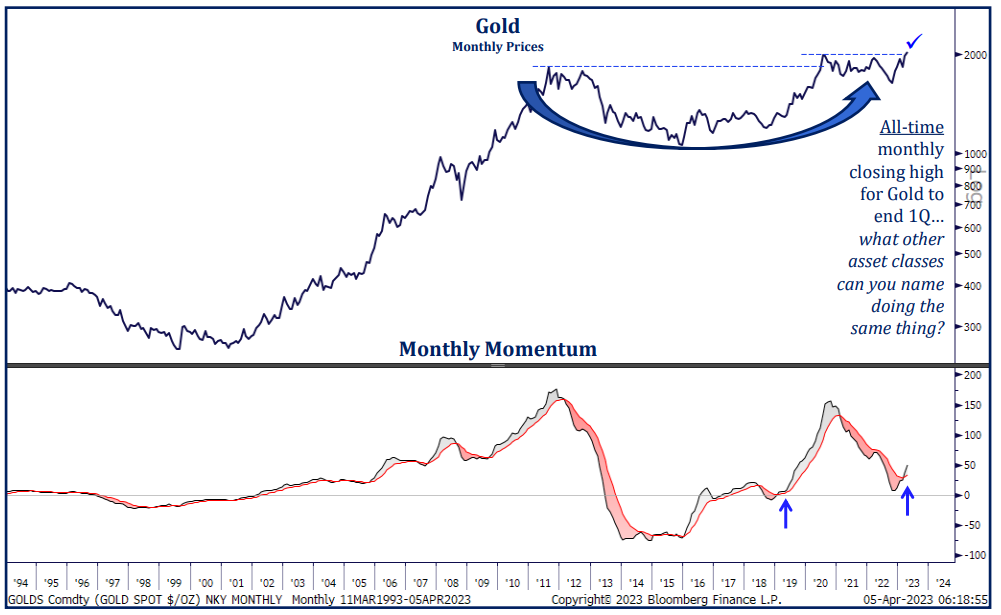

The recent performance of gold has caught investor attention. Following the banking sector stress, and a near-record drop in the US 2-year Treasury yield, markets have had a significant change in risk appetite. Markets have repriced from 100bps of further tightening to a Fed pivot almost overnight. The volatility within the rate markets have caused a spike in the MOVE Index (interest rate volatility fear index) to levels last seen in the depths of the 2008 financial crisis.

Source: Strategas. As of 3/31/23.

Source: Strategas. As of 3/31/23.

The elevated volatility in rates and inflation has led to bonds serving as a less effective hedge against equity declines. On the other hand, gold has outperformed risk assets such as equities and credit, making it an effective hedge in the recent risk-off rotation and rising rate environment. The performance of gold considering the positive level of real yields and risk-free rates has been strong. In this piece, we’ll provide our perspective on the following topics:

- History of gold and its use cases

- Performance drivers

- Cases for owning gold

- Risks of ownership

- Central bank impact

Brief History of Gold

Gold might be the most disagreed upon asset class out there. It’s hard to get an unbiased opinion. Most within the investment commuity either fall into the “Gold Bug” category and stack gold bars in their safe rooms, while the other side thinks gold is a useless paper weight. We thought now would be a good opportunity to attempt to share an objective view on gold and its potential place within asset allocations.

Source: World Gold Council. As of 3/31/23.

Source: World Gold Council. As of 3/31/23.

Why Does Gold Matter in 2023?

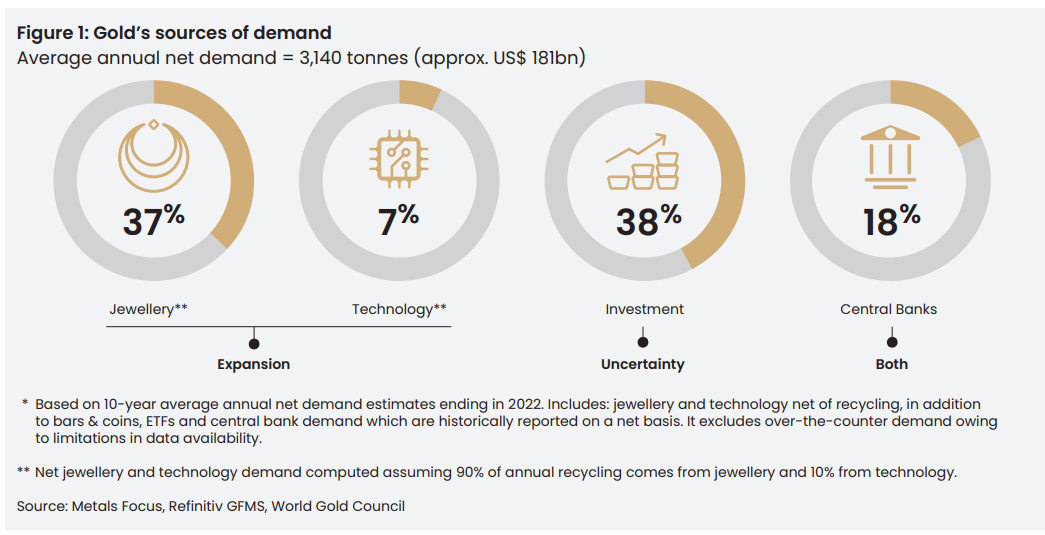

As shown above, gold has many current uses. It has been used as a form of currency for thousands of years. Unlike paper or some electronic currency, gold has a (somewhat) fixed supply and as a physical commodity can be relatively difficult to obtain. In fact, gold mine production has grown slowly over time, only increasing by approximately 1.7% per year over the past 20 years despite the rise in the price.

As a result of its scarcity, gold has been perceived historically as a natural (very long term) hedge against inflation, and provides an alternative to investors when the value of other forms of fiat currencies have depreciated. Gold is the ultimate infinite duration, non-interest bearing real asset.

Source: World Gold Council. As of 3/31/23.

Source: World Gold Council. As of 3/31/23.

Gold Isn’t Just Priced in US Dollars (USD)

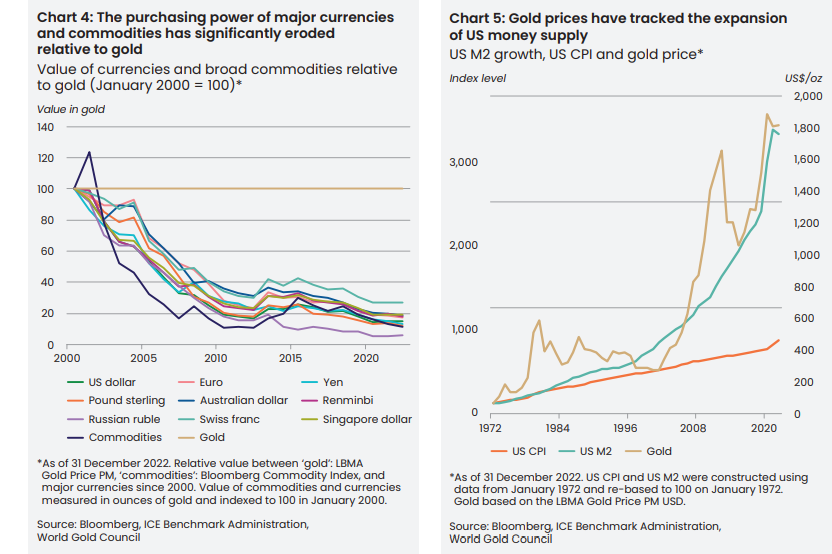

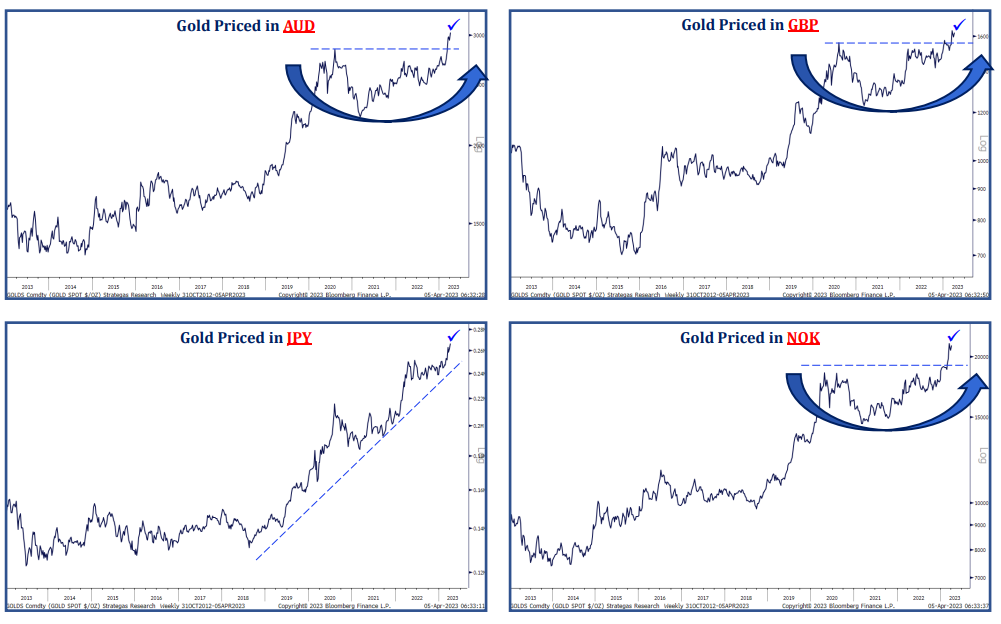

Another benefit of gold is its global acceptance. Given that currencies are no longer pegged or redeemable to gold, the market has the ability to hold governments accountable to actions that impact their currencies. While we typically look at gold vs. US Dollars, there are markets versus virtually all fiat currencies which can be viewed as an overall sentiment gauge on monetary policy across the world.

Source: Strategas. As of 4/10/23.

Source: Strategas. As of 4/10/23.

What Drives Gold’s Long-Term Performance?

Gold’s performance is driven primarily by three main return drivers:

- Long-term interest rates

- The value of paper money relative to real assets

- Fear

In general, gold does well during periods where either easy monetary policy creates rising inflation, or during economic depressions. As a result, gold is best thought of as protection against extreme tail environments rather than providing substantial diversifying qualities for asset allocations during normal times. Gold performs well during the unexpected.

What Drives Gold Short-Term Performance?

Ultimately, fear is the key to short-term gold performance. The potential for large and sudden changes in real rates, debasement risks, sovereign balance sheet risks, geopolitical risks, and general market tail risks all play a part in driving the level of fear in the markets.

These risks have some influence on gold’s performance due to its “safe haven” status. As uncertainty rises, preference shifts towards holding more gold in a portfolio, and drives prices higher. Fear appears to be larger driver of demand than opportunity cost, as measured by the level of short-term US rates (i.e., holding gold forgoes getting paid 4.5%+ in Money Market Funds or Tbills).

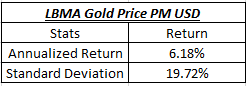

How Volatile is Gold?

Source: Aptus Research (50 year Performance of LBMA Gold Price since 4/1/1973). As of 4/18/23.

Source: Aptus Research (50 year Performance of LBMA Gold Price since 4/1/1973). As of 4/18/23.

Like most asset classes, gold can go through periods of extreme volatility. One only has to look at the period from 2008 to 2013, when gold suffered a 34% decline, a 281% price increase, followed by a sharp 38% retracement. That is a lot of volatility for a “safe haven”!

Given the increased level of volatility in gold, we believe it should principally be viewed as a long-term portfolio component. Surprising to most, gold has had an annualized return of 6.37% over the last 50 years (following the end of the gold standard in 1971). Admittedly, that return was accompanied by substantial volatility.

Real Yields Impact On Gold

Real yields can substantially influence the pricing of gold. Remember the real yield is the yield an investor expects to receive after accounting for inflation. Think of it as the amount of purchasing power an investor (often a conservative investor) expects to gain or lose by holding an investment or cash.

The inflation figure within the calculation is based on inflation expectations, which are a byproduct of the difference between the yield on TIPS and the yield on a nominal Treasury bond of the same duration. Bottom line is when investors get paid a high yield from cash (or cash like securities), it raises the opportunity cost of holding gold.

Theoretically, higher real yields should be bad for the price of gold and vice versa.

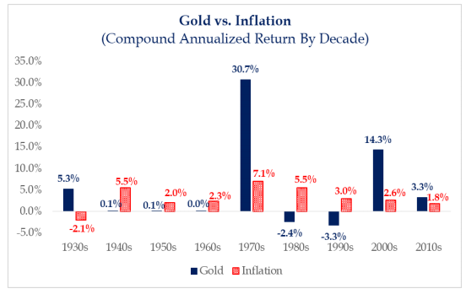

So, Is Gold a Good Inflation Hedge?

Gold is often thought to be a hedge against runaway inflation, but reviewing the relationship between gold and US inflation over the past several decades shows mixed results. Since 1971 (when the US went off the Gold Standard), gold has outperformed the rate of inflation in 3 of the last 5 decades.

Source: Strategas. As of 3/31/23.

Source: Strategas. As of 3/31/23.

The caveat to this point is that over the last 40 years, the US has experienced one of the lowest periods of inflation ever, which limited the need for a “debasement” hedge.

Source: Unlimited Funds. As of 3/31/23.

Source: Unlimited Funds. As of 3/31/23.

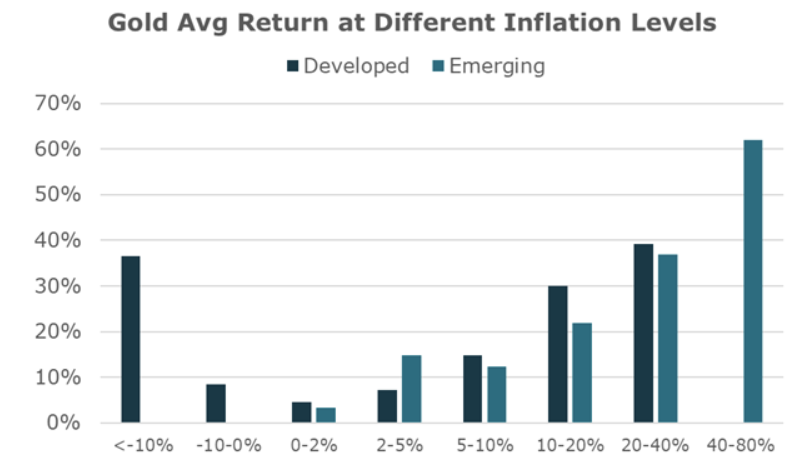

Expanding the dataset to include global data, during periods of significant inflation, gold has historically shown itself to be a solid holding in preserving wealth.

Cases for Owning Gold

Deeply Negative Real Yields

During times of falling or deeply negative real yields (Treasury bond minus the expected rate of inflation), investors are presented with the risk of a loss of real purchasing power. In these times, gold can serve as a reasonable investment tool for portfolios and could offer a substitute for bonds.

Hedge Against Bear Markets

While gold can provide downside protection during equity turmoil, during other periods of economic expansion it can be drag on portfolios, given there are no yield or growth drivers behind the asset class. The size needed for the gold holding to benefit the overall allocation, it could be argued against holding a large position in gold over a full market cycle. Worth noting, viewing gold as a “hedge” creates more correlation risk in a portfolio.

Debasement Hedge (Maintain Purchasing Power)

Gold is of somewhat finite supply especially when compared to traditional fiat currencies. During periods of financial largesse (i.e., money printing), gold can perform well as it’s often viewed as the currency of last resort. During periods of US Dollar uncertainty, investors often seek currency alternatives such as gold for a fear hedge.

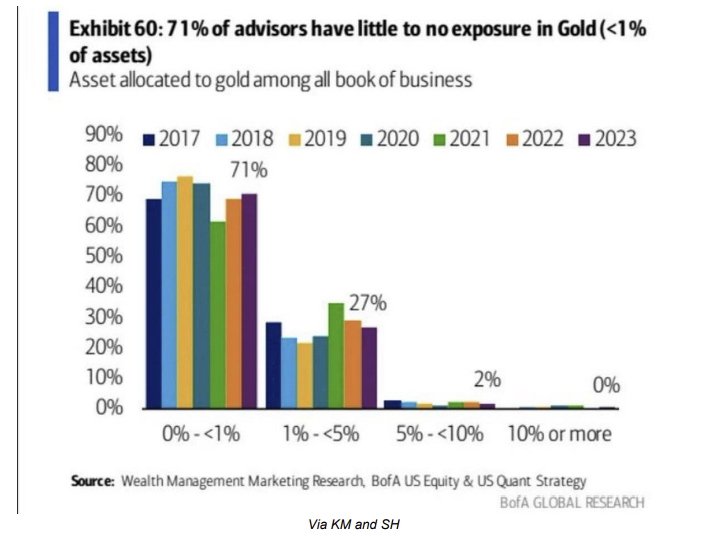

Gold is Massively Under Owned…Although It’s Understandable Why

Source: BAML. As of 3/9/23.

Source: BAML. As of 3/9/23.

Source: Bloomberg. As of 4/18/23.

Source: Bloomberg. As of 4/18/23.

Is there a Thesis for Owning Gold Now?

Gold is an under-owned asset class by both retail and institutional investors, and the environment of late has something to do with that. The last 10+ years have been an environment of low and stable price inflation along with rising equity and real estate prices. Given the period of low inflation and reasonable growth, there has been little need for investors to allocate to the shiny yellow metal.

There is a case to fear the goldilocks period of strong growth and low inflation we’ve been experiencing. This could be changing given the presence of elevated systemic fears, sticky inflation, and recession risks. Many investors see gold’s downside in the case of a soft landing or further Fed hawkishness as less likely or less painful than gold’s upside. Its upside would be an environment where there is a growth shock that pushes the economy into a recession.

Given the possibility for a stagflationary world where growth and inflation could become negatively correlated, the correlation between stock and bond prices would be higher and possibly even positive (as seen in 2022). In that scenario, the value of Treasury bonds as a portfolio hedge would diminish. Theoretically the demand for them would consequently drop while term premiums (the additional requirement over the risk-free rate that investors charge to lend for long durations) would be forced to increase. These factors should drive yields higher until they find an equilibrium. In this environment, it’s likely gold would perform quite well.

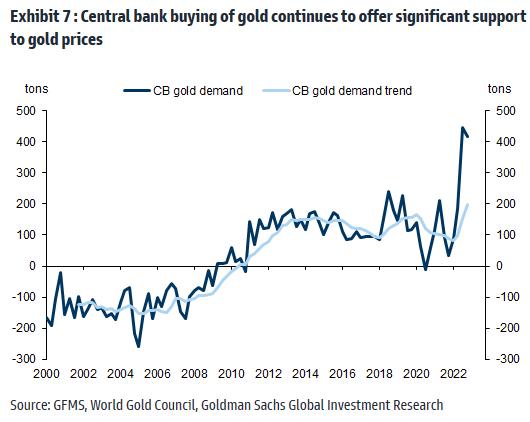

Central Banks are Buying More Gold, Helping Lift Prices

Central banks often own gold as it can be used to diversify a central bank’s portfolio of reserves, reducing its exposure to fluctuations in other currencies or assets. In addition, holding gold can enhance a central bank’s credibility as a signal of a strong and stable economy.

Source: Goldman Sachs. As of 3/31/23.

Source: Goldman Sachs. As of 3/31/23.

Central banks generally view holding reserves in gold as an important part of their overall strategy for managing their balance sheets and protecting their currencies. The proportion of a central bank’s reserves held in gold can vary depending on its individual circumstances and objectives, but many central banks do view gold as an important component of their overall reserve holdings.

It’s no secret that the US holds the privilege of the reserve currency of the world. The chatter of the potential loss of dollar hegemony over the past weeks has been amplified by media pundits. While it’s unlikely that the US loses the reserve currency (see our recent post on the dollar here), it’s reasonable to think our enemies could utilize other sources (like gold) to redirect internal reserves following the US’s seizure of Russian reserve assets.

So, in addition to the losses experienced by foreign US Treasury bond holders last year due to the monumental rise in rates, central banks are faced with the additional dilemma of finding safe places to park reserve assets that both preserve wealth (purchasing power) but also secure sovereign assets from outside intervention (i.e., freezing of Russian assets).

Pitfalls of Gold

Valuing Gold

Investors typically look to real interest rates and the dollar index (for US investors) in analyzing gold’s value. While this has historically worked well, there are other factors that influence the price of gold, such as macroeconomic drivers and supply and demand for the metal. This can lead to significant volatility for gold holders, as illustrated earlier in this note.

Gold vs TIPS

Gold competes with all assets but most closely with those that resemble it best – a perpetual asset that holds its (real) value over time and has no credit risk. In this case, sovereign US inflation-protected bonds are the closest observed proxy for such an asset. TIPS returns are based on Real Yields + an Inflation Adjustment. Since these assets compete with gold for potential allocations, when real yields rise making TIPS a real alternative, gold historically performs poorly (and often very poorly).

Opportunity Cost vs. Cash

Given the current yield environment, a long-term allocation to gold or precious metals could prove less efficient given its opportunity cost vs cash. Plus the associated volatility of gold.

Low Returns and High Volatility on a Standalone Basis

Over the last 50 years, gold has averaged just over a 6% return with a standard deviation of near 20%. Those aren’t typically the type of risk adjusted returns you are jumping at to add to a portfolio.

Source: Bloomberg. As of 4/18/2023.

Source: Bloomberg. As of 4/18/2023.

As evidenced above, if you purchased gold in September of 1980 at $666, it took you roughly until September of 2007 to break even just in nominal terms. 27 years of pain and agony while serving as a very poor preserver of purchasing power. While the highlighted dates are somewhat selective (i.e., the height of the inflation scare of the 70s/80s), we can’t overlook that investors flock (performance chase) to the best performing assets at the worst possible times.

To Conclude

Gold can offer benefits to portfolio construction when considering a full market cycle investment horizon. Some of the beneficial characteristics of gold are as follows: a) broad marketplace demand given limited supply; b) historic protection from extreme market events (i.e., tails) such as high periods of inflation or devalued currencies; c) a component of portfolio diversification; and d) a source of liquidity and versatility in times of chaos.

While gold is a controversial asset and certainly not a great long-term accumulator of wealth (i.e., there are no cash flows and no growth) it’s reasonable to assume it can serve as storage of wealth over long periods of time. While there are other portfolio diversifiers that can add value when constructing portfolios, adding gold to the mix of a long-term asset allocation could make sense.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2304-23.