Fed Chairman Jay Powell finally delivered his long-anticipated address to leading economists and academics. A few quotes that caught our attention, not to mention the market’s attention:

“In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation… Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”

“Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.”

“Labor supply has softened in line with demand, sharply lowering the “breakeven” rate of job creation needed to hold the unemployment rate constant. Indeed, labor force growth has slowed considerably this year with the sharp falloff in immigration, and the labor force participation rate has edged down in recent months.”

“The stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance. Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”

“At the same time, GDP growth has slowed notably in the first half of this year to a pace of 1.2 percent, roughly half the 2.5 percent pace in 2024 (figure 3). The decline in growth has largely reflected a slowdown in consumer spending.”

“The effects of tariffs on consumer prices are now clearly visible. We expect those effects to accumulate over coming months, with high uncertainty about timing and amounts. The question that matters for monetary policy is whether these price increases are likely to materially raise the risk of an ongoing inflation problem. A reasonable base case is that the effects will be relatively short lived—a one-time shift in the price level.”

Our Cliffs Notes

- Fed Chair Powell accepted the market’s argument that the labor market is weakening and that it is a larger threat to the economy than tariff-related inflation. July Non-Farm Payrolls (along with big revisions), and a continual tick up in claims, had to catch his attention, and he finally admitted this to be a concern.

- Inflation has risen in some regards, but less than feared, and tariff impact is likely a one-time thing.

- Once you open the door like this, it’s nearly impossible to walk back. We’re going to get some cuts!

- Data-dependent comments are likely in reference to 2026 and beyond, as I anticipate the Fed will give the market what it wants (2 to maybe 3 cuts) in the back half of this year.

Market Reaction

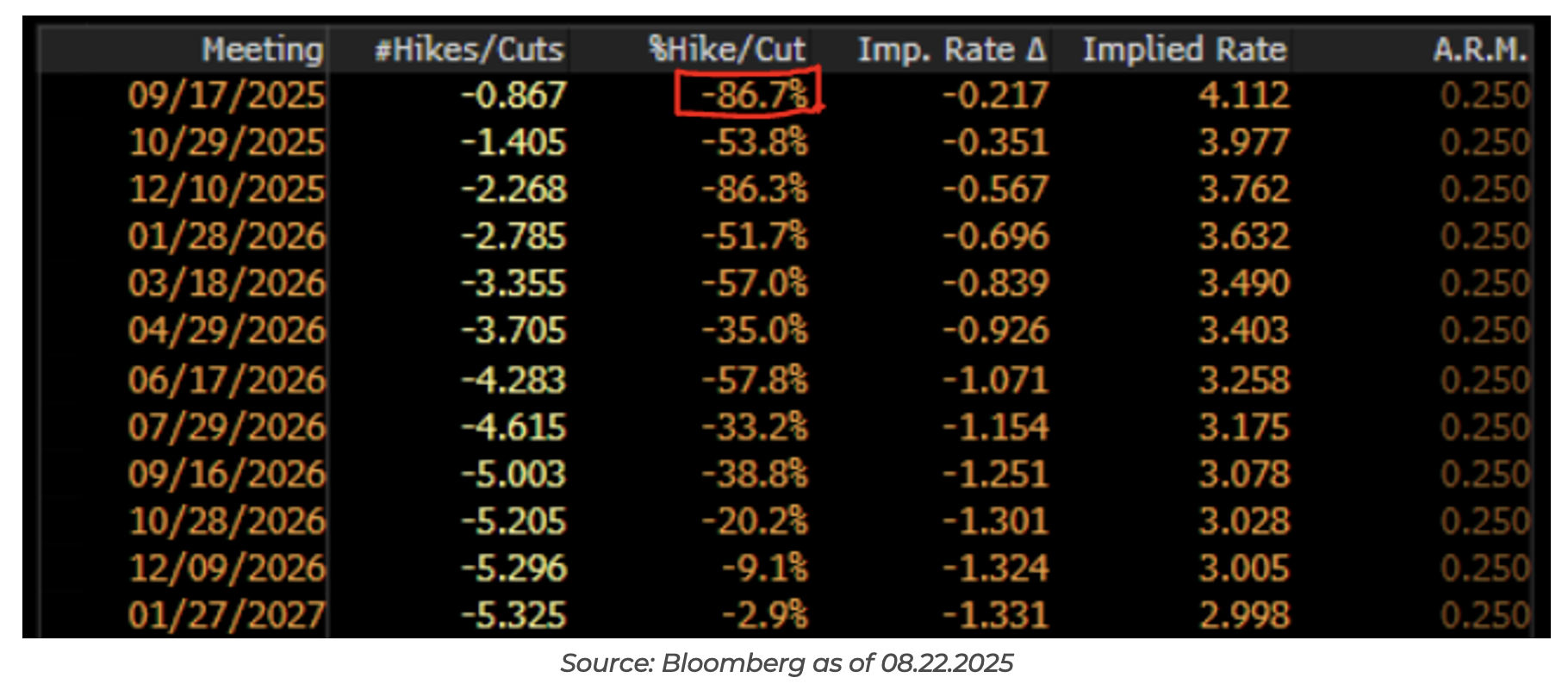

Interest rate markets are projecting roughly a 90% chance of a 25bps cut in September and slightly over 2 cuts for the rest of the year. September rate cut odds sat in the low 70% range coming into today. Markets are reacting as you’d expect risk assets higher, bond yields lower, and USD weaker.

If you think the Fed is ahead of the curve in terms of acting prior to the labor market deteriorating, this “Powell Pivot 3.0 (or whatever the number is)” is likely bullish for risk assets (and lower bond yields). If you think the Fed is late for the party and reacting to bad data that is about to get worse (unemployment rate quickly over 4.5%), typically rate cuts in the face of economic deterioration haven’t historically been a good thing. We’re in the “this is an insurance cut” camp, not the “reaction” camp.

If we take a look at the reaction from the long end (10-year yield) and the shape of the yield curve following today’s speech (back to normal, upward-sloping curve), we can presume the market is telling the Fed this was the correct move. Many were worried we’d experience the same reaction function as last time the Fed cut last year, when the long end proceeded to sell off drastically. While it’s too early to declare victory, we were happy to see the long end “play ball” with the dovish rhetoric from Powell, as we are likely to soon enough restart the cutting cycle.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2508-24.