Newton’s First Law of Motion states that an object in motion tends to stay in motion unless an external force acts upon it. The Fed is in motion (hiking rates/QT) and until the external force (lower inflation) acts upon it, expect them to stay in motion (higher rates/QT). There is no pivot until there is lower inflation/ weaker jobs market.

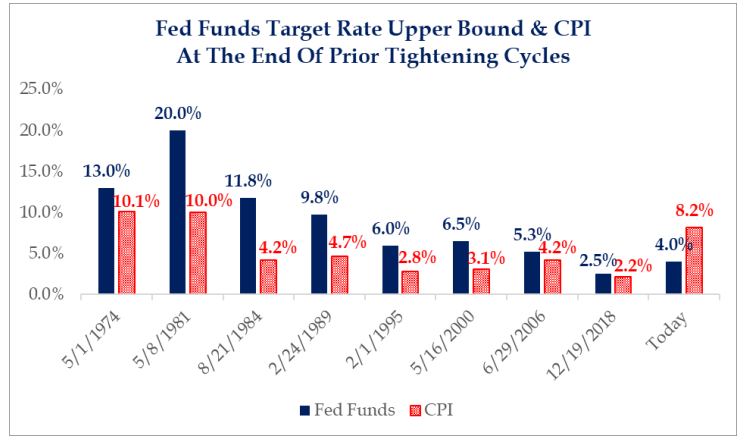

The question is at what point does policy act as a force against inflation? Is a terminal rate at ~5% enough? Historically, the minimum condition for restrictive policy is a positive real rate (interest rates > inflation). Using headline, rightly or wrongly, there still is a way to go. As the chart below shows…in the end, the terminal Fed Funds rate has always been higher than the CPI at the end of prior tightening cycles. Will this time be different?

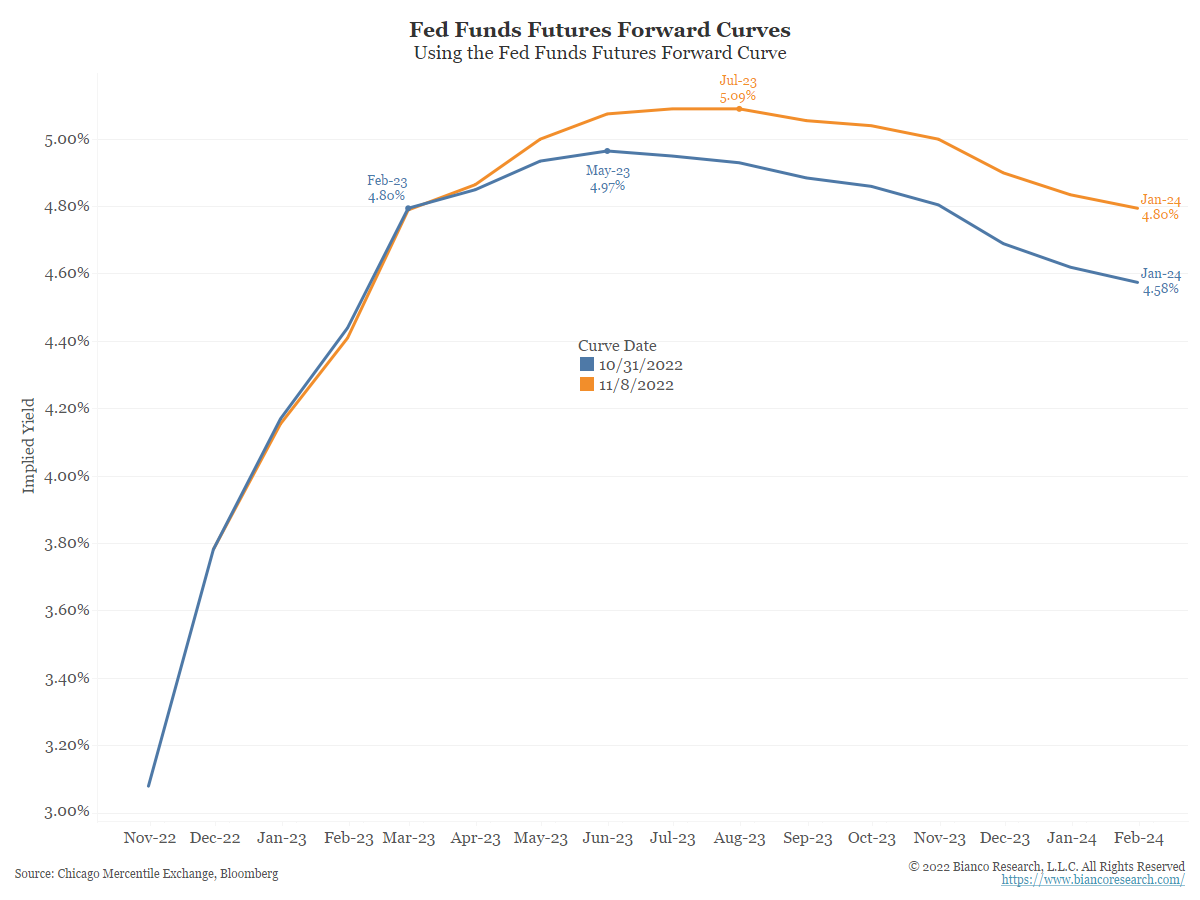

Source: Bianco as of 11.08.22

Source: Bianco as of 11.08.22

Simply put, the action the Fed is taking, by aggressively raising rates at a pace not seen in decades, is leading to upheaval in financial markets. The market narrative is that the Fed is making a mistake and will “pause,” “pivot”, or “step down” from this policy. The thinking is that the Fed’s policy function will cause a needless recession or unwarranted financial instability. Implied in this thought is that inflation is not persistent, and the aggressive Fed action is not needed.

Source: Strategas as of 11.02.22

Source: Strategas as of 11.02.22

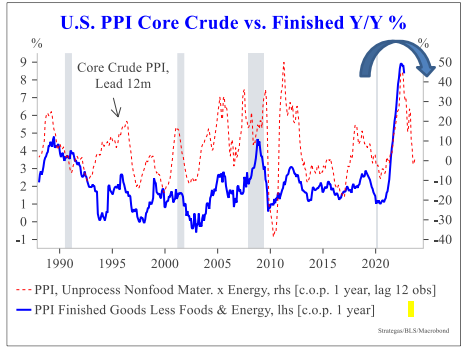

Will PPI lead CPI lower?

Source: Strategas as of 11.08.22

Source: Strategas as of 11.08.22

There are several positives on the inflation front that should begin to bring inflation lower, although we believe this process will take time.

- Longer-term inflation expectations still look anchored

- The U.S. PPI inflation pipeline is easing

- U.S. small businesses reported less price pressure (NFIB)

- U.S. import prices are declining

- M2 growth has slowed

- Home prices are declining/ Investment portfolios are lower (wealth effect)

- Supply chains are easing a bit (eg, NY Fed measure)

- Some retailers look to have over-stocked inventory

- The winter plan looks to include demand destruction in Europe

- The China PPI has hooked down

- Global growth remains under pressure (eg, OECD LEIs)

Two big things are working against inflation coming down quickly, even considering Fed tightening. First is a high likelihood of higher prices within the energy sector now that the SPR depletion is over. Second is that shelter inflation still has a ways to go to catch up to higher home prices (being 30% of core CPI, that is a big effect).

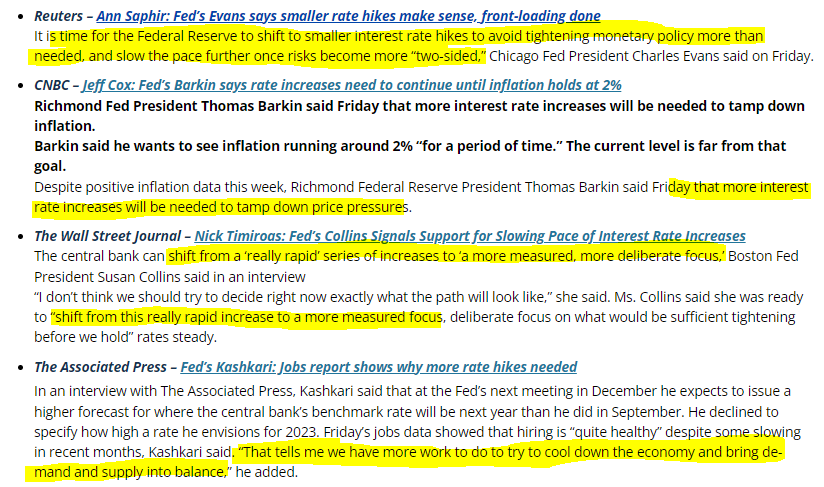

Is the Fed in Agreement on Policy? Nope!

Source: Bianco as of 11.09.22

Source: Bianco as of 11.09.22

We’ve seen a continuation of the disappointing trend from Fed officials. The officials focus on the short-term (next meeting) and the size of the rate hikes. They might extend a little longer and comment on where the terminal rate is, but unfortunately, they rarely go further. Jay Powell does the same.

It could be argued these speeches are the clearest form of forward guidance ever given, despite the Fed officially ending forward guidance several meetings ago.

Left unanswered is why the Fed is hiking 75 basis points at every meeting. Why are they raising the Fed Funds rate hundreds of basis points this year? What would happen if they were not this aggressive? Has the long-term trend of inflation changed?

The closest the Fed will come to answering this long-term question is to say that “inflation expectations have remained well-anchored.”

The reason, we believe, for the lack of explanation on these issues is there is no agreed-upon long-term inflation outlook at the Fed. Obviously the Fed missed the boat by calling inflation transitory and persistently overlooking the implications of the monetary + fiscal policy they were leading.

Most of the officials are from academia and have never/ rarely held private sector jobs (Powell the exception). They’ve also never experienced an inflationary environment like today. There is much uncertainty behind the question of why inflation is different this time… but we aren’t getting many answers as to why they believe things are the way they are.

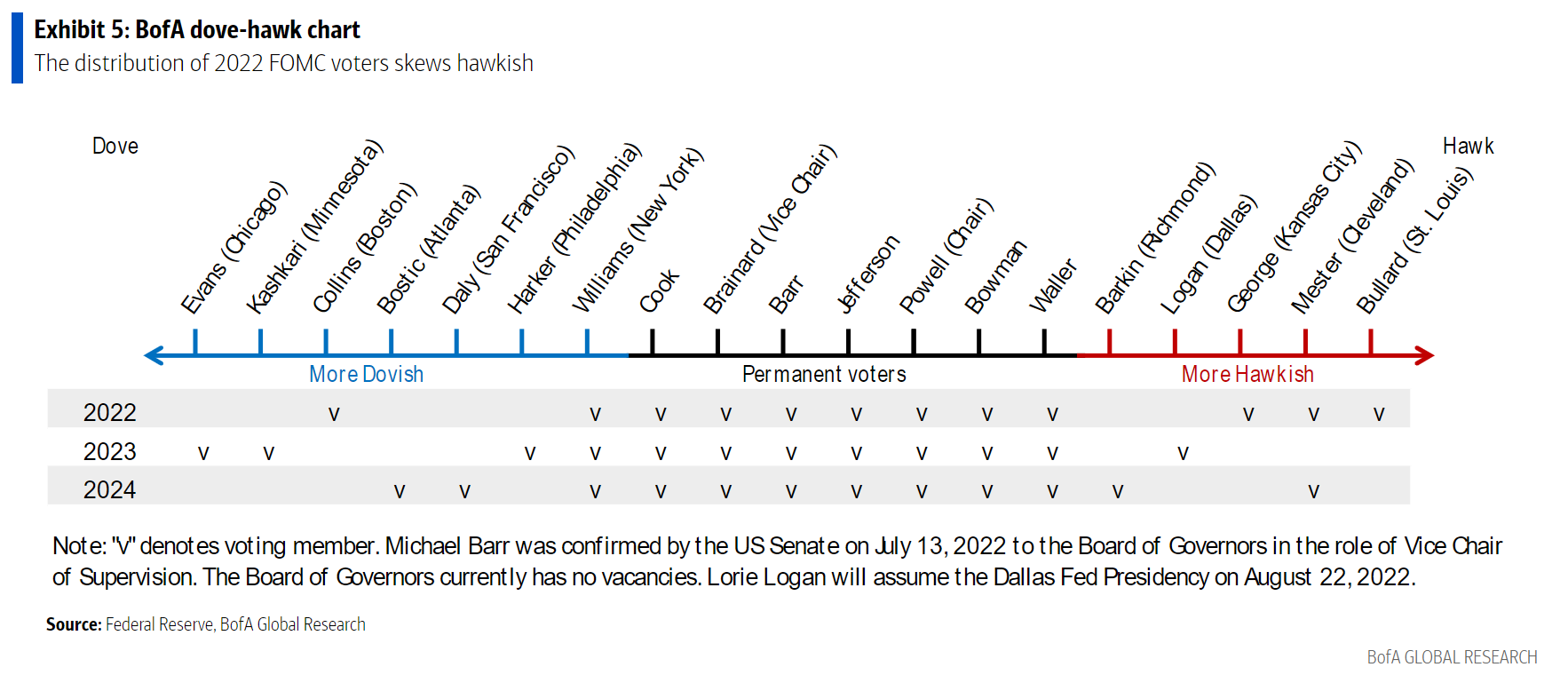

What Does the Fed Look like in 2023?

The Federal Open Market Committee is composed of 12 members. Seven members of the Board of Governors + the New York Fed President + 4 rotating District Presidents.

- Chairman serves a renewable 4- year Term

- Board of Governors are appointed by the President (confirmed by the Senate). They have a permanent voting seat

- NY Fed President is a Permanent Voter

- (4) Voting District Regional Presidents (Yearly Rotation – shown below)

Source: BAML as of 11.08.22

Source: BAML as of 11.08.22

Voting rights changes at the Fed are somewhat confusing to most outsiders. We do know that certain members have more clout. We thought we’d help clarify. The Chairman + Board of Governors + NY Fed President are known voters. The 4 Regional Presidents are revolving. These four votes shift notably more dovish in 2023, as Bullard, George, Collins and Mester are being replaced by Evans (Chicago), Harker (Philly), Logan (Dallas) and Kashkari (Minneapolis).

Bullard, George, and Mester are all hawkish speakers / voters. Collins leans dovish. Evans and Kashkari have historically been very dovish. We would note that as a nonvoter (this year) Kashkari has been uncharacteristically hawkish (will that continue as a voter?). Logan is the new Dallas Fed president and is typically moderately hawkish, and Harker leans dovish.

With the swap from hawkish voters to dovish voters, could the pivot be nearer than expected? We are already getting a taste of the “pause” or “slow down” message from the dovish leaning members (noted above). My question is…will the Fed be able to anchor inflation expectations before this shift occurs?

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

When a page is marked “Advisor Use Only” or “For Institutional Use”, the content is only intended for financial advisors, consultants, or existing and prospective institutional investors of Aptus. These materials have not been written or approved for a retail audience or use in mind and should not be distributed to retail investors. Any distribution to retail investors by a registered investment adviser may violate the new Marketing Rule under the Investment Advisers Act. If you choose to utilize or cite material we recommend the citation, be presented in context, with similar footnotes in the material and appropriate sourcing to Aptus and/or any other author or source references. This is notwithstanding any considerations or customizations with regards to your operations, based on your own compliance process, and compliance review with the marketing rule effective November 4, 2022.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2211-8.