As this is being written, WTI crude oil trades at $96.13/bbl (per barrel); the last time oil closed that high was 2014. Of course, given recent events and the inherent volatility in oil, price could easily be >$100 or <$90/bbl by the time this piece is published and read. Either way, after eight years of sub-$80/bbl oil (with the majority of time spent below $60/bbl), we now find ourselves in a completely different environment driven by a confluence of forces, several of which may stick around longer than people expect.

Russian/Ukrainian Conflict

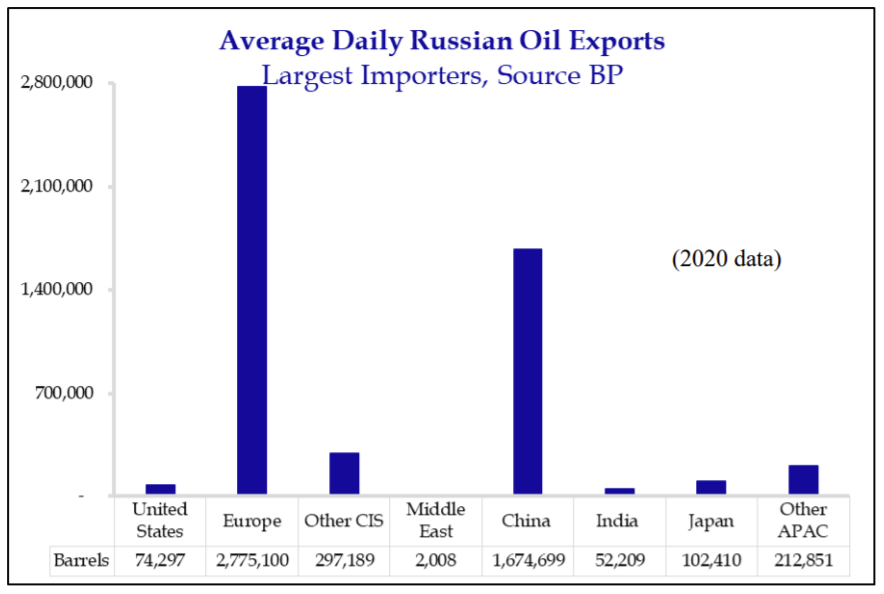

It is difficult to understate the importance of Russian oil, not only to western Europe, but to the world. According to the February 2022 OPEC Monthly Oil Market Report, Russia is the second largest global producer of oil at 9.95 million barrels per day (MBls/d), behind the US at 11.75 Mbls/d with Saudi Arabia a near tie at 9.87 Mbls/d (Nov. 2021 production numbers). To further put this in context, Russia’s share represents right at 10% of global supply. However, unlike the US, which consumes far more oil that it produces, Russia is a large net exporter, meaning that the majority of that nearly ten million barrels of oil each day is being consumed by other parts of the world. The primary beneficiary is Europe, although some of that oil makes it over to the US as well (7% of total November 2021 crude imports to be exact, per the US Energy Information Administration).

Source: Strategas Securities, LLC, as of 02.28.2022

Source: Strategas Securities, LLC, as of 02.28.2022

Disruption of these flows would wreak havoc on global supply, which is why foreign countries who have sanctioned everything from Russian banks to private citizens’ assets abroad have fallen short of denying Russia a market for their most valuable natural resource. Amos Hochstein, the State Department’s senior energy security adviser, said in an interview last Friday that, “sanctions will not target the oil flows as we go forward,” simply because this would be deemed more of a punishment for US and European consumers than it would Russia. Hochstein elaborated, “If we target the oil and gas sector for Putin, and in this case the Russian energy establishment, then prices would spike. Perhaps he would sell only half of his product, but for double the price. That means he would not suffer the consequences while the United States and our allies would suffer the consequences.”

Given Russia’s place in the global energy scene, it isn’t at all surprising that oil markets would wake up at the sight of heightened geopolitical tensions. Indeed, allowing some sort of premium to account for the thought that the commodity could be used as a weapon in this war makes rational sense. However, while this will certainly drive near-term movements in oil, we don’t believe this is the primary reason to be bullish over the long-term.

Global Supply/Demand Fundamentals

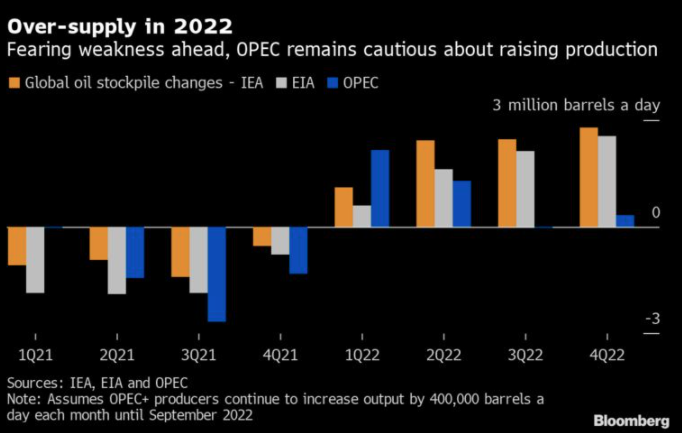

Coming in to 2022, the three major energy forecasting agencies (US Energy Information Agency – EIA, International Energy Agency – IEA, Organization of the Petroleum Exporting Countries – OPEC) all expected that 2022 would be the year when increasing oil supply would outstrip demand and inventories would reverse their decline, leading to more normalized prices. At the end of third quarter 2021, this is where they all stood:

Source: Bloomberg, as of 02.28.2022

Source: Bloomberg, as of 02.28.2022

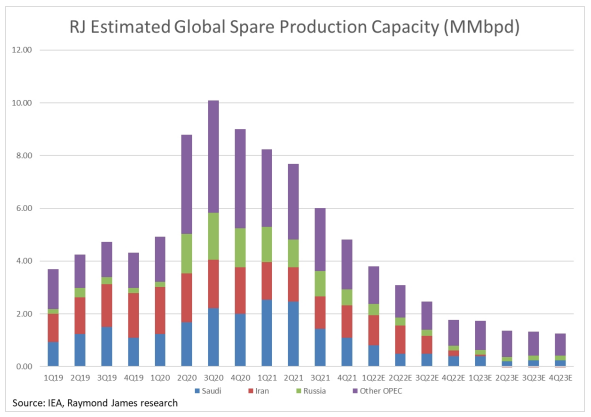

Since that time, the outlook has tightened considerably. The IEA has increased its 2022 demand forecast by 900,000 bls/d, citing a milder-then-expected negative impact from the Omicron variant and a weather-driven switch to oil from gas for residential heating and industrial needs. Moreover, while OPEC+ has continued its pledge of adding 400,000 bls/d per month through September 2022 (the gradual rolling-off of COVID-era cuts), they have repeatedly fallen short of that mark due to several member nation’s inability to ramp production from existing capacity. Regarding that point, the IEA noted that unless OPEC+ member nations with spare capacity (namely Saudi, Iraq and UAE) make up for the production deficits of the broader group (namely Angola and Nigeria), the total amount of oil lost in 2022 could approach one billion barrels! The COVID pandemic not only drove oil prices lower than we’ve seen in years, it disincentivized investment in new production, which has now become apparent even in those countries that were believed to have ample ready inventory.

Source: Raymond James, as of 02.28.2022

Source: Raymond James, as of 02.28.2022

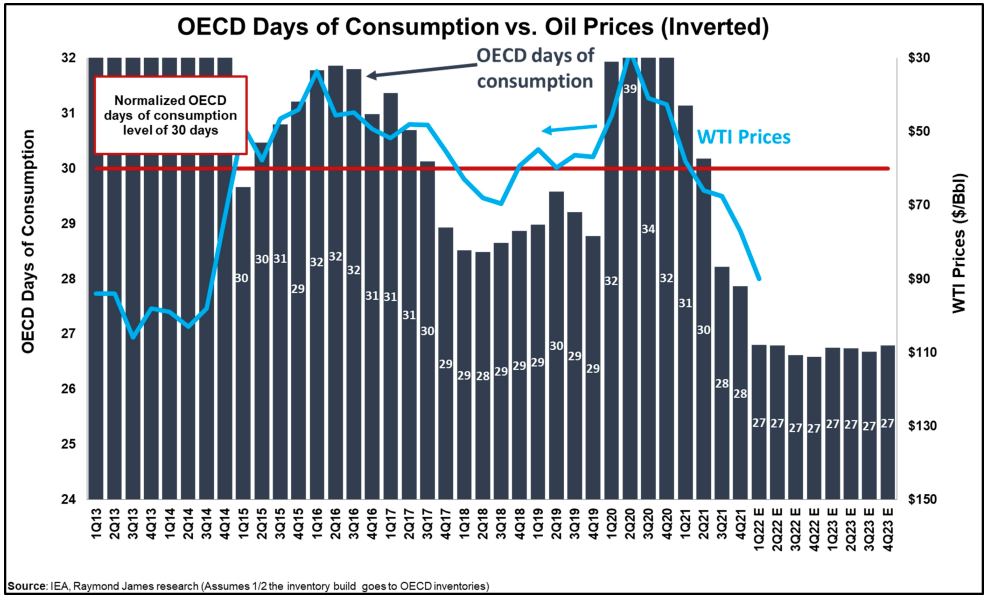

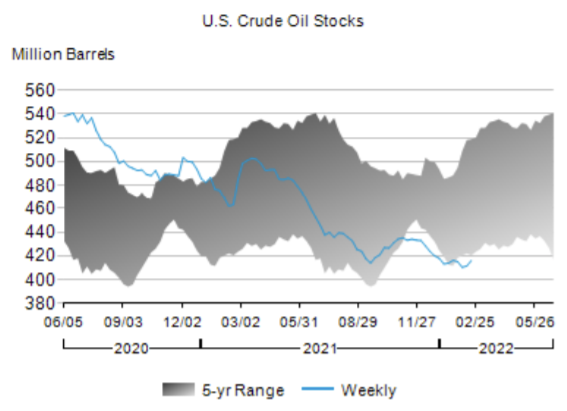

All of this wouldn’t be overly concerning in a normal environment, but global inventories are currently lower than normal. Even if markets return to a surplus in 2022 (which is looking less certain than it did a few months ago), the added supply will only serve to put a small dent in depleted inventory levels. This is being seen globally, as well as here at home:

Source: Raymond James, as of 02.28.2022

Source: Raymond James, as of 02.28.2022

Source: US Energy Information Agency, as of 02.28.2022

Source: US Energy Information Agency, as of 02.28.2022

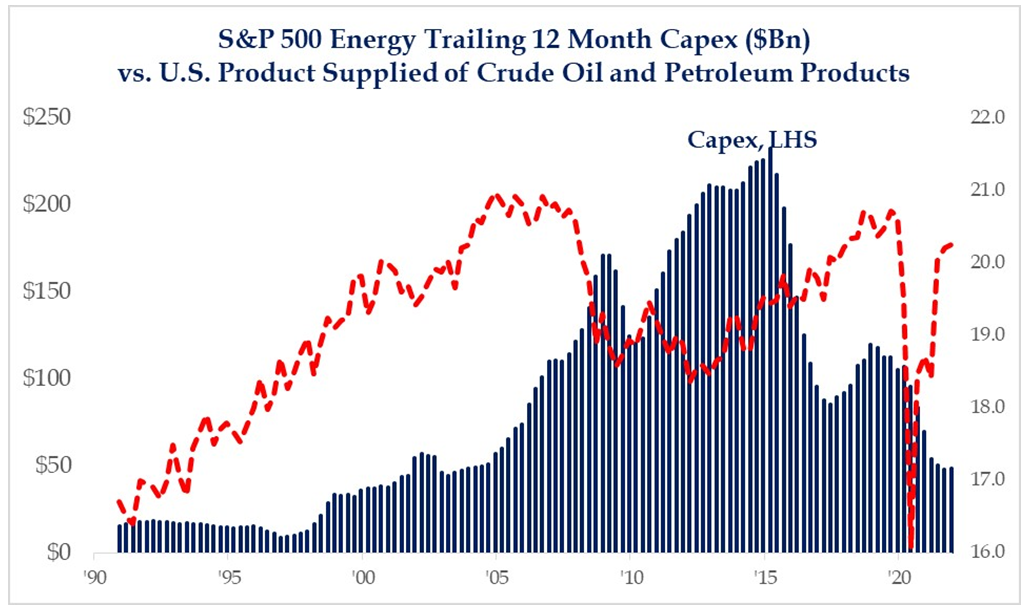

Speaking of here at home, how are US producers responding to the jump in commodity prices? As the largest producer of oil and liquids (includes condensate, natural gas liquids) in the world, certainly the US has the ability to influence global supply. The answer is two-fold: yes, activity has increased, leading to greater production domestically; but no, companies are not responding with the frantic growth-at-all-costs proposal of past cycles. This point was driven home in an interview post 4Q’21 earnings announcement with Scott Sheffield, CEO of Pioneer Natural Resources – one of the largest independent E&P companies in the country and largest acreage owner in the prolific Midland Basin. When asked about increasing output in response to elevated oil prices, he responded, “Whether it’s $150 oil, $200 oil, or $100 oil, we’re not going to change our growth plans.” This is coming from a guy who expects oil prices to climb higher, as demonstrated by the fact that Pioneer bought out their entire 2022 oil hedge book in 4Q’21 in order to have unfettered upside exposure to the commodity going forward.

To be fair, not everyone is following suit. Financial discipline has been witnessed primarily at the public company level, where shareholders are demanding the return of capital over reckless growth (still marred by the capital destruction days of the 2010’s). But after years of industry consolidation, private companies only represent ~30% of US oil production, down from over 60% several years ago¹. That means that lower reinvestment rates, even if just at the public level, should keep spiraling production increases in check.

Source: Strategas Securities, LLC, as of 02.28.2022

Source: Strategas Securities, LLC, as of 02.28.2022

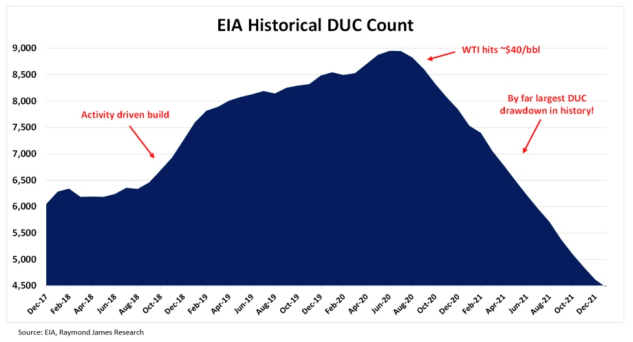

This has resulted in free cash flow generation not seen from the energy sector since 2008. Not only are oil prices high, but companies have become much more efficient operators than they were ten or even five years ago. With that said, this level of underinvestment can’t continue. The primary means by which domestic producers have been able to maintain this level of hydrocarbon output while keeping expenditures in check is that they’ve been drawing on an inventory of discounted flows known as the DUC (drilled-uncompleted) well count. This represents those wells that have been drilled to total depth but not yet fracked and put on production. At any given time, there must be some level of DUC inventory due to the fact that operators often complete several wells in a row to utilize frac fleet efficiency. And during times of lower oil prices (like much of 2015 – 2020), operators are incentivized to drill wells (to utilize long-term drill rig contracts) but hold-off completion until prices improve. Right now, we’re seeing the opposite – DUC’s are being drawn down at a record rate in order to increase production without spending as much money.

Source: Raymond James, LLC, as of 02.28.2022

Source: Raymond James, LLC, as of 02.28.2022

This means the rig count has to go up. It bottomed in July 2020 at 276/1,030 (North America / World) and has since climbed to 886/1,632. This seems like a huge jump but put in the context of the all-time high in 2011 of 2,740/3,722, it pales in comparison. Given the vast increases in drilling efficiency and speed, there is no reason to expect absolute numbers will approach 2011 levels. But it is reasonable to think rig counts must rise to offset natural production declines, stem the drop in DUC count and satisfy global demand.

Conclusion

In terms of energy markets, the conflict between Russia and Ukraine is currently getting all the attention. But as we’ve discussed, there are fundamental issues at work which give us cause to be an oil bull long past the (hopefully soon) conclusion of this war. As COVID reaches the endemic phase, oil demand has come roaring back and is forecasted to surpass its 2019 highs this year². At the same time, we think the chronic underinvestment in oil supply both domestically and internationally has created a situation where demand can’t easily be met in the near-term, at least not in a meaningful way as to build the inventory depletion of the last year. As a result, we remain bullish on oil price and the companies that produce it. We have been overweight energy in our Compounders stock sleeve since the beginning of September 2021 and we seek to maintain that position.

While a global peace would certainly take the hostility premium out of oil, we expect that these longer-term factors should keep the floor above $80/bbl, perhaps for the next year or two to come. Domestic operators have become extremely efficient at producing oil, generating free cash flow at levels below $50/bbl. It is hard to imagine a perpetual environment where that type of economic rent is allowed to exist, and prices should eventually settle around the $65/bbl mark. Until then (and even after), domestic E&P companies generate tremendous free cash flow and have developed shareholder-friendly return policies, making them some of the highest-yielding companies in the index. Moreover, we have gotten more bullish on oil field services, as a dwindling DUC well inventory and the need for more production will drive a higher rig count and related services, even as operators pledge fiscal discipline.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

Advisory services offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2202-35.