Back in February, we wrote about a common tax mistake investors make with their fixed income allocations: ignoring the state tax benefits of Treasuries. A simple breakout of Treasury income (which is not taxable at the state) can save clients thousands (or more). As we head towards year-end, we want to expand on that concept.

There is a massive inefficiency sitting in many taxable accounts right now due to a razor-thin gap in the Aggregate Bond Index (the Agg).

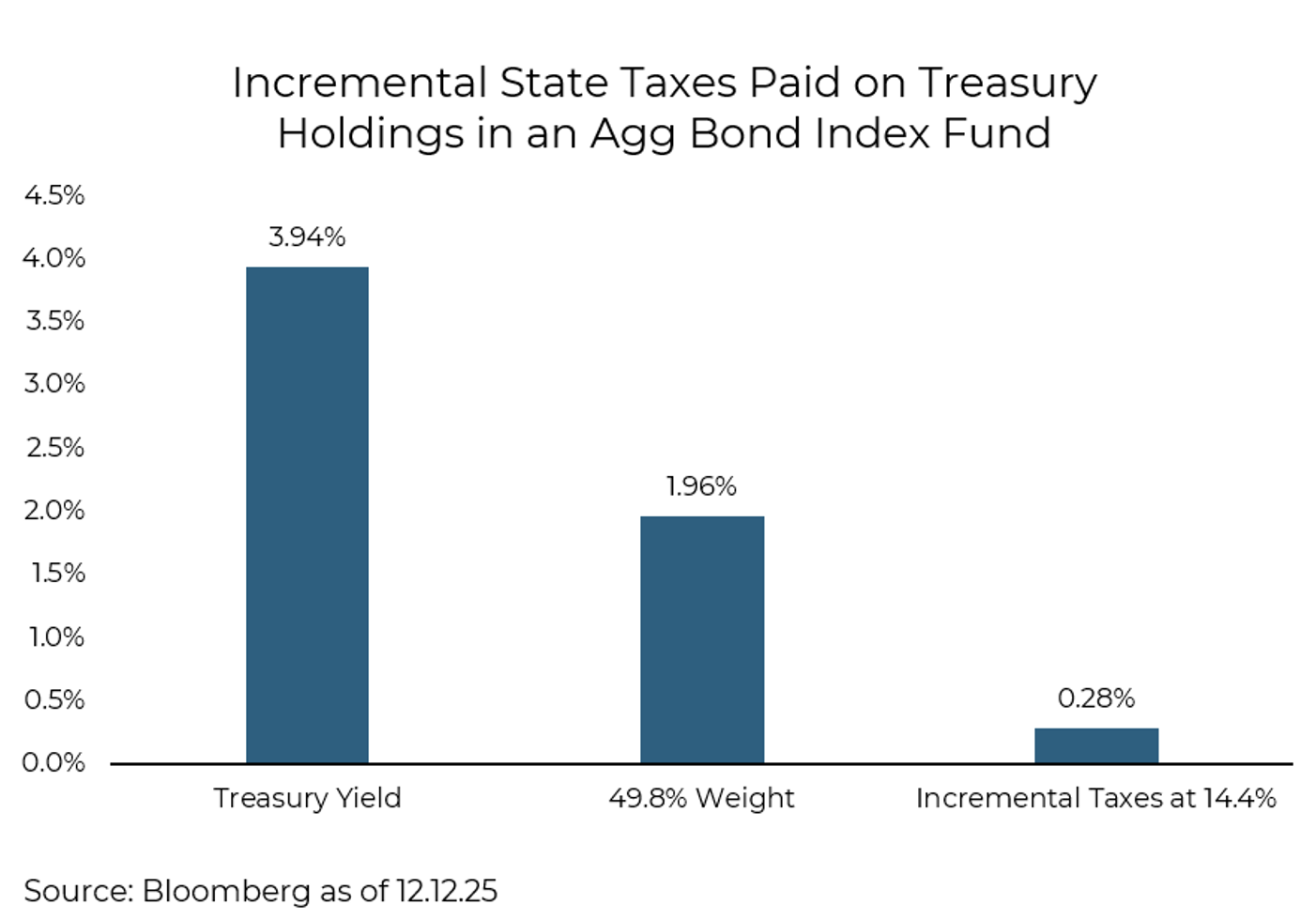

In high-tax states like California and New York, a fund must maintain at least 50% of its assets in U.S. government obligations at each quarter-end to pass the state tax exemption through to shareholders. While the Bloomberg Aggregate Bond Index (Agg) is the standard benchmark for core fixed income portfolios (and actual tax-exempt eligibility is dependent upon the specific ETF used), its current composition may fall short of this threshold. The Agg is currently comprised of approximately 45.5% US Treasuries and 4.3% government-related bonds, bringing the total U.S. Government exposure to 49.8%, below the 50% threshold.

That 0.2% difference is the hurdle that may be costing your clients thousands of dollars in after-tax returns. Because the Agg sits at roughly 49.8%, your fund may fail that 50% test. This means you are paying state taxes on income that should be state tax-exempt. You are effectively making a voluntary donation to the state revenue department.

At a 14.4% tax rate (the highest effective state tax rate in California), an investor is paying an incremental 28.25 bps ($2825 in state taxes per $1,000,000 invested), owning a Bloomberg Agg index fund compared to owning the Treasury allocation alone (current yield of 3.94% for Treasuries x 49.8% weight x 14.4% tax rate).

The Case for “Unbundling”

Let’s look at a simple structural fix. Instead of holding the Agg, imagine you simply “unbundled” it. You take ~50% of your investment and buy a dedicated Treasury fund (or individual Treasuries), and you put the remaining 50% into a credit-oriented fixed income strategy, whether an outright credit fixed income fund or a fixed income alternative that may outperform. The allocation and risk profile can be structured to be nearly identical, but by holding the Treasuries separately, they become 100% eligible for the state tax exemption.

However… Why Own the “Other” 50%?

While unbundling solves the tax problem, it doesn’t solve the market problem. If you separate the portfolio, you are left holding a standalone bucket of higher-risk fixed income in an environment where spreads are near all-time narrow levels as outlined in our recent post, Reconsidering Core Bonds: Why Treasuries May Be the Smarter Choice Today. We have to ask if the juice is worth the squeeze?

This brings us to our broader view: Don’t just unbundle the Agg. Rethink the credit portion entirely.

The Better Alternative

If the goal is tax efficiency and meaningful return, simply buying a plain vanilla corporate bond fund may be suboptimal. We believe there is a better way. By utilizing new bond alternatives, previously highlighted in our piece on how ETFs Changed the Game for Equities, Now It’s Time for Fixed Income, you can achieve two goals that the Agg cannot.

First, an investor may be able to avoid a sole focus on what we view as an unattractive risk/reward profile of spread-oriented fixed income. Instead, alternatives that may maintain credit exposure as a component while utilizing a broader set of tools designed to generate both potential return and built-in protection may be the better allocation.

Second, new strategies wrapped in an ETF structure can be more tax-efficient than simply buying traditional bonds. By aiming to defer income over time rather than forcing taxable distributions today, these strategies can further reduce the tax drag on a portfolio.

Give us a call. Let’s discuss how swapping out that legacy Agg position can instantly lower your client’s tax bill, remove credit risk from their allocations, and unlock the diverse opportunities provided by modern ETF alternatives.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2512-19.