Risk tolerance is used (a lot) in the wealth management space, and I’m not sure anybody thinks about what they are saying at this point. Here’s the gist of what is usually meant:

Let’s say you are aggressive as an investor. That tends to mean you can stomach the value of your invested assets fluctuating, at least more than a conservative investor. To take it a step further, stocks tend to be viewed as ‘risk’ assets while bonds are viewed as ‘conservative’ assets.

With that logic laid out, the traditional framework of portfolio construction is that aggressive investors need more stocks and less bonds while conservative investors need the opposite. For the sake of time, we will ignore risk capacity.

We’ve all played into this line of thinking, Aptus included, and that bothers me. It bothers me because it’s flat out wrong. I get the line of thinking and I’m not arguing that adding more bonds doesn’t reduce the fluctuations in account value. Our stance is that fluctuations in account value are meaningless, especially if that puts capital at risk!

We tend to lightly tread on this subject, but those days are behind us. We want to force change at the highest level of portfolio construction – asset allocation. It starts with viewing risk through the correct lens.

Purchasing Power

After thousands of meetings with advisors and investors of all backgrounds, I’ve found very few investors who want stability if the sacrifice for it is their purchasing power.

Your client capital devoted to bonds and cash equivalents is at risk! They are certificates of confiscation. They have been and will continue to be.

Yes, for short-term money – I get it, but for anything with a long-term horizon, I believe it’s time to question the traditional logic.

Don’t fall for the illusion of control. Increasing bonds to be conservative may lower fluctuations in account value, but it is increasing your risk. We think your main concern should be to protect purchasing power, that’s the risk at hand.

Here’s some data to support our convictions…

Fiscal Backdrop

The US Federal government spends more than it receives. This imbalance creates a deficit. Below is the deficit over time with the blue line (left axis) being in % of GDP terms and the red line (right axis) being in dollar terms.

The deficits are relentless, year after year, and that’s reflected in our ever-increasing debt loads. As in the chart above, below shows the Total Public Debt as a % of GDP in blue and in dollars with the red line.

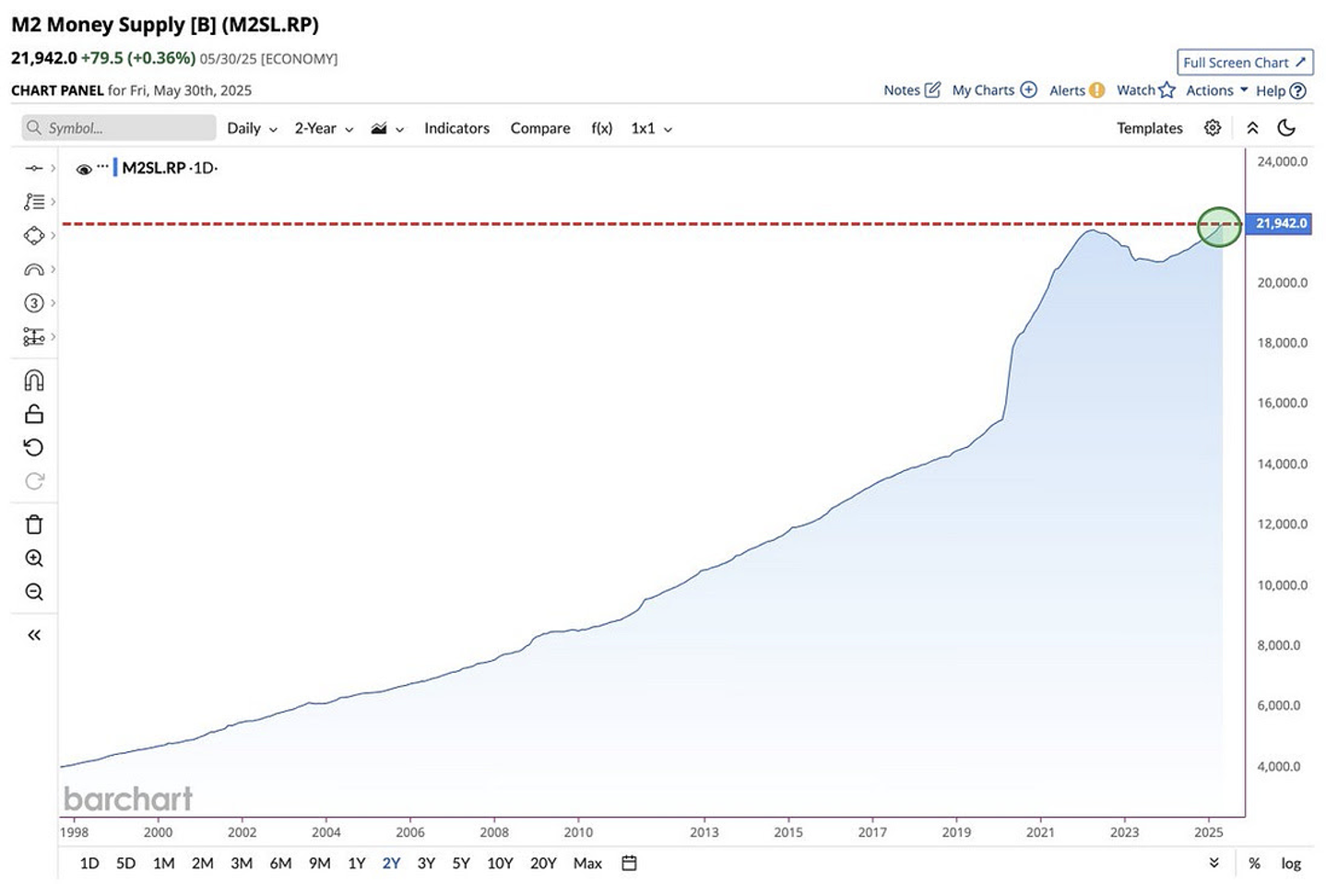

As debt increases, so does the supply of dollars.

You can argue this doesn’t matter. Here’s a reminder of why it does, from last month’s note:

-

-

- This means that $1,000,000 in 1972 would buy the same amount of goods and services as $7,550,358 would buy today.

-

-

-

- $1,000,000 today only has the purchasing power of $132,444 in 1972 dollars.

-

-

-

- Purchasing power of $1,000,000 has eroded by about 86.76% since 1972 due to inflation.

-

We have arguably hit what Lyn Alden calls Fiscal Dominance. Her image below captures the implications as clearly as anything can:

In other words, Choo Choo… there’s no stopping this train.

Risk Tolerance

“It is the protection against the worst of outcomes, and the active participation in the best of outcomes, that will differentiate the long-term performance of terminal capital.”

– David Dredge

If the objective of investing is to preserve and/or grow purchasing power, which I think it is, then risk tolerance should be thought of differently.

Asset Allocation decisions matter more than any other you’ll make as it relates to successfully accomplishing investment objectives. If you simplify the choices into just stocks or bonds, the appropriate allocation for long-term assets is simple… bonds should be avoided.

We aren’t advocating just own stocks and hold on for the ride; we advocate for convexity in portfolios, with that convexity produced by negative carry hedges.

In other words, we want to own more stocks while allocating small portions of capital to sacrificial hedges. Hedges against the stock market risk hold a perfectly negative correlation, while providing a convex payoff profile in the periods most needed. The presence of hedges totally changes our portfolio’s ability to own more risk. Bigger engine with better brakes.

We want to avoid ‘diversifiers’ that inject unknown carry costs and unknown correlation.

We believe risk tolerance is more appropriately discussed with a perspective on hedging. Meaning, how much of your equity risk should be hedged? More aggressive = less hedging. More conservative = more hedging.

We believe this approach to asset allocation and risk control leads to higher terminal values. Maybe I’m dumb, but that seems like a good outcome.

Not to muddy the waters, but I’ve conveniently avoided discussing things like gold and bitcoin. Given the backdrop and our beliefs, the volume of questions around these two holdings is increasing by the day.

I’ll say this, we do believe most investors are managing the real risk relatively better by adhering to our more stocks, less bonds, risk neutral mantra. Internally, there are strong convictions about the potential benefits of gold and/or bitcoin. More to come on that…but maybe, the potential allocation plays into an appropriate risk tolerance framework.

Conclusion

The backdrop is one where we are convinced that the need to own more stocks and less bonds will become increasingly apparent over time.

We will continue to build solutions that help facilitate this shift and model portfolios that express this conviction.

We believe our allocations, which are a blend of risk assets with hedges, are positioned to be better in the tails. It’s the tails that carry the greatest impact towards compounding wealth through time.

If you have any questions at all, please reach out. We want to help cut through the noise. As always, thank you for your trust.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2507-10.