The Fed left rates unchanged for its 5th straight meeting — keeping the fed funds range 4.25%-4.5% which was widely expected. Governors Miki Bowman and Chris Waller dissented in favor of a 0.25% cut. It was the first double-dissent by governors since 1993.

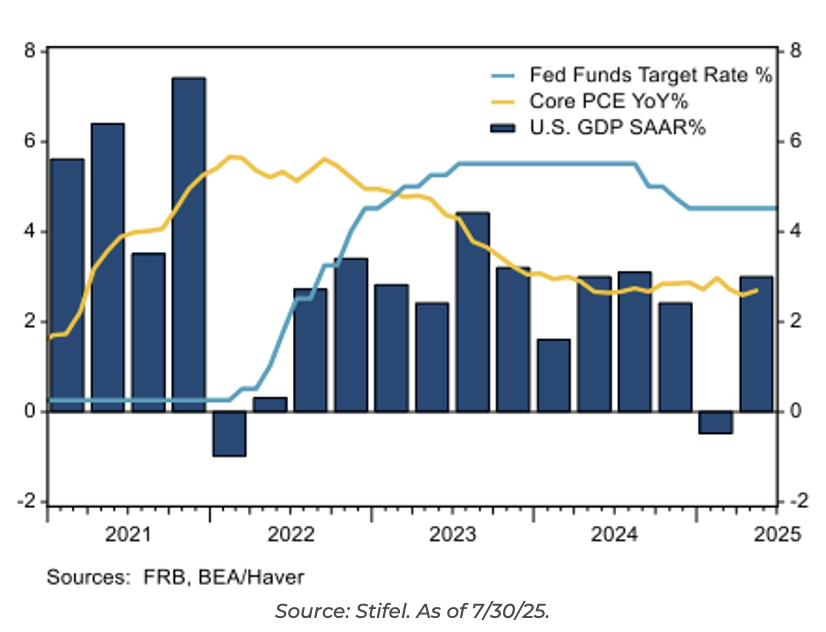

The statement had only one material tweak, to observe that growth “moderated” in the first half; previously, growth was observed to have continued to “expand at a solid pace.” The updated assessment of activity reflects an average growth rate of 1.2% in the first half of this year, a material slowdown from the 2.8% average in the back half of 2024.

The adjustment in language likely reflects the slowing private final demand seen in 1Q and 2Q reports. There was no change in the description of the balance of risks, and the Committee remains attentive to risks to both sides of its mandate. Nor was there any change in the very limited forward guidance. Overall, there wasn’t much to take from this statement regarding the next meeting in September.

The Committee continues to wait for more clarity regarding fiscal policies, particularly tariffs, and their potential impact on the economy. They have two inflation reports and two employment reports between now and the September meeting, which could weigh on the “data-dependent” outcome.

The Q&A session was filled with questions tilted about why the Fed isn’t reducing its policy rate. The questions regarded lower inflation metrics, some labor market softness, growth positive but down, and the dissents from Bowman and Waller. It’s clear it’s not just the President wanting rate cuts; the media does too!

Putting The “No Cut” Into Perspective

The central bank has been 180’ed by the Trump administration. They are in a scenario where they perceive two conflicting threats to their mandate – the prospect of higher inflation (from tariffs) and lower output/employment (from tariffs and deportations). Demand has come down somewhat, but it appears the committee thinks supply has as well. Add on top the CPI running above target for 4 years straight, and if another burst of inflation were to come – even a “transitory” one – it would be extremely uncomfortable for the Fed.

The good news is that we are finally reaching the limits of Fed “can-kicking”. With growing internal disagreements, the FOMC reached a sort of compromise in June that if the tariff inflation didn’t show up by September, it would end its “wait and see” period and deliver the rate cut markets have been waiting for. Now we move on to Jackson Hole in less than a month for further clues of what’s to come.

Stocks turned south on Powell’s comment, “You could argue we’re looking through goods inflation by not raising rates”, as the market sentiment for a September cut declined. Current interest rate futures are pricing at about a 48% chance of a September rate cut, well off the highs.

Where is Inflation Headed?

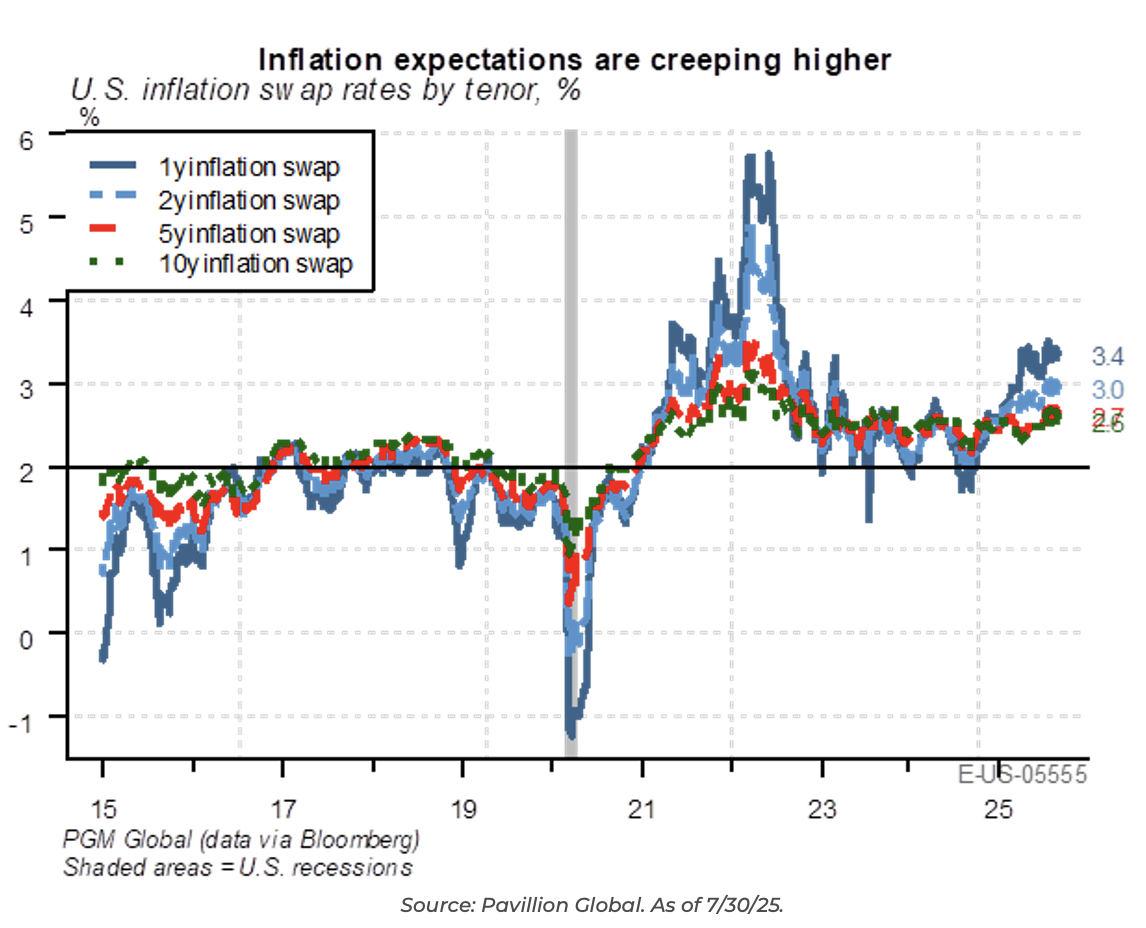

Inflation expectations are now rising across the important tenors, even as oil prices remain near the lower end of their recent price range.

Inflation pressures continue to hinder the ability of the Fed to cut rates without risking losing the long end of the yield curve. The inflation game feels like a bit of whack-a-mole. Some components are playing nice while others show some heat.

Powell commented on this dynamic during his press conference, “Service inflation has been moving lower while goods inflation has firmed, a swap from what we saw in the last couple of years.” Of course, the recent rise in goods inflation is being attributed to tariffs.

Sticky inflation will continue to lead to a slow reaction function from the Fed. The risk here is that inflation continues to settle in slightly above target (call it 2.5-3%). The problem from there is what type of hardship does it take to bring it down the last bit? Is the juice worth the squeeze?

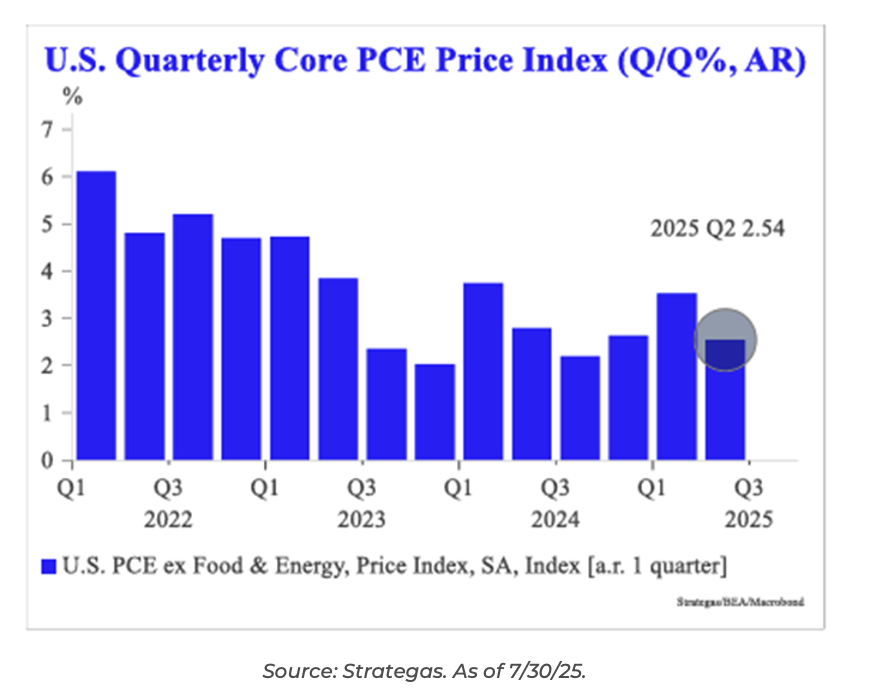

As you can probably tell, I think the Fed should have gone ahead with the cut…one cut isn’t likely to rock the boat, but I think it would have been a positive sign to parts of the market most impacted by the current rate hiking cycle. Core PCE Q/Q is running at 2.54%, as they say, “Good enough for government work”.

Finding the Neutral Rate

It’s hard to know exactly how much above “neutral” the Fed’s interest rate is. Fed Chair Jay Powell says you’ll only know for sure once you get there, which is reasonable since the neutral rate can’t be observed directly—it’s just an estimate.

A restrictive rate slows demand enough that inflation drops, but if rates stay too high for too long, growth will falter, and a recession could follow because company profits shrink and weaker firms close.

One popular way economists judge if a policy is restrictive is to look at the yield curve. Right now, the curve is normally shaped from the 3-year note through the long bond, but the front end of the curve is inverted from the FFR to the 3-year note. This suggests the Fed’s rate is above the market determined rates.

Treasury Secretary Bessent referenced this inversion when he urged the Fed to move at least a little closer to neutral while they “wait and see” on tariff impacts. However, this is not a perfect measure, since the front of the curve mainly reflects expectations of what the Fed will do next, not necessarily where the neutral rate should be.

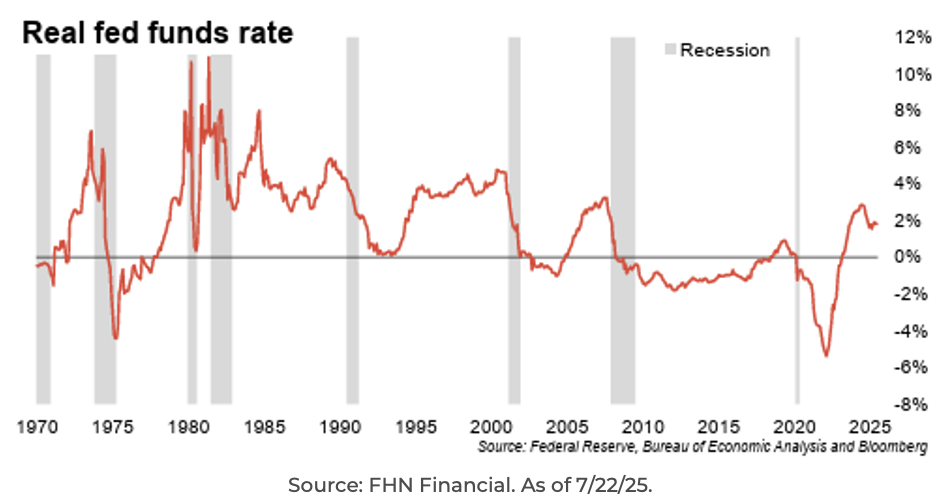

Another rule of thumb—often attributed to former Fed Chair Alan Greenspan—is that the real fed funds rate (interest rate minus inflation) needs to be negative to truly boost a weak economy. Historically, many economists considered a real rate around 2% as “neutral”, which, as it happens, is exactly where we are now.

In short: There’s no simple way to know if rates are at neutral, but signs like the yield curve and the relationship between inflation and interest rates give clues.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2507-29.