Some investors still view dividends and coupons as more “real” than selling shares for cash. That made sense decades ago, when trading costs were high.

Today, transaction costs are negligible. When the underlying economics are the same, there is little difference between receiving income and selling shares to meet cash needs. The real difference lies in taxes, where deferred structures can hold a clear advantage.

When it comes to investing, the difference between paying taxes today and deferring them for tomorrow can be enormous. The math is simple, but the impact compounds.

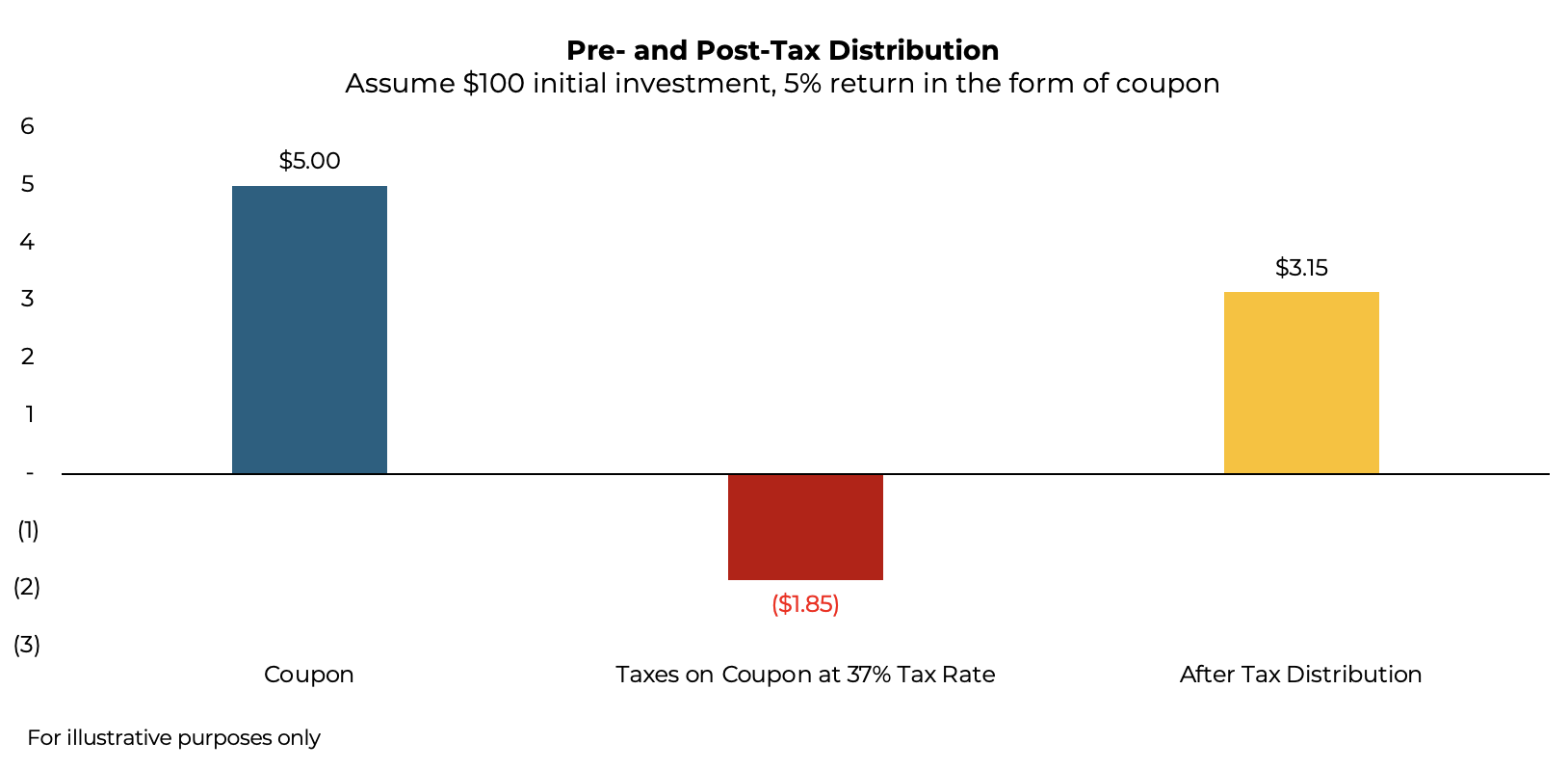

Scenario 1: Taxable Bond Yielding 5%

Take a bond paying a 5% coupon. For every $100 invested, the owner receives $5 of taxable income. Since bond interest is taxed at the short-term rate (assume 37%), $1.85 ($5 x 37%) of that $5 coupon goes straight to the IRS. An investor is left with $3.15 of after-tax income to reinvest or spend.

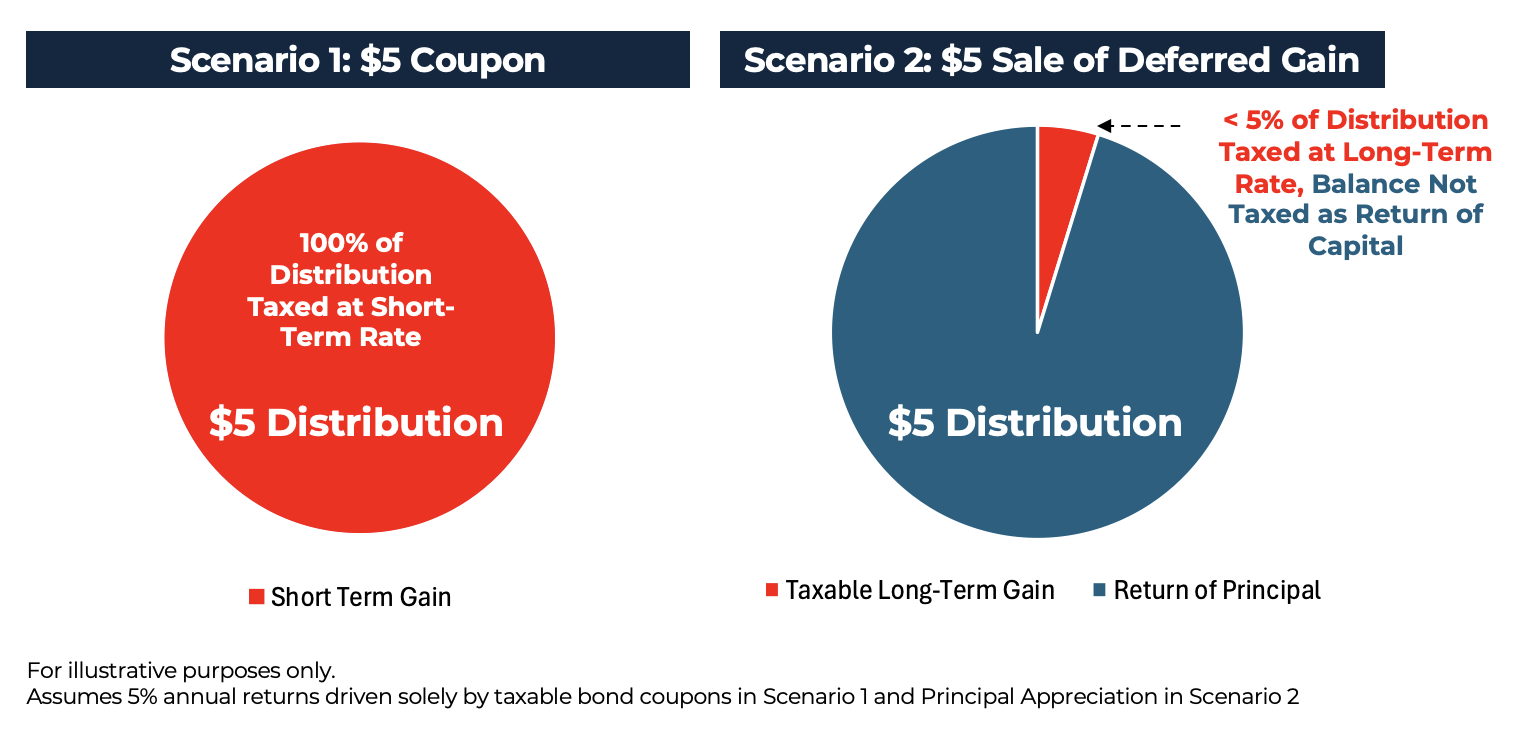

Scenario 2: 5% Deferred Return

Now compare that with a strategy that produces the same 5% return, but instead of distributing income, it simply grows from $100 to $105. If the investor wants the same $5 of pre-tax cash, they sell $5 worth of the $105 position.

Here’s a key benefit: when selling, cost basis is spread across the entire holding. So the $5 sale is mostly principal, with only a fraction recognized as a taxable gain. Specifically, $5 is 1/21st of the position ($5 of $105 value), so only that small 1/21st slice is treated as a gain.

At a 20% long-term capital gains rate, the tax owed is just five cents ($5 x 1/21 x 20% = $0.05). That leaves the investor with $4.95 after tax, compared to $3.15 in Scenario 1, for the same return and the same $5 withdrawal.

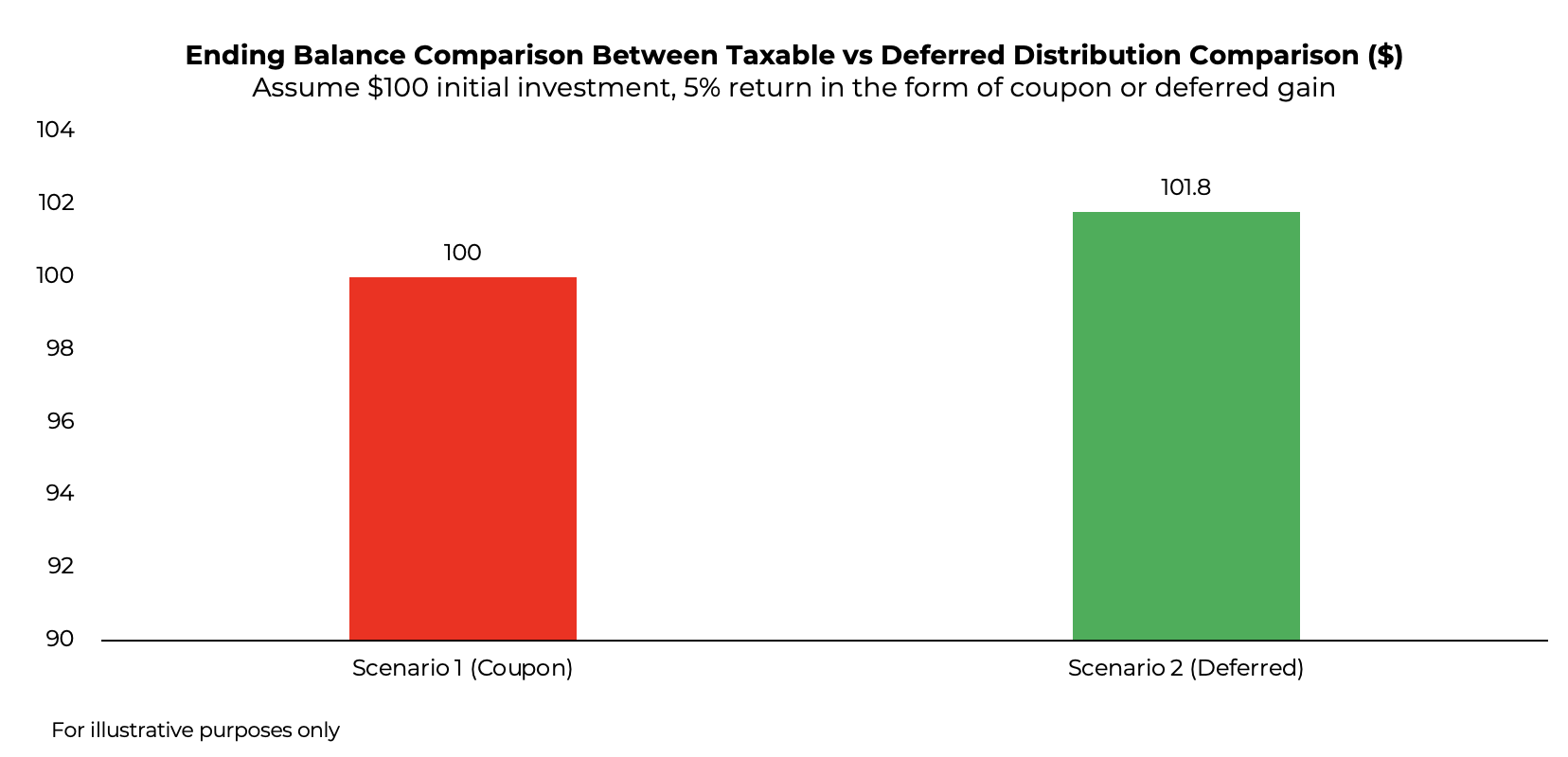

Scenario 3: Equalizing After-Tax Distributions

Suppose the investor only wants $3.15 of after-tax cash (to match Scenario 1). With the deferred structure, they only need to sell $3.18.

In each case, the investor earns the same return and receives the same after-tax distribution. But the deferred structure keeps an additional $1.82 in the account.

In year one, that extra $1.82 is material, but left to compound over decades, it becomes much more meaningful.

Coupons are a Relic of the Past

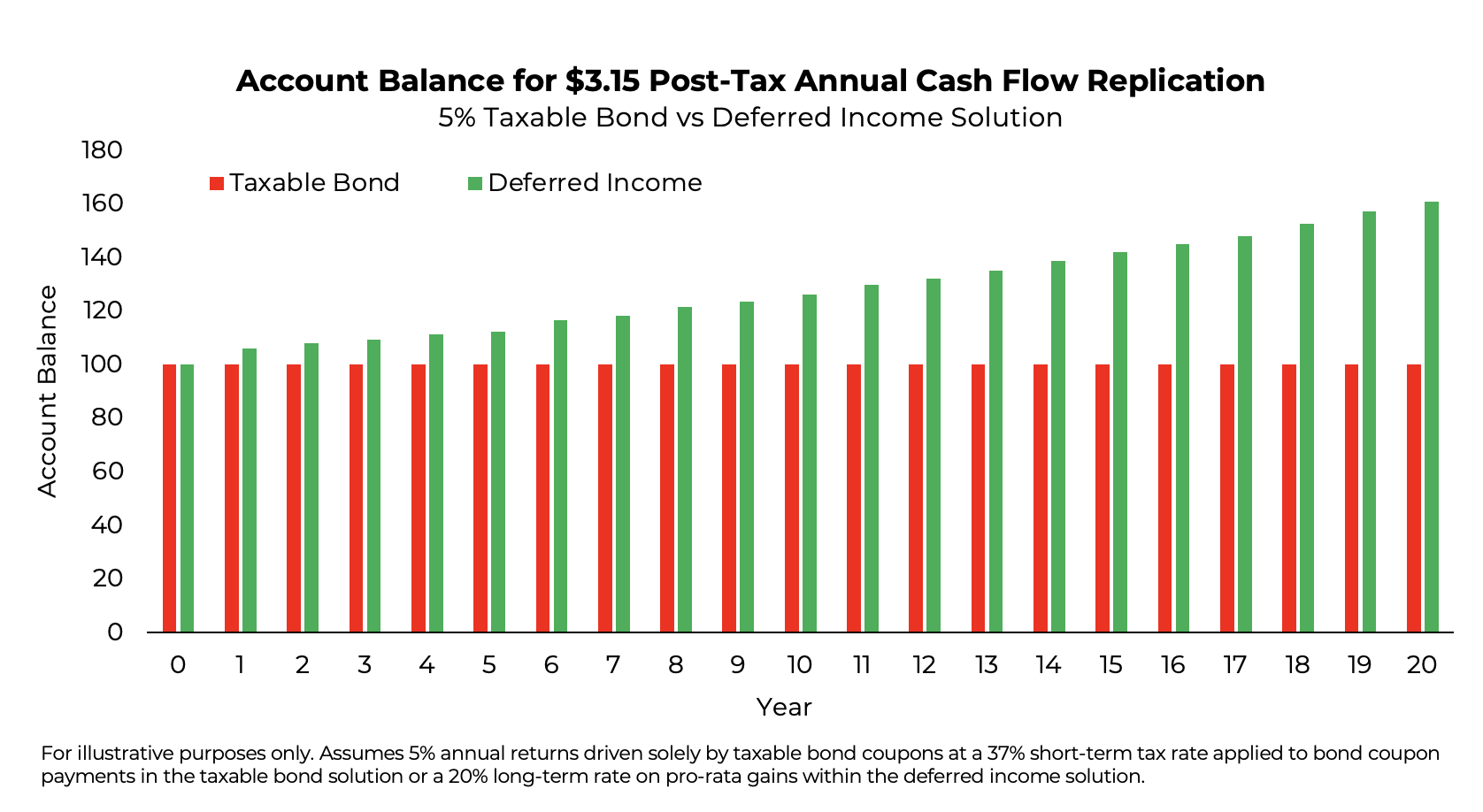

The lesson is simple: the method of receiving cash matters far less than the amount actually kept. With today’s tax code favoring long-term capital gains, instincts should always be checked against the actual math of who’s getting what share of the payment.

By deferring income and letting your capital keep working, you turn what would have been an immediate tax bill into future growth that will be taxed a lower rate. Over time, that compounding difference can reshape long-term wealth outcomes.

We’re all over tax savings, let us know if we can help think through any client cases.

Disclosures

Past performance is not indicative of future results. This material is not financial or tax advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed and all calculations may change due to changes in facts and circumstances.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2509-17.