A farmer who needs 40,000 gallons of water a day has a few ways to get it.

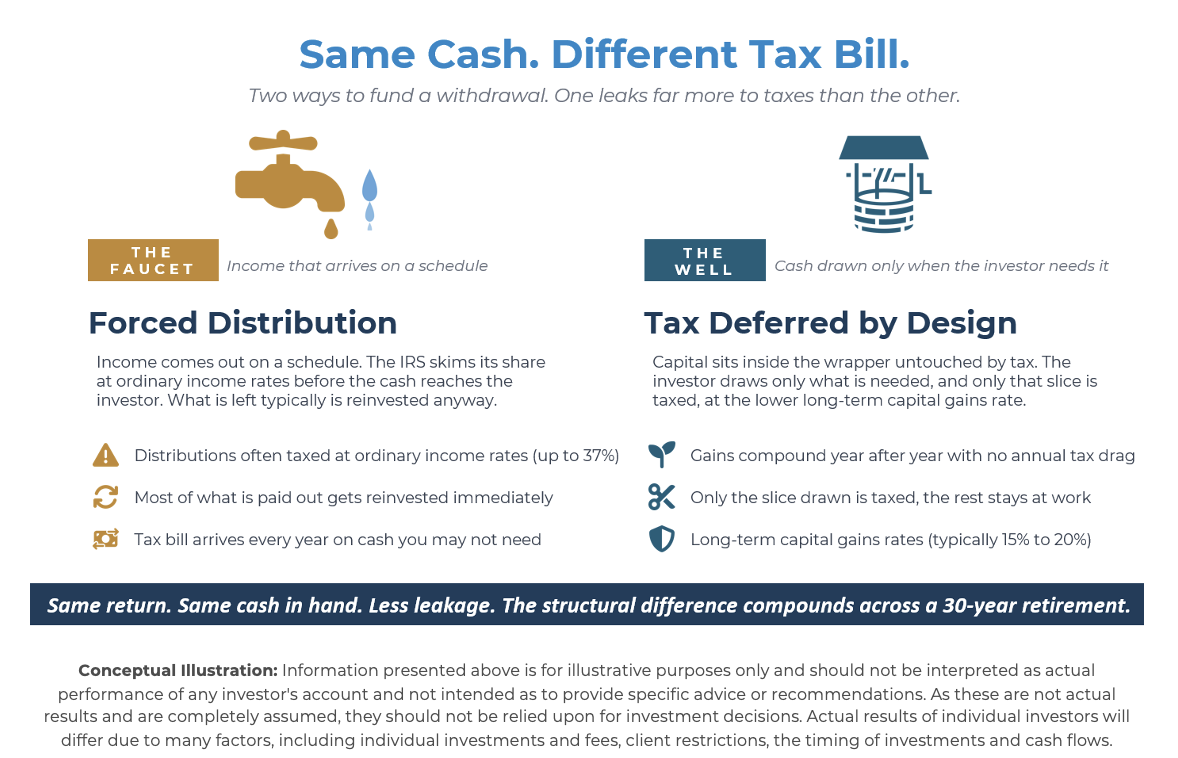

One is a faucet stuck in the on position. Water flows continuously into a trough whether the farmer is there to use it or not. The hot sun overhead evaporates a portion of every gallon on its way down. The trough fills faster than the crops need it. The excess spills over the side and runs off into the field. Most days, the farmer needs only forty thousand gallons. The faucet doesn’t know that. It keeps running. The sun keeps taking its share. The trough keeps overflowing. The water that actually reaches the crops is a fraction of what came out of the spigot.

Another is a well at the edge of the field. The water sits there, cool and sheltered, doing nothing. When the farmer needs water, he pumps it. Only the water he actually pulls up is exposed to the sun, and only for the time it takes to reach the crops. Nothing spills, because nothing was produced that he didn’t need. Nothing evaporates unless he pumps it.

Both deliver forty thousand gallons a day. The faucet loses water to evaporation every day, and loses more to spillage on top of that, because most of what it produces was never needed in the first place.

We believe this is the most important structural difference between income-distributing investments and total-return investments held in a taxable account.

A traditional bond fund is a faucet. Every coupon flows through the IRS first, which takes its share by evaporation before the water ever reaches the investor’s trough. What is left then has to go somewhere. Roughly 90% of fund-level distributions are immediately reinvested by the investor anyway, which is the spillage half of the problem: the investor may not want the water that quarter, so they pour the after-tax remainder back into the same fund the faucet was draining. The IRS takes a piece on the way out. The trough overflows on arrival. The investor refills the trough from what is left and waits for the faucet to do it again next quarter.

For a given total return, the position that delivers most of it through price appreciation rather than income is a well. The distinction is about how the return is delivered, not necessarily about asset classes. The investor owns the appreciating asset and draws from it only when they actually need cash. The water that stays in the well does not evaporate because it never leaves the well. It compounds in cool storage, untouched by the sun. When the investor eventually draws a glass, only that glass passes through the open air, and the evaporation rate at that point is lower because long-term capital gains are taxed at a lower rate than ordinary income. Nothing spills, because nothing was drawn that wasn’t needed.

The investor who needs $40,000 a year from a million-dollar portfolio does not necessarily need a portfolio that yields 4%. They need a portfolio that produces a 4% total return.

We believe that a new generation of ETFs has been built explicitly to be the wells. Some deliver short-term Treasury-like returns through capital appreciation rather than monthly coupons. Others use options in hedged equity solutions to replace bonds for a portfolio with similar risk, but with returns driven by price appreciation rather than income. This fits right into the Aptus mantra of ‘More Stocks. Less bonds. Same risk.’ It also hopefully results in a better after-tax outcome for investors.

For a taxable investor, the structural question is not “what yield does this generate?” It is “when does this water leave the well, and how much do I lose on the way out?” A position that compounds quietly inside its wrapper, and only releases water when the investor decides to draw it, is doing more work than the headline yield suggests. A position that distributes water every month, however much the investor likes the look of it, is paying the sun and the dirt before the investor ever takes a sip.

The faucet is the convention. The well is the improved structure. Across a thirty-year retirement, the spread is the difference between paying for the water you wanted and paying for the water you didn’t. For a taxable investor, that compounds into a portfolio that is meaningfully larger at the finish line, or a retirement that doesn’t have to be downsized to make the math work.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2605-20.