Common practice is to insure your house, your car, your life, your health, and even your dog. Then you reach what may be the largest financial asset many families own, the investment portfolio, and skip the insurance step entirely. To see why that might be a mistake, it helps to start with a fire.

At 5:12 on the morning of April 18, 1906, a magnitude 7.9 earthquake hit San Francisco. The shaking did real damage, but the fires that followed did far more. Gas lines ruptured, the water mains had broken, and the city burned for three days. By the time it was over, 80% of San Francisco was gone.

Here is the part most people don’t know. The standard policy of the day covered fire but excluded earthquakes. Nearly 90% of properties carried fire insurance. Almost none carried earthquake coverage, because the product barely existed. So when the city burned, the same question landed on every insurer’s desk at once. Were these fires covered, or were they caused by an excluded earthquake and therefore excluded, too?

The industry split along ethical lines. Some companies hid behind the exclusion. Several went bankrupt trying to pay. And a senior underwriter at Lloyd’s of London named Cuthbert Heath sent his San Francisco agent a telegram that became famous in the trade: pay every policyholder in full, regardless of the terms of their policies. Heath knew the fine print probably let him deny the claims. He paid anyway.

The firms that paid in full generally became the firms people wanted to insure with for the next century. The ones that hid behind the exclusion are mostly forgotten. The lesson the industry took from 1906 was simple. The protection you pay for is only real if you can count on it when the disaster actually comes.

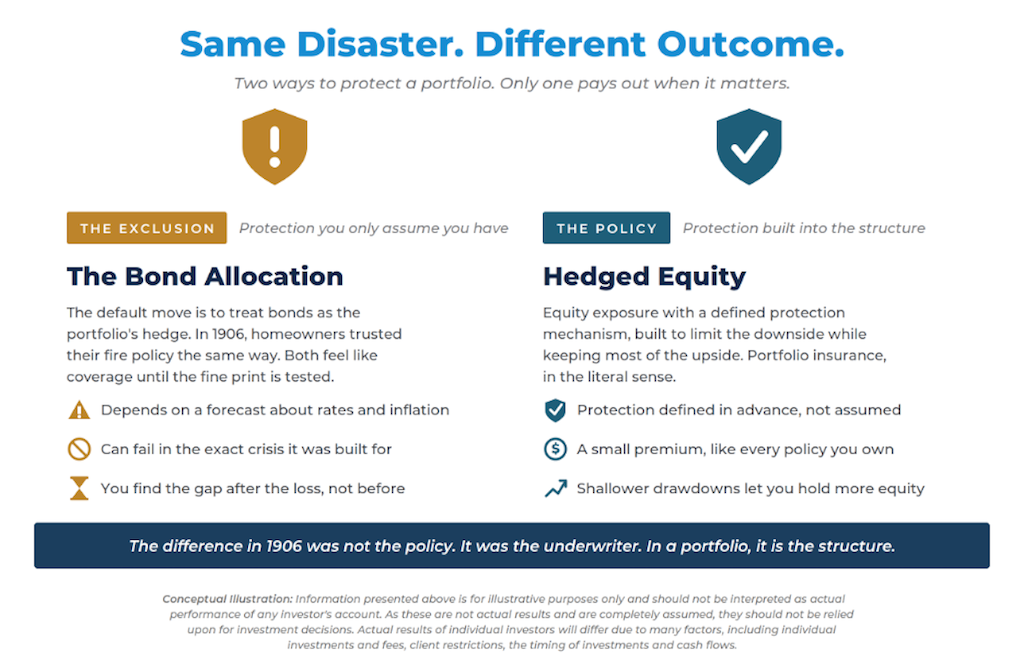

You Insure Everything But This?

Now look at how a typical investor handles risk. They cover every major asset they own, then assume the portfolio is already insured by its bond allocation. We think that’s the same assumption the 1906 homeowners made about the thing that actually burned the city down. The coverage felt real, right up until the fine print mattered.

A static bond allocation depends on a forecast: that rates fall, that inflation stays tame, that the hedge moves the right way at the right time. When those assumptions break, the protection may not be there. That is an earthquake exclusion in different clothing.

A hedged equity strategy is not the insurance, but it’s the insured home. The equity is the house, and the hedge, usually built with options, is the policy layered on top. The strategy still loses value in a serious drawdown, the same way an insured home still suffers from a fire. The goal is for it to lose meaningfully less because the hedge is designed to pay off precisely when the equity is falling.

Like home insurance, the hedge costs something, and in most years it appears to do nothing visible. The premium is small relative to the asset. It earns its keep in the rare moments when it pays out. It also does something quieter in the meantime. A drawdown that is structurally shallower lets the investor hold more equity than they otherwise could, because the catastrophic case is handled. Better defense allows more offense. The fire coverage is part of why you can carry the mortgage at all.

The 1906 story has one last thing to say. The difference between the homeowners who came out whole and the ones who were wiped out was not always the policy. It was the underwriter. In a portfolio, the equivalent is the structure. Protection written into a low-cost, transparent, daily liquid wrapper is protection we think you can build upon; a bit sturdier than hoping for a relationship that may disappear when needed most.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2606-15.