You don’t earn your gross salary.

The number on the offer letter and the number in your bank account are two different figures, and everyone understands the gap. Withholding comes out first. But the subtler trap comes when you receive a small raise. Picture a 3% bump that is purely a cost-of-living adjustment. Your salary is higher, the price of everything is higher by the same amount, and your real income has not moved an inch. Yet the IRS does not care. It taxes the full 3% increase as income, even though none of it left you better off. You paid real tax on a raise that was not real.

A bond’s coupon works exactly the same way, and most investors read it as if the headline is the take-home. It is not.

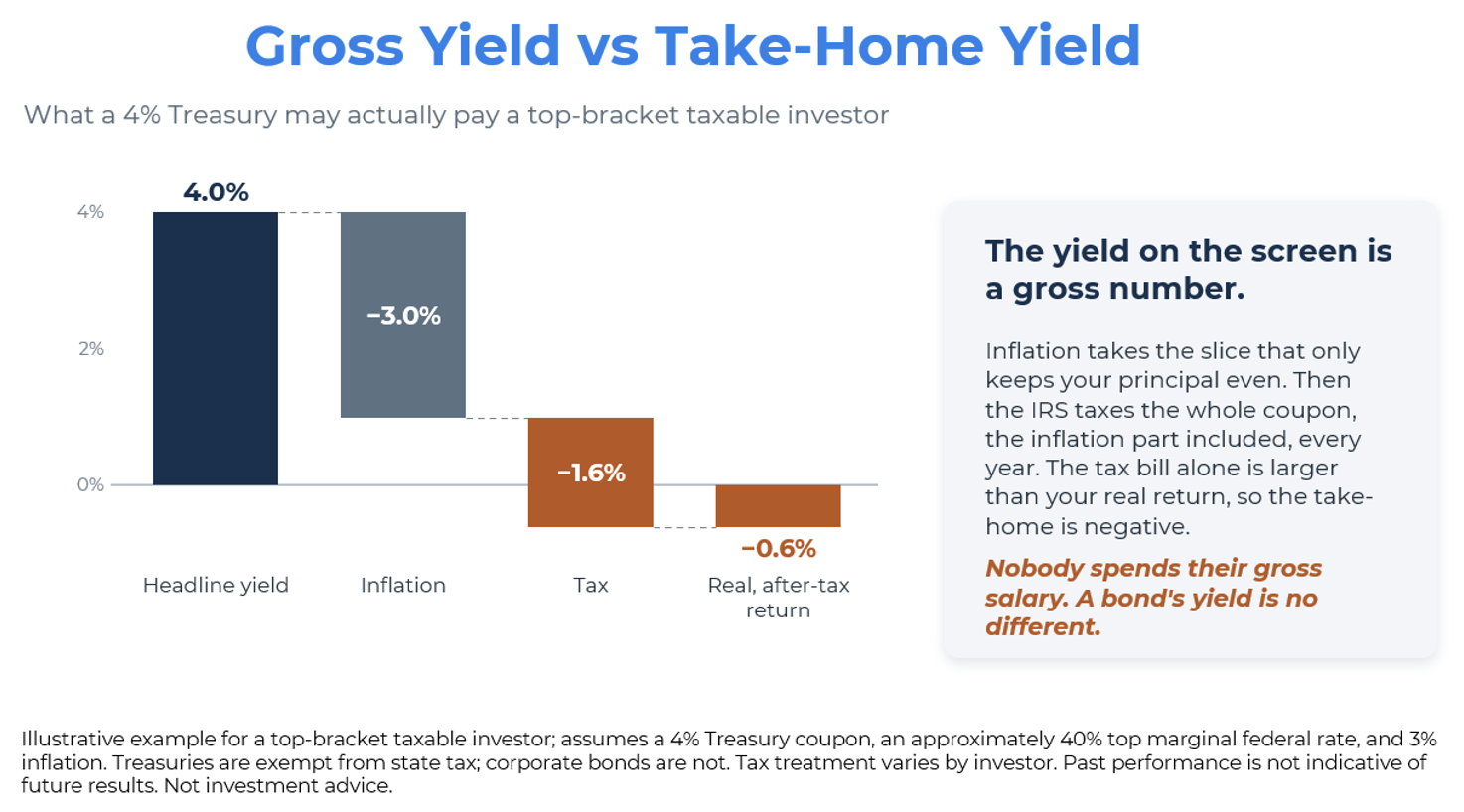

Start with what the coupon is actually made of. Part of any yield is simply compensation for inflation, the slice that keeps your principal’s purchasing power from eroding while you hold the bond. Whatever is left on top is your real return. On a 4% bond when inflation is running 3%, only about 1% of that yield is real. The other 3% are the bond running to stand still.

Here is the part the yield-chasers never quote. The IRS does not tax your real return. It taxes the entire coupon, inflation compensation included, at ordinary income rates, the investor’s highest marginal rate, every year, whether the bond is up or down. Not the preferential rate that long-term stock gains enjoy. The full freight, on the nominal number, before inflation is ever subtracted and before that money is spent.

At a top bracket, the tax on a 4% coupon is ~1.6% and more on a corporate bond where state tax applies too. Your real return before tax was about 1%. The tax bill alone is larger than the entire real return, which leaves the real, after-tax return negative. You did not earn 4% and hand back a slice. You earned roughly a point of purchasing power and were taxed as though you had earned four.

This is why “but yields are finally high again” is only half true. Higher yields are genuinely good news. But the number on the screen is like a gross salary, and you don’t spend your gross salary. The IRS taxes the part of your yield that was never really income, which is why the real, after-tax number is so much smaller than the headline.

We believe the honest verdict is narrower than the bond bulls want. Higher yields are good news mostly for bonds held where the annual tax does not bite, inside a tax-deferred account, where the coupon can compound without the yearly haircut. In a taxable account, a static bond allocation is still leaking. It leaks more slowly than it did when the ten-year yielded 0.5%, but it leaks.

So the question for a taxable investor is not “what does this bond yield?” It is “what does this bond keep, after tax and after inflation, in the account I actually hold it in?” Asked that way, the answer increasingly points somewhere other than a traditional bond.

This is the Aptus mantra at work: More stocks. Less bonds. Same risk. It also, hopefully, leaves the taxable investor with a better after-tax outcome.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2606-21.