We wanted to put together a note to discuss the recent underperformance of municipal bonds relative to their taxable brethren (MUB vs AGG, shown below). Tax-free bonds have faced a number of headwinds throughout 2025, and even with the decline in interest rates, they sport a negative total return YTD, a sharp performance divergence from the Aggregate bond index.

We believe there are several factors that have impacted market sentiment on the asset class, and we will list our interpretation of why Munis have struggled and some thoughts on why the backdrop could provide an opportunity for future return potential.

Key Drivers to Muni Underperformance

- Supply- Year-to-date, there has been a surge of new supply of municipal debt. Post-COVID, many municipalities were flush with government stimulus money, which led to low municipal debt issuance. This trend has reversed as municipalities need to shore up their funding needs while also investing to improve aging infrastructure.

- Tax Status- Commentary from the Trump administration on pulling back the municipal bond tax exemption. In our opinion, this is a very low probability event. Municipalities often attract capital from local investors who wish to invest in their communities while receiving a tax incentive. Often, the spread difference between a municipal bond and a Treasury bond of equivalent duration is notable. The tax-exempt benefit (especially for high tax bracket investors) provides a reasonable after-tax return for investors while also providing better financing terms for the municipality. Restructuring the status quo of the Muni market is unlikely.

- Federal Spending Reform- Government assistance programs for municipalities have been in the crosshairs. President Trump and his administration have proposed recommendations for FEMA regarding the share of incidents covered by Washington, DC. The federal government has received a rising share of the bill over the last 50 years since FEMA’s inception (well over the 75% long-term average). This could shift some of the cost burden onto state and local governments. We believe this is manageable.

- Lower Tax Rates- Banks have seen fewer active buyers in the municipal sector following corporate tax cuts. The tax rate drastically impacts the tax-equivalent yield on municipal bonds. Lower tax rates mixed with tighter spreads relative to Treasuries have left Munis less attractive relative to other investments.

- Banker Risk Appetite- Banks have been hammered with losses within their fixed income portfolios as interest rates have risen. Lower tax-equivalent yields, a very attractive short-term alternative (T-bill and chill isn’t just a retail strategy), and better lending opportunities have lowered the appetite for municipal investment.

- Reduced Banking Cash Flow- the cash flow profile of banks has been impacted by rising rates. Banks like to buy cash flowing assets (e.g., mortgage bonds) where they receive monthly principal and interest payments giving them optionality for reinvestment. Given the large increase in interest rates, mortgage prepayment and refinances have slowed drastically, lessening the cash flow pool of investable assets for Munis.

- Fewer Calls- Given the higher interest rate environment, a lower fraction of bonds have been called prior to maturity (a typical municipal bond structure involves an optional call feature exercisable by the issuer). Many of the bonds at market were issued at yields well below the current “market yield”, making it unwise for issuers to call the bonds. This dynamic created excess demand on limited supply of Muni bonds. This appears to be correcting; we are seeing more municipal bond supply and higher yields/ spreads.

Summary

Looking back, the municipal market was relatively expensive coming into 2024, given many of the points detailed above. Many of the supply/demand imbalances in the municipal market are improving, and it could be argued that they have been overdone. Participants seem to agree, as the spread and yield levels have enticed greater participation in the municipal market from relative value/crossover buyers, which we view as a good sign.

We believe the current positioning of the municipal market, specifically with bonds in the 5-10 year duration range, appears to offer attractive tax equivalent yields (for high tax bracket investors) and strong interest rate risk protection relative to their taxable cohort. Additionally, as these bonds season, we believe they have strong roll-down (the yield curve) potential, which can make future return potential particularly attractive.

Looking Ahead

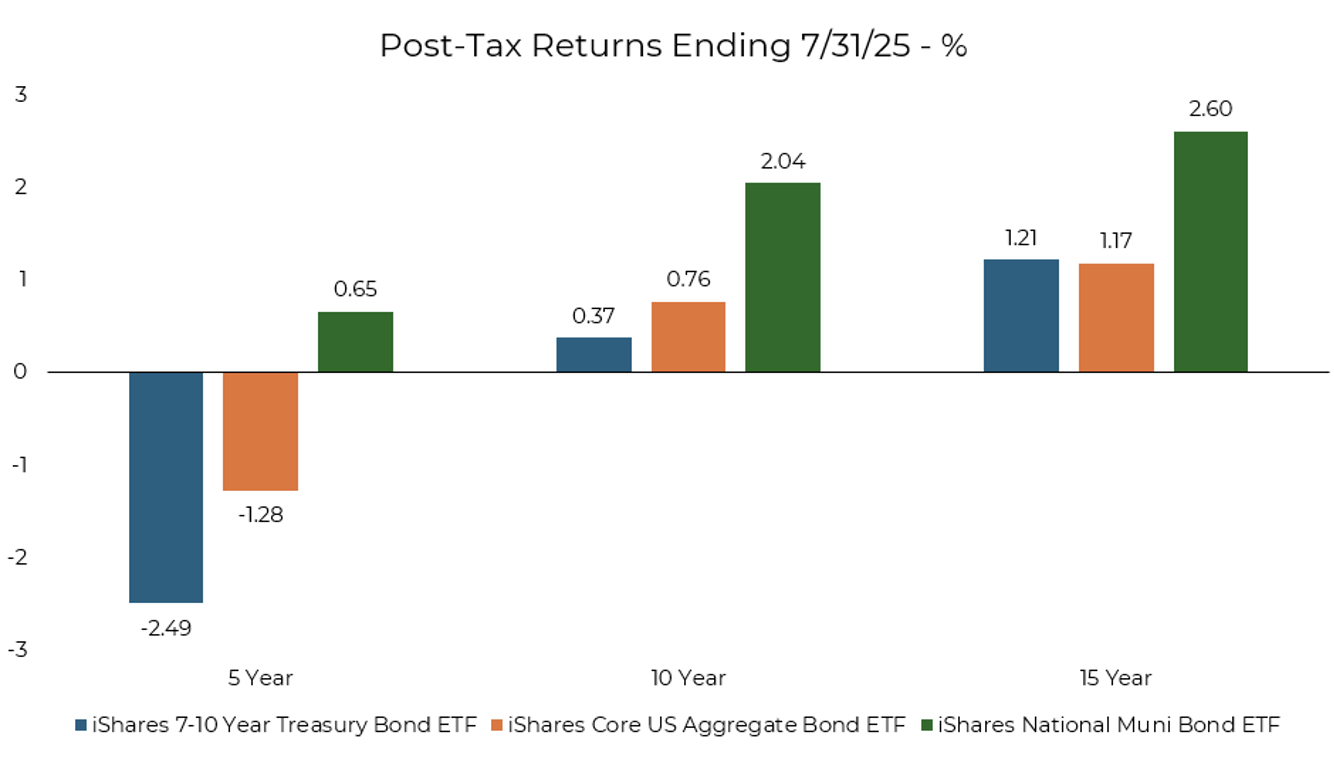

Historically, municipal bonds have shown better after-tax returns for high tax bracket investors.

Source: Aptus via Morningstar as of 07.31.2025

Source: Aptus via Morningstar as of 07.31.2025

Additionally, they have shown a moderately uncorrelated return profile versus other risk assets during times of market chaos. Looking ahead, we anticipate municipal bonds will continue to provide value to tax-sensitive investors’ portfolios as they patiently clip their coupons and ride out the recent underperformance.

Disclosures

* Morningstar’s Tax Cost Ratio (TCR) is built on the fund’s after-tax returns, which themselves are calculated assuming investors pay the maximum federal tax rates on both ordinary income (which includes non-qualified dividends, interest, and short-term capital gains) and long-term capital gains/qualified dividends, including the 3.8% Net Investment Income Tax (NIIT). The methodology explicitly assumes the highest applicable tax rates across these categories. admainnew.moringstar.com +10

To break it down:

-

- Ordinary income / short-term gains / non-qualified dividends are taxed at the top ordinary income rate, which Morningstar treats as 40.8% (this includes the NIlT). Advisor Perspectives +1

- Qualified dividends / long-term capital gains are taxed at the maximum long-term rate— typically 23.8% (20% long-term capital gains + 3.8% NIIT).

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2508-21.