Equity markets have recently been dominated by the “Magnificent” few and a relentless bid for high-beta tech. Suggesting that lower volatility stocks can retain their documented long-term benefit feels a bit like advocating for marathon training during a 100-meter dash. It is steady and calculated, but lately, it has been left in the dust.

The Reality of the “Volatility Paradox”

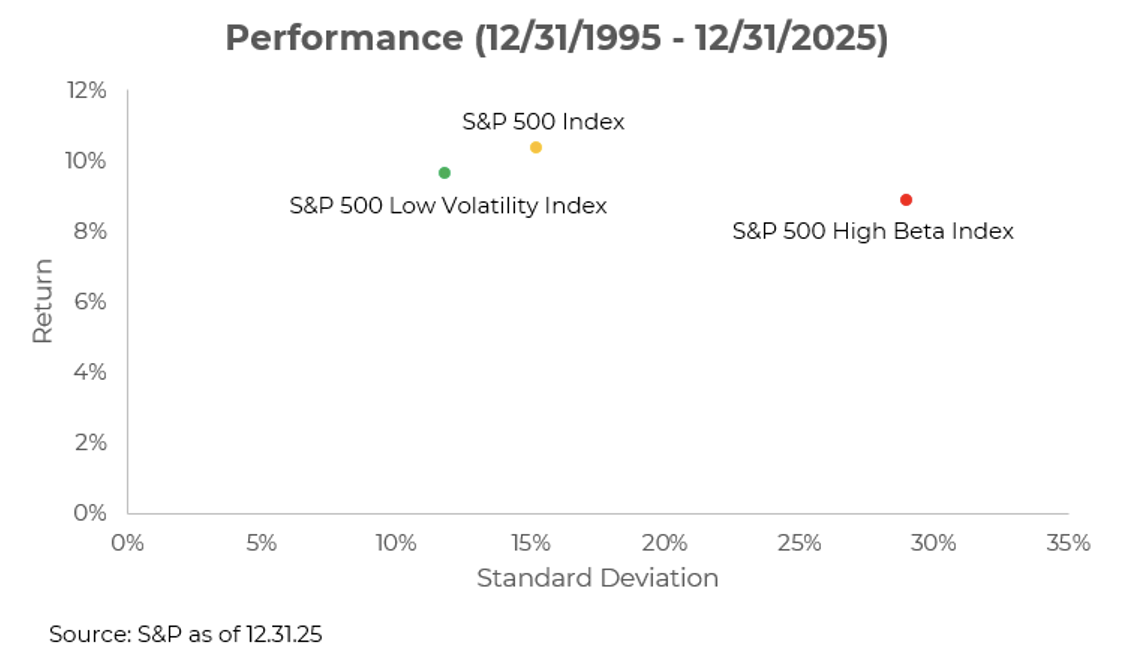

There is a persistent view that to get higher returns, you need to stomach higher volatility. The long-term data tells a different story. If you look at the last 30 years, lower volatility stocks (as defined by the S&P 500 Low Volatility Index) have achieved higher returns than high beta stocks (as defined by the S&P 500 High Beta Index) and been more closely aligned with the broader market in terms of total return.

The secret is the impact of the drawdown… or better said, the lack thereof. High-beta stocks tend to capture the imagination on the way up, but they have captured significantly more of the pain on the way down. By losing less during market corrections, lower volatility stocks often don’t need to work as hard to get back to even. You capture a material portion of the upside with less of the pain.

Why Now? Lessons from History

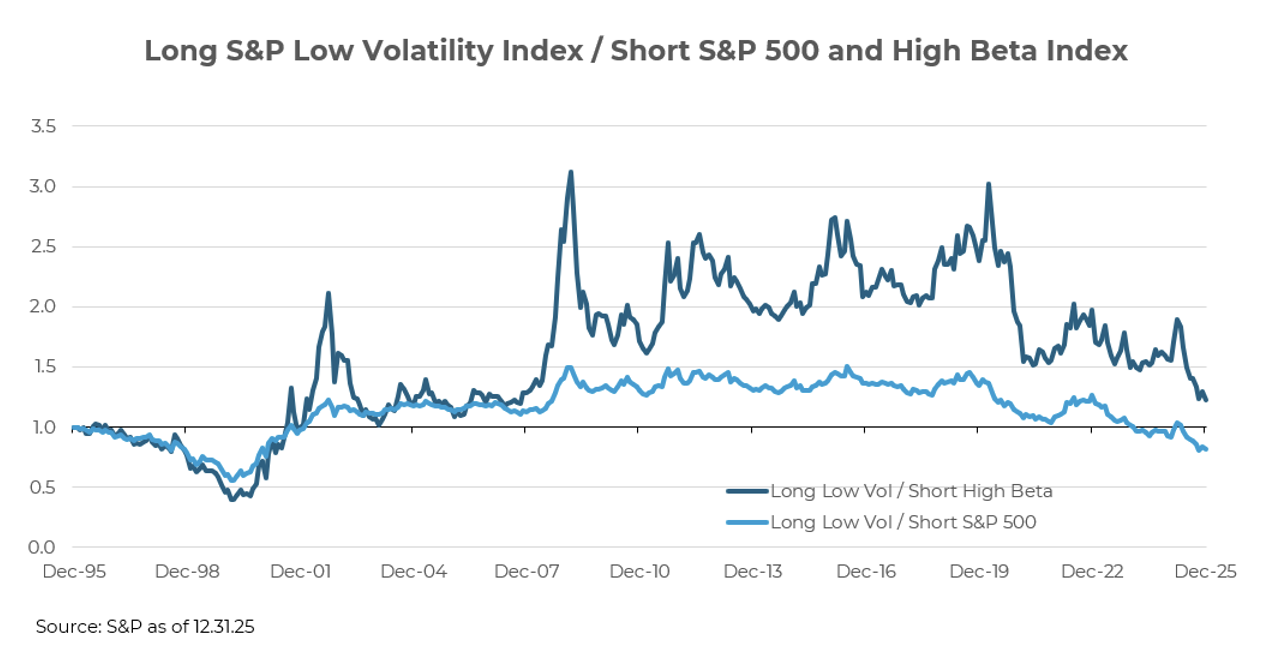

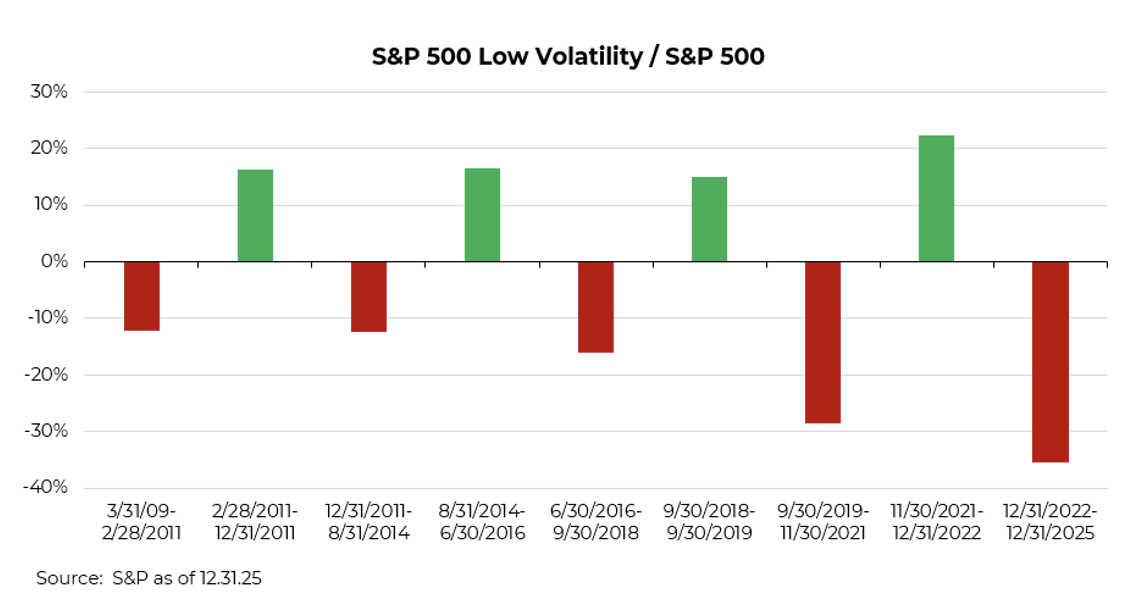

If the long-term case is so strong, why hasn’t everyone piled in? Since 2020, lower volatility stocks have been stranded in the desert.

The Late 1990’s “New Era” Echo

-

- In the late 90s, low-volatility stocks were discarded as “relics of the old economy.” Investors chased dot-com dreams until the math no longer supported the multiples.

-

- The Reversal: When the bubble burst in 2000, low volatility didn’t just protect capital; it thrived on a relative basis for years as investors rediscovered the value of earnings over “clicks” and “eyeballs.”

The 2019 Growth Pivot

-

- Following the post-GFC recovery, high-beta names surged when interest rates were pinned at zero and continued as high beta technology led markets higher, given strong fundamentals.

-

- The Potential Reversal: When high-beta stocks lead by this significant a margin, it often signals “stretched” relative valuations for the highest-risk segment of the market. While momentum can certainly carry prices further in the short term, history shows that these periods of extreme leadership from high-risk names frequently serve as a precursor for a sharp reversal.

We believe the current underperformance of lower volatility may have created a compelling entry point for those looking for equity exposure with a smoother ride.

A Better Way: Multi-Factor Minimum Volatility

We aren’t suggesting you simply buy a basket of utility and consumer staples stocks and hope for the best. The market has evolved and we believe lower volatility exposure should evolve with it. Instead, we advocate for a multi-factor minimum volatility solution. This approach moves beyond simply finding the “quietest” stocks by integrating companies that exhibit both low volatility and strong fundamentals.

Our framework is designed to:

-

- Capture Resilient Themes: Target the drivers behind the tech rally, such as real earnings, solid cash flow, and durable business models.

-

- Filter Out Sentiment: Systematically avoid companies that have participated in market rallies purely on hype, where valuations may exceed what their fundamentals justify.

-

- Prioritize Quality: Ensure that “low vol” doesn’t mean “low growth”, by anchoring the selection in financial strength.

Existing strategies with similar rules, including a core component within our Large Cap Upside Strategy, have generated a similar risk profile to the S&P 500 Low Volatility Index, but with returns more aligned with the broader market.

The Bottom Line

By focusing on “min vol” with a fundamental tilt, we’re looking to efficiently capture a factor that participates in the market’s growth over time, while protecting against the potential “return to earth” for high-premium, high-beta names. Past episodes show that now may be a time when this framework bounces back from recent relative challenges.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2601-31.