In 1977, the U.S. Senate Select Committee on Nutrition and Human Needs released its Dietary Goals for the United States. The recommendations were straightforward. Eat less fat and replace those calories with carbohydrates.

The guidelines were framed as cautious, conservative, and protective of public health. The food industry reformulated everything. Low-fat became a marketing badge. School lunch programs, hospital cafeterias, and federal nutrition programs all aligned around the new guidance. Hundreds of millions of Americans followed the advice in good faith over the next four decades.

The result was the worst public health outcome of the modern era.

Obesity rates have roughly doubled, Type 2 diabetes rates have risen to levels that strain our healthcare systems, and metabolic disease has become one of the leading drivers of mortality in the country. The cautious recommendation, repeated across billions of meals, produced exactly the outcome the recommendation had been designed to prevent.

The recommendation to cut fat had been correct on its own terms. What was missed was that the replacement, sugars and refined carbohydrates in particular, did more cumulative damage than the fat they replaced. The visible problem (heart disease in the 1970s) was real, but the intervention designed to solve it created a different, slower, larger problem that was invisible until enough time had passed.

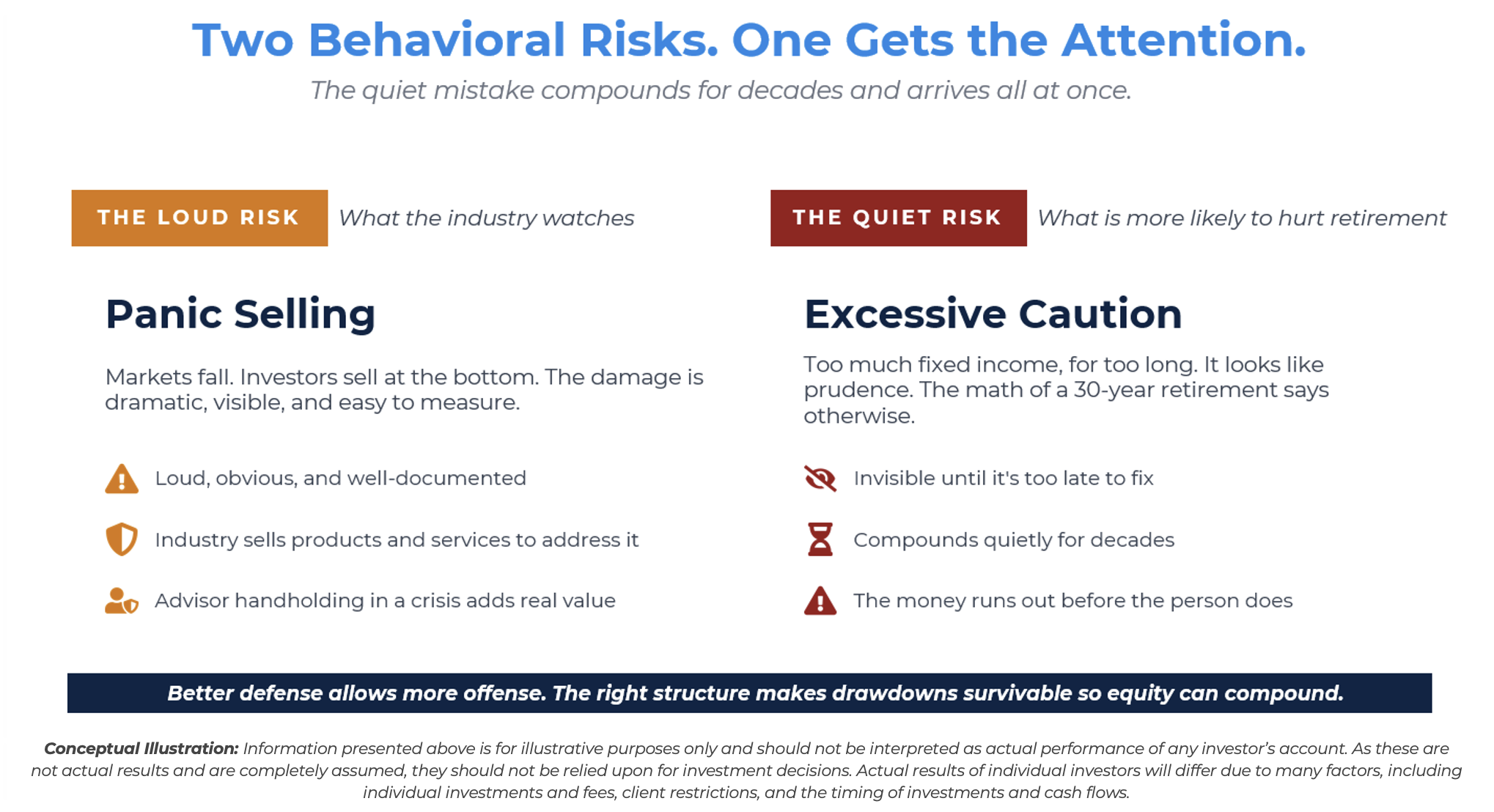

The Investment Industry has a Similar Measurement Problem

The headline behavioral failure is panic. Markets fall, investors sell. Markets rise, investors buy back. Thus, the industry has focused on selling products and services to help clients stay invested. The problem is real, and advisor handholding in a crisis does add value. But the investment clients stay in may not be the right ones in the first place.

The bigger behavioral mistake may be the opposite of panic. It is being too careful, for too long, with too much.

The 55-year-old who moves to 100% bonds the day she retires. The 50-year-old who has held 30% in cash since 2008. None of these decisions feel dangerous. They feel like prudence. But the math of compounding through low real returns and high taxes, across a thirty-year retirement, is brutal. The portfolio can arrive too small, and run out too soon.

That is longevity risk.

Because it looks like prudence, it compounds quietly for decades and arrives all at once, in the form of a retirement that has to be downsized.

Solving for Both the Short and Long-Term Risks

The 1977 guidelines treated nutrition as a single dial. Less fat. The industry treats retirement risk the same way. Less equity. In both cases, the dial is wrong.

We believe the structural answer to longevity risk is not less stocks and more bonds; the answer is more stocks and less bonds, at a similar level of risk. The way to get there is not less engine. It is better brakes.

That is what options-based diversification is designed to do. True diversification, sourced from convexity rather than from a bigger bond allocation, makes drawdowns more survivable. A more survivable drawdown is a drawdown that the investor can actually sit through. An investor who can sit through drawdowns can afford to hold more equity for longer, which may be the only reliable answer to a thirty-year retirement.

Better brakes allow a bigger engine. The same risk budget, spent differently, builds a bigger portfolio and a longer runway.

The 1977 mistake was not cutting fat. It was measuring fat intake for forty years, while metabolic disease did the real damage. A portfolio that defaults to “safety” fails the same way. Short-term volatility is the easy thing to measure. Whether the money grows enough to get there, and lasts once it does, is the thing that we believe matters.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2605-17.