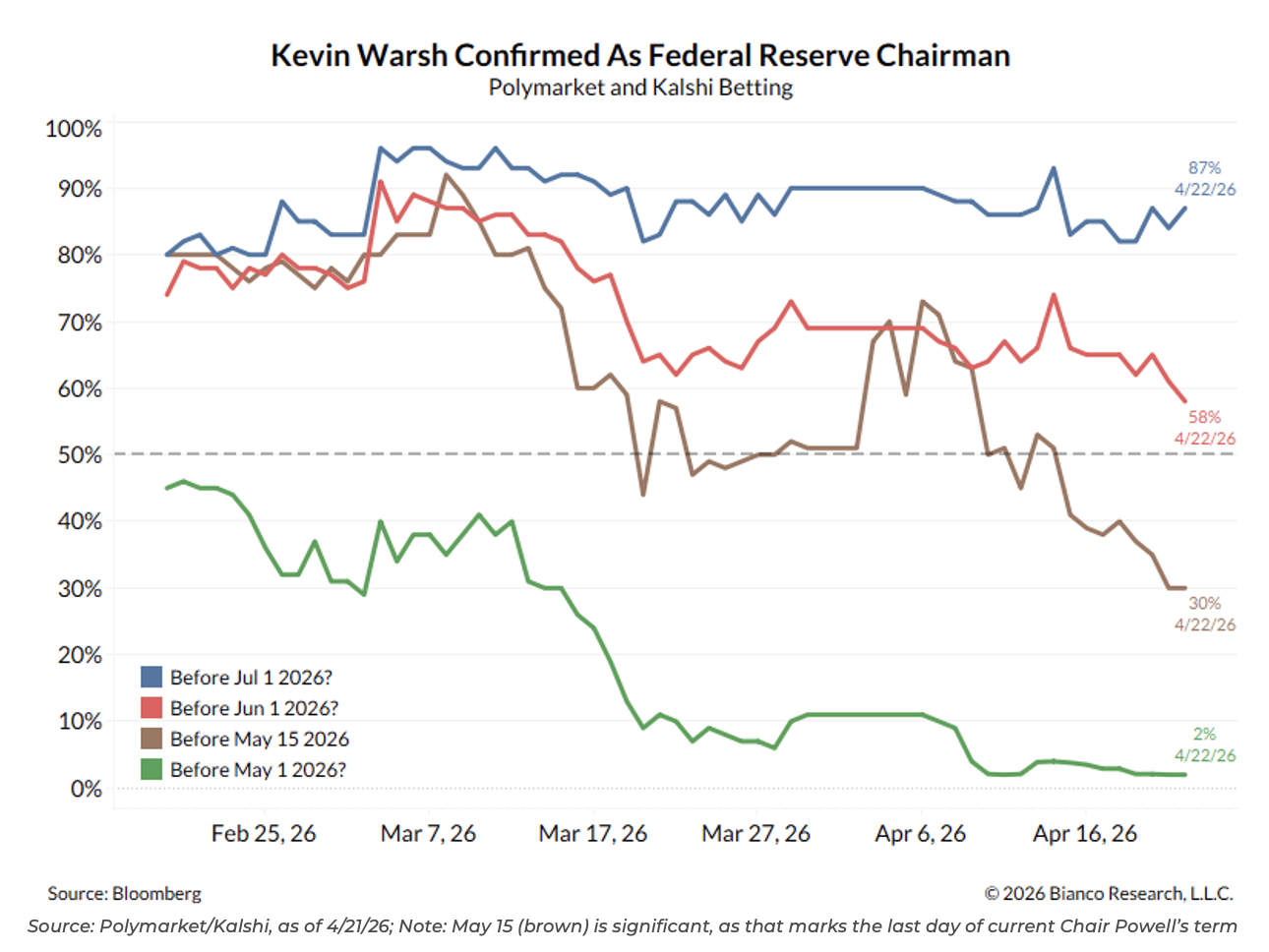

President Trump’s nominee, Kevin Warsh, appeared before the US Senate seeking ultimate approval to be named the 17th Chair of the Federal Reserve. While the US President may be the “Leader of the Free World,” one could make a strong argument that the US Federal Reserve, and therefore its leader, wields more power. As such, the approval process is highly politicized, with this installment being no different. Democrats have expressed their opposition, putting Warsh’s ultimate approval in jeopardy.

Admittedly, there is cause for partisan divide on the subject of Warsh as prospective Fed Chairman. President Trump hasn’t minced words in criticizing current Chairman Jerome “Too Late” Powell (Trump’s less-than-endearing nickname), expressing his discontent at what he views as an interest rate regime that is higher than it should be. It is natural to assume that if this is the President’s stance, he would surely nominate someone ready and willing to fall in line with such sentiment.

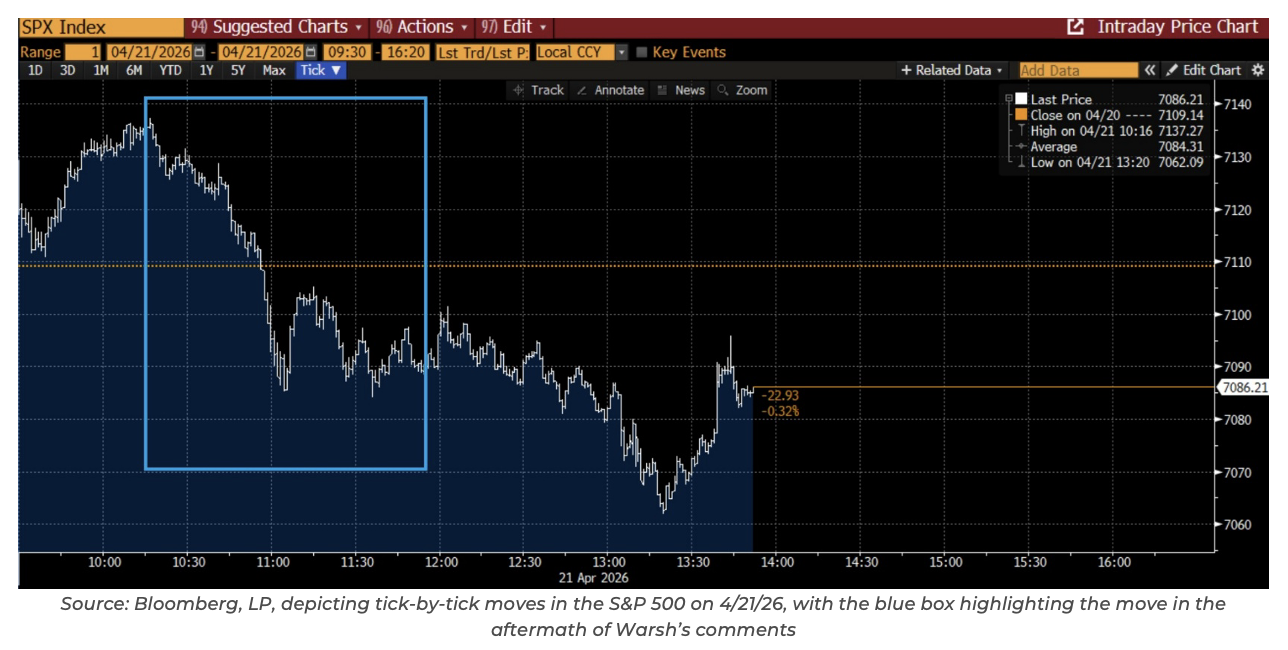

Warsh tried to dismiss that label, addressing the question as to whether he would be President Trump’s sock puppet with, “absolutely not…I’ll be an independent actor if confirmed.” In an interview earlier that day, President Trump admitted that he’d be disappointed if Warsh didn’t cut rates as soon as he took office.

Like President Trump, the stock market also favors interest rate cuts. All things equal, lower interest rates reduce borrowing costs and increase liquidity in the financial system, generally buoying risk assets. So the prospect of Warsh failing to live up to President Trump’s desire for rate cuts adds to the rate debate, with Fed Funds Futures adjusted to price only a ~50% chance of a 25 basis point rate cut over the next 12 months, down from roughly a sure thing the day before. Stocks used the comments as an excuse for a breather after the huge rally of late.

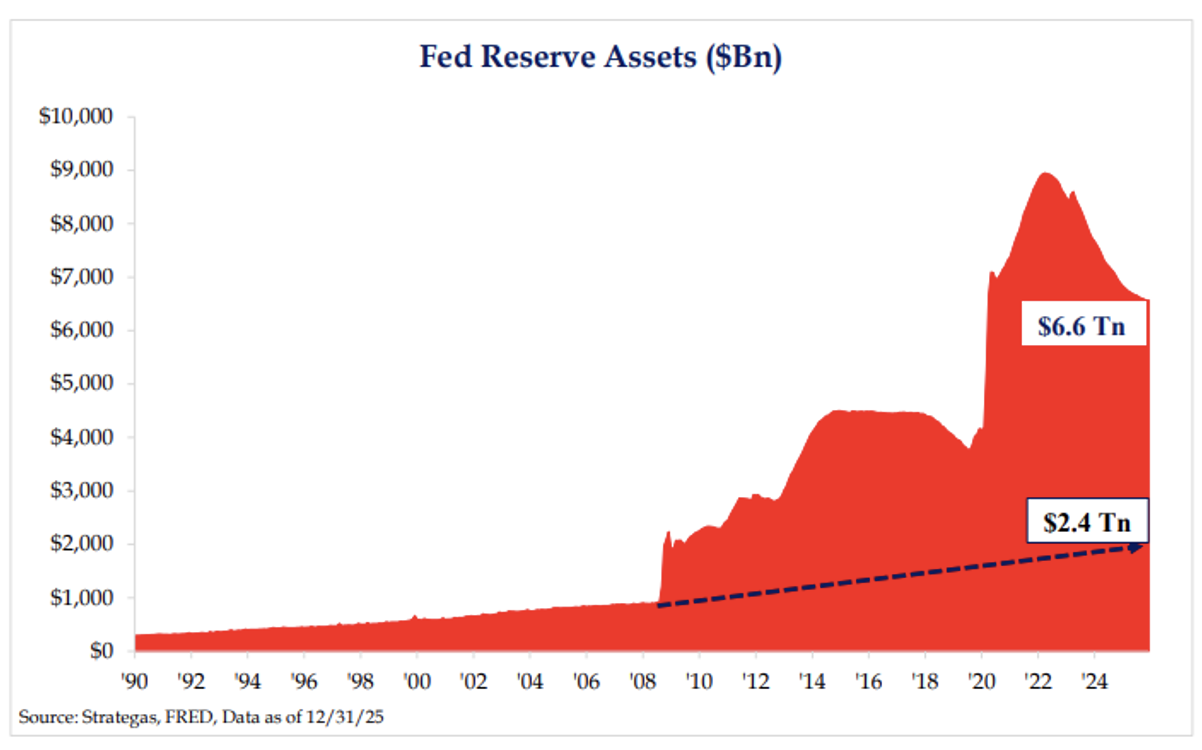

In any event, it is highly likely that Warsh will eventually be approved as Chairman. And while his independence and allegiance to President Trump’s wishes will be simultaneously tested, there may be a middle ground that allows him to satisfy both. Warsh has long been a critic of Quantitative Easing (QE), the practice of utilizing the Fed’s balance sheet to influence interest rates. It is important to remember that before the Global Financial Crisis (GFC), there was some debate as to whether QE was even legal, loosely interpreted as such under Section 13(3) of the Federal Reserve Act as appropriate in “unusual and exigent circumstances.”

While the GFC would undoubtedly qualify, what has followed seems a needless stretch, as QE has played a response to unemployment, social justice, climate change, and a health crisis. While Warsh expressed his opposition to QE as early as an op-ed written during his Fed governor tenure in 2010, the signs of its longer-term effects are just now visible.

1. It was regressive, leading to widening wealth inequality as savings weren’t rewarded while financial assets soared (the number of private equity firms doubled to ~10,000 in the 15 years that followed the GFC).

2. It rewarded financial engineering over capital spending, witnessed by innumerable companies choosing to issue cheap debt and buy back stock instead of investing.

3. It changed the concept of risk, as investors relied upon the Fed’s QE lifeline, pushing further out the curve. Investors searched for higher yields in dangerous places, as seen by the growing number of zombie companies (those with insufficient funds to pay off and or even service their debt).

So why does this matter? If Warsh is successful in reducing the Fed’s balance sheet, it will undoubtedly tighten financial conditions. Without an indiscriminate buyer in the market, bonds lose an important bid that has served to artificially depress yields for so long.

At a time when the macro landscape seems fairly balanced (considering inflation, employment, growth, etc), tighter financial conditions could push the economy into a recession. No Fed Chairman wants to unnecessarily manufacture a recession; the convenient counterbalance would be lowering interest rates. As a result, we could see largely unchanged monetary policy in aggregate, while both sides of the independence/rate cut debate claim victory. Nothing ever goes that smoothly, but it makes sense to have a game plan.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2604-22.