markets adjust. When we add everything up, we believe the conclusion is clear. Illiquidity, opaque valuations, misaligned incentives, and delayed volatility do not belong inside default retirement products.

The following are the core issues as we see them:

Issue 1: Retail investors do not understand private credit

Private credit is opaque and negotiated behind closed doors. It behaves nothing like the liquid public bond sleeve investors think they are buying when selecting a target date fund.

Specific to retirement plans, many plan participants are auto-enrolled and assume retirement funds hold transparent, low-fee, liquid stocks and bonds. That assumption collapses once complex private loans with limited disclosure and manager-to-manager pricing differentials enter the mix.

Issue 2: Illiquidity and valuation chaos

Private credit does not trade on exchanges and does not have real-time pricing. When two large managers assign a 14-point gap to the same loan, that is not a rounding error. We believe it is a sign that the asset may not be suitable for a product designed to be priced daily, rather than what a default retirement vehicle should contain.

Issue 3: Misaligned incentives

We believe the incentives across the ecosystem are pointed in the wrong direction. Target-date sponsors may want the higher yield and lower reported volatility because it helps reported results. Private credit managers want inflows because they need liquidity and fee revenue. Politicians may appreciate the lobbying dollars that support these efforts, but it is retail savers who ultimately provide the liquidity and take the risk. According to public lobbying disclosures, at least one private market firm has spent more than $3.5 million on lobbying in 2025 alone. We do not think that effort exists because the structure primarily benefits retirement plans.

Issue 4: Private credit is expensive

There are fees at the origination level. Fees at the fund level. Carried interest on performance. Monitoring fees charged to borrowers. Transaction fees. Structuring fees. By the time all layers are finished, there is a real possibility the incremental yield may barely clear the cost for retail investors. Meanwhile, investors can access public bonds, Treasuries, and TIPS for a few basis points. These markets are liquid, transparent, and priced continuously. The hurdle for private credit to justify its fee stack has never been higher, especially when spreads are near cycle lows.

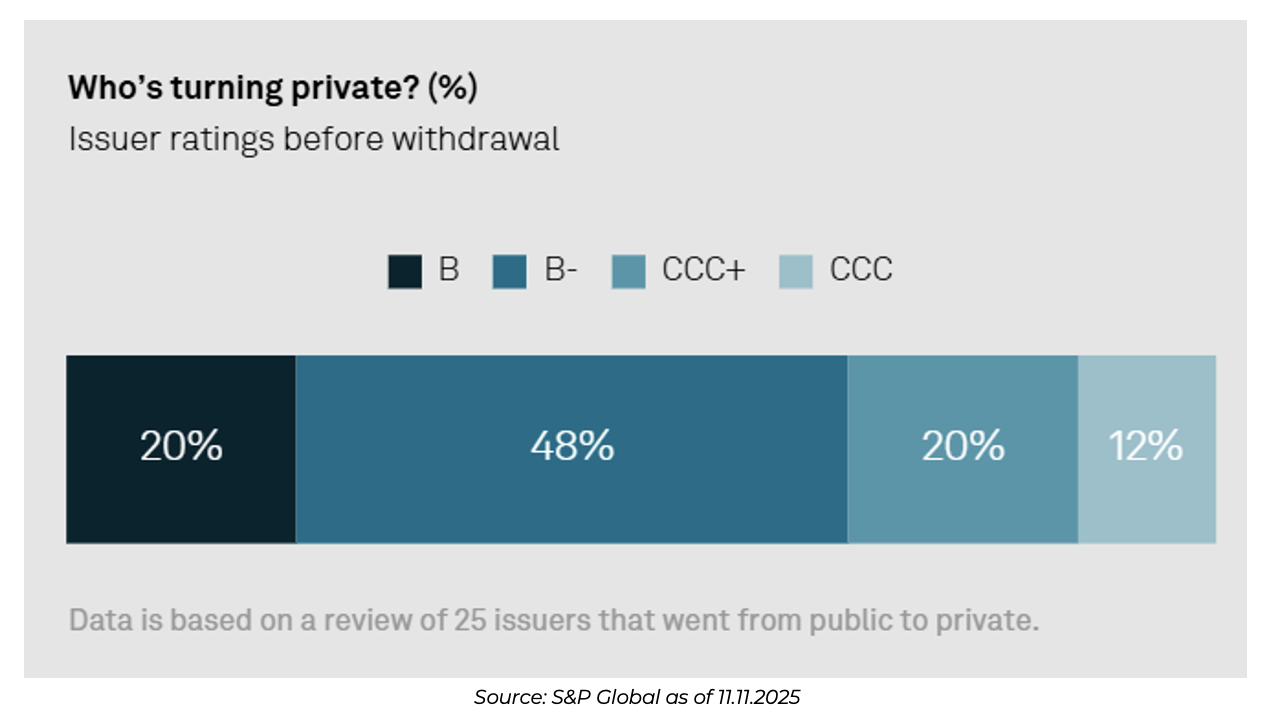

Issue 5: The cycle appears to be late stage

Introducing new retail investors to private credit at this stage of the credit cycle may prove challenging. Spreads across markets aren’t far from cycle lows, covenants appear light, and the quality of issuers turning to the market appears to be low quality, according to S&P Global.

Historically, this has been the moment when buyers, not sellers, pay the price. And if something breaks inside a target-date fund, we do not believe it will be the sponsors who absorb the impact. It will be the participants who may not even know what they own.

Pulling It Together

Private credit is not inherently bad. But in our view, it does not belong as a base allocation to retail investors who don’t understand the risks, and definitely not inside default retirement products that rely on transparency, simplicity, and daily liquidity. Target-date funds are supposed to be straightforward. Predictable. Easy for participants to trust.

Private credit is opaque. Illiquid. Priced inconsistently. Expensive. And now being pushed into retail channels for reasons that benefit everyone except the end investor.

The smooth line on the chart is the trap. The risk is real. And retirement savers deserve better than to be the liquidity sleeve for an asset class even the professionals cannot price consistently.

If you are evaluating a private fund or own one already, we are happy to review it and outline the real risk-return trade-offs in plain English.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2511-15.