With the recent increase in the use of option strategies around concentrated stock positions, we wanted to measure the benefits of using shorter-tenure options that are actively managed over time during extreme price fluctuations compared to the more common longer and passive approach. With NVIDA (ticker NVDA) stock up more than 1,800% over the last 5 years, we found a case study on NVDA to be a great place to start.

Whether the concentration in NVDA is spurred from employee stock compensation or investor capital appreciation, it is very common for individuals to seek yield from a large position that otherwise pays a miniscule dividend. A covered call strategy is a common way to meet a client’s income need. A covered call strategy is implemented when a client sells out-of-the-money calls on a stock that they own. By selling a call, the client enters into a contract where they are paid an upfront premium in exchange for the obligation to sell the stock at a specified price in the future. Put more simply, the client is compensated today for giving up future upside in the underlying stock.

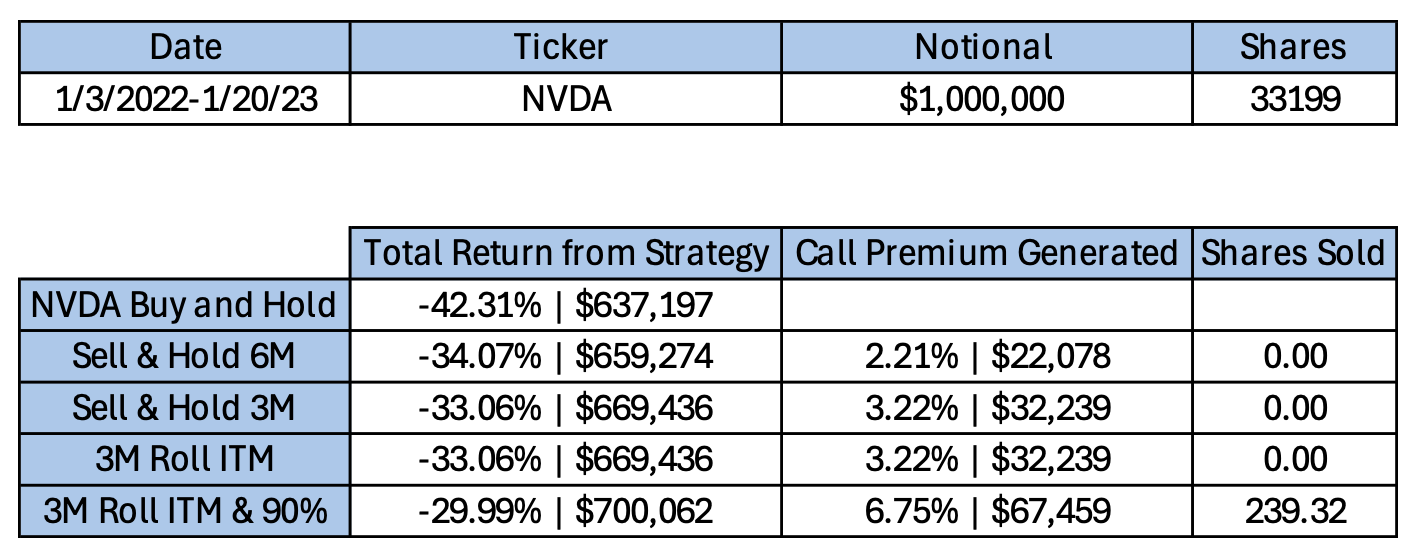

In the case study below, we compared four different covered call strategies on NVDA stock over 2022 and 2024 and measured the strategies total return, call premium generation and total shares needed to be sold to buy back the calls. We selected these time periods because they represent drastically different performance with NVDA down -42.31% from 1/3/22 to 1/20/23 and up 189.50% from 1/3/2024 to 1/17/2025.

Overview of Strategies

1. Sell & Hold 6M: Sells 6-month calls, rolling at expiration

2. Sell & Hold 3M: Sells 3-month calls, rolling at expiration

3. 3M Roll ITM: Sells 3-month calls and rolls when the stock price closes ITM or at expiration

4. 3M Roll ITM & 90%: Sells 3-month calls and rolls when the stock price closes ITM, closes with the option at a 90% gain or at expiration

All four of the strategies sell the closest option to a 10 delta at the time of the implementation (using closing data). Delta is defined as the expected change in the price of the option for a $1 move in the underlying stock price and is often used as an estimation of the likelihood of the option finishing in-the-money (ITM). So, a 10-delta call is estimated to finish ITM 10% of the time. This is a fairly conservative call sale that is often used when looking to generate income with the goal of retaining stock.

If the call option is ITM at expiration, we buy back the call to avoid delivery and sell the minimum number of underlying shares needed to pay for the purchase. We will then sell a new 10 delta call with the strategy’s target tenure.

Bull Market Analysis (1/3/2024-1/17/2025)

Key Observations

Total Returns

-

- The passive Sell & Hold 6M strategy significantly underperformed, capturing only 37% of NVDA’s upside and generating only 3.47% in annualized premium.

- Active strategies like 3M Roll ITM (+154.13%) and 3M Roll ITM & 90% (+152.60%) retained much more upside while generating substantial premium income.

Call Premium Generation

-

- Shorter-term strategies generated significantly more premiums due to the higher number of rolls.

- The most active strategy (3M Roll ITM & 90%) generated $156,050 in call premiums—more than quadruple the passive Sell & Hold 6M ($34,710).

Shares Sold

Passive strategies required selling more shares to buy back options when they were in-the-money.

-

- Sell & Hold 6M sold nearly half the initial position (8,974 shares) to avoid delivery at expiration.

- Active strategies reduced the need to sell shares significantly with the 3M Roll ITM selling only 3,473 (61% fewer than the Sell & Hold 6M).

Bear Market Analysis (1/3/2022-1/20/2023)

Key Observations

Total Returns

-

- All covered call strategies mitigated losses through premium generation compared to “Buy and Hold” (-42.31%).

- The most active strategy (3M Roll ITM & 90%) limited losses to -29.99%, outperforming the 3M passive approach by ~3%.

Call Premium Generation

Active management significantly increased income during the downturn.

-

- Passive strategies like Sell & Hold 6M generated only $22,078.

- Active management (3M Roll ITM & 90%) generated nearly triple ($67,459).

Shares Sold

-

- Share sales were minimal during bear markets due to lower volatility and fewer in-the-money options.

- Only the most active strategy (3M Roll ITM & 90%) required selling shares (239 shares).

Summary

This case study demonstrates the potential benefits of short-term and actively managed covered call strategies, particularly when applied to higher-volatility names like NVDA. The results showed that more active, shorter-term strategies outperformed passive, longer-term approaches in terms of total returns, premium generation, and share retention.

In the NVDA bull market of 2024, active strategies retained significantly more upside potential while still generating substantial income. During the NVDA bear market of 2022, these strategies provided better downside protection through increased premium generation. Overall, the study suggests that investors with concentrated stock positions may benefit from adopting more dynamic covered call strategies, which can adapt to changing market conditions and potentially optimize both income generation and capital appreciation.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2503-27.