Every so often, margin debt headlines resurface as a supposed warning sign for the stock market. The latest iteration: U.S. margin balances have crossed one trillion dollars for the first time.

David Rosenberg highlights:

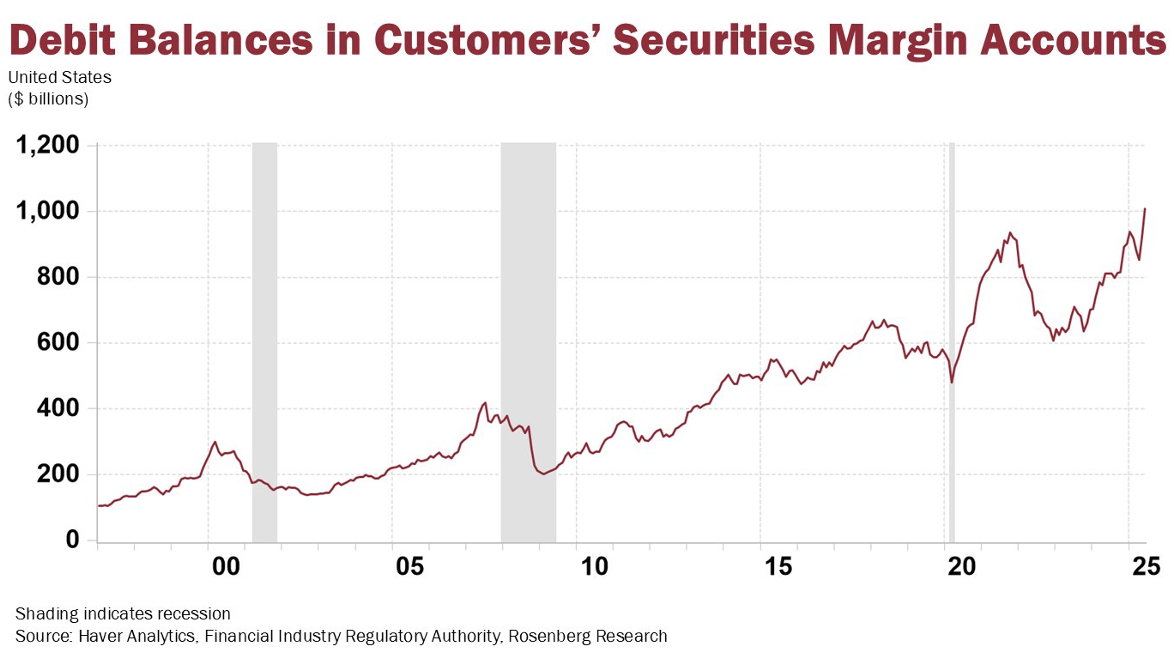

“For the first time ever, margin debt has topped $1 trillion and has ballooned +25% over the past year. Fully one-fifth of all the leverage supporting the stock market has been built up just in the past year alone; almost half of the outstanding margin debt has come in the past five years alone. That is quite an achievement. It’s also pretty scary.”

While that sounds ominous, this post will outline why it is not particularly useful.

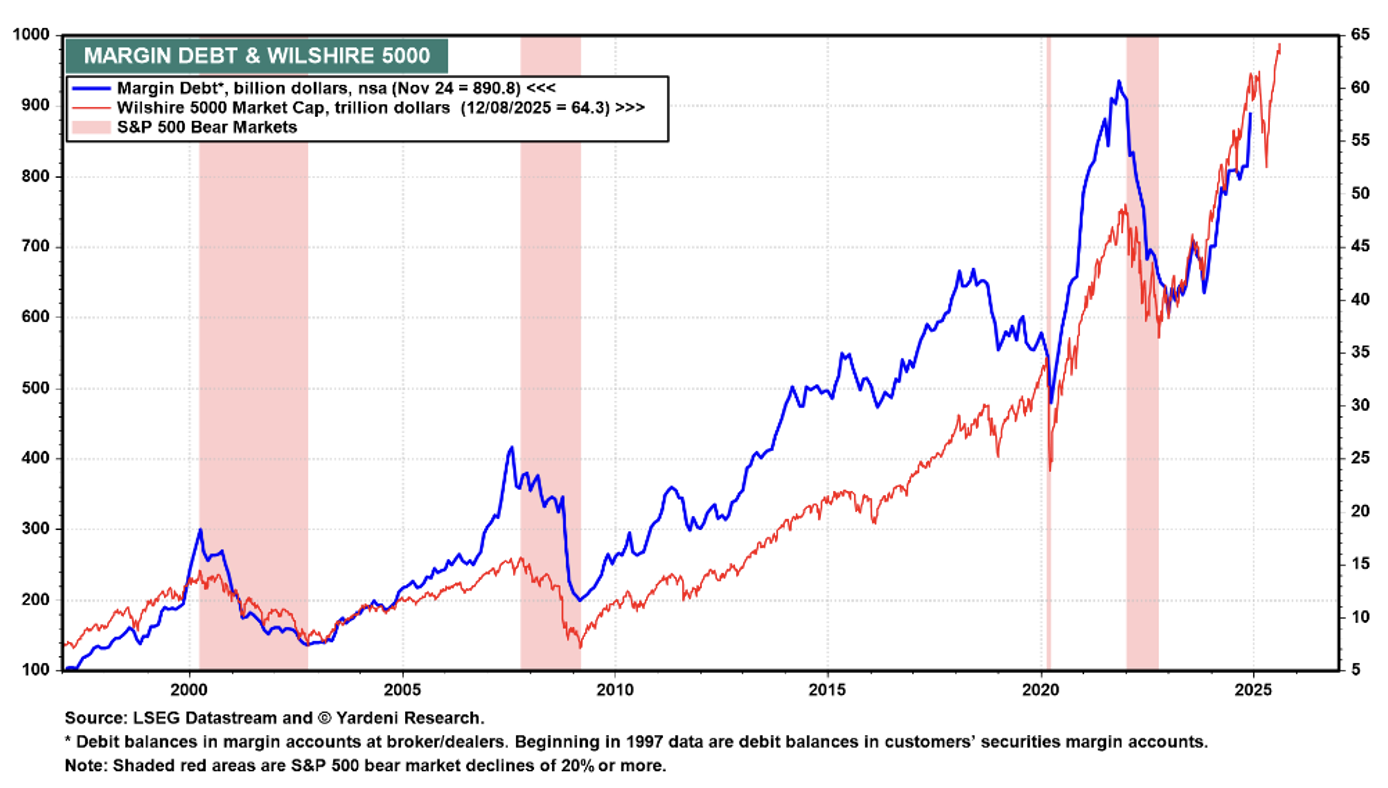

The core issue is that margin debt is a coincident indicator. It moves with the market. When equities rise, account values increase, and investors naturally take on more leverage. Margin debt rising ~25% over the last year? The S&P 500 is up about the same. Margin debt has almost doubled over the last five years? The S&P 500 is up about the same.

Source: Yardeni Research

Source: Yardeni Research

Historically, margin debt peaks alongside other coincident metrics like stock prices, earnings, and economic strength. That is because it is part of the same cycle. Margin debt does not predict market tops any more than corporate profits or index levels do. It tends to follow rather than lead.

None of this is to say leverage is irrelevant. It can certainly amplify market moves, especially on the way down. But we believe using margin debt as a standalone warning sign is misguided. Most of the time, it is just a byproduct of rising markets. By the time it reverses, the market already has.

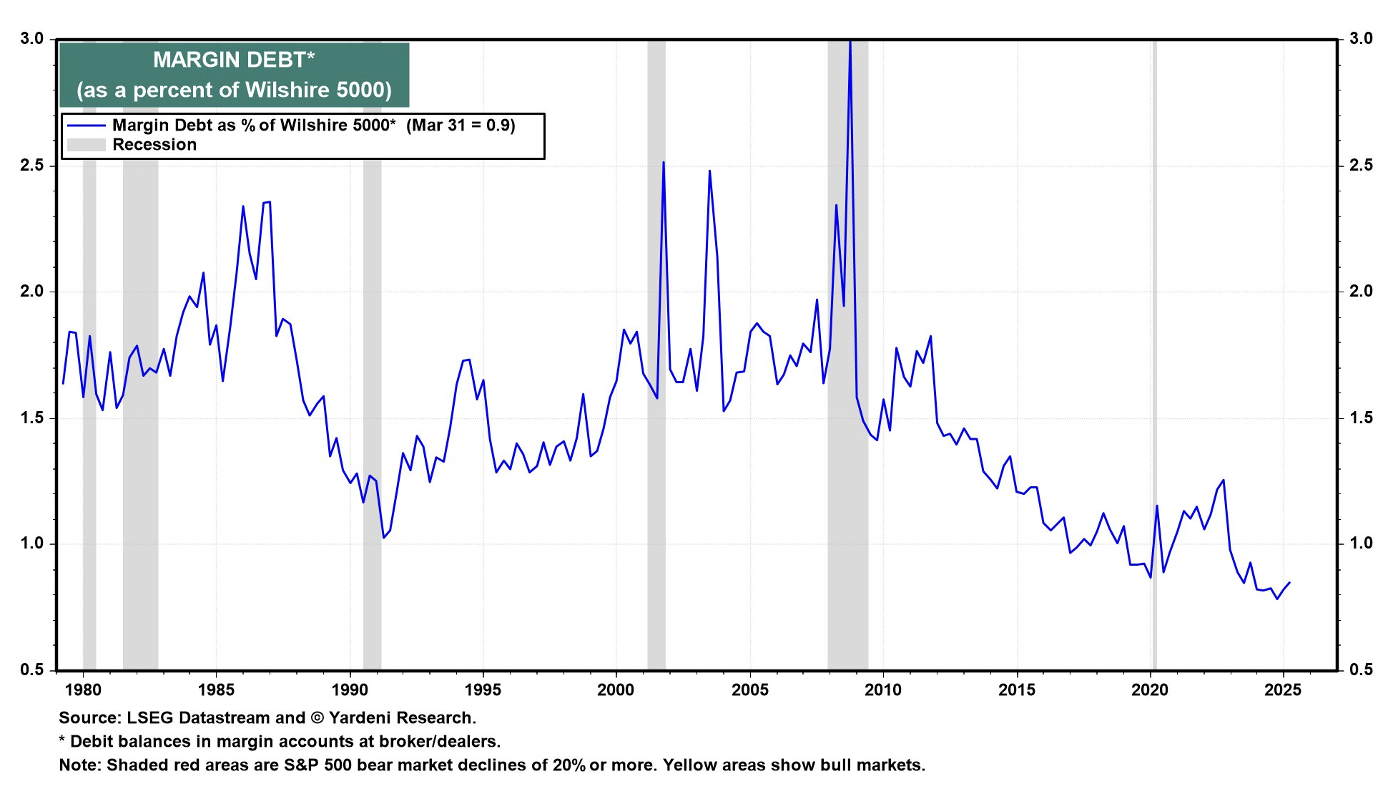

If anything, the total dollar value of margin debt should be normalized against something, such as the total market cap of equities. Even then, the relationship with future returns is noisy at best. A high margin-to-stock market cap ratio might indicate more fragility, but it still won’t tell you when the next correction will hit. We also happen to have a very low level of margin debt normalized against the market cap of US stocks.

Source: Yardeni Research

Source: Yardeni Research

Yes, leverage matters. But earnings, interest rates, liquidity, and sentiment matter more. Margin debt is part of the story, not the story.

So the next time you see a chart of rising margin balances used to forecast a crash, remember this: margin debt reflects where we are, not where we’re going.

Disclosures

Past performance is not indicative of future results. This material is not financial or tax advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed and all calculations may change due to changes in facts and circumstances.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2508-14.