The Fed’s annual Jackson Hole Economic Policy Symposium takes place on Friday and will open with a speech by Chair Powell at 10am EST. We expect Powell to reiterate that the FOMC remains committed to bringing inflation down and that upcoming policy decisions will depend on incoming data. He will likely pair this with verbiage on slowing the pace of tightening, which he laid out in his July press conference and the July minutes released last week. In addition, we hope to get a few more comments on the pace of Quantitative Tightening (QT) and its expected implications to financial conditions. While the market might view the likely slowdown in hikes as a pivot, we aren’t so sure that is the case.

Looking Back to the 2021 Speech: What Went Right for Powell … Well, Not Much

In his 2021 address, we think Powell got it wrong in several important ways. He asserted that the surge in inflation was “likely to prove temporary”, that the low unemployment rate “understates the amount of labor market slack”, and that “we see little evidence of wage increases that might threaten excessive inflation”. He also endorsed the more inflation-tolerant monetary policy framework that the Fed adopted in 2020 as “well-suited to address today’s challenges”. We’d guess he’ll hope to be more prophetic than last year.

The Market is Still Trying to Buy “Peak Inflation” and Another Fed Pivot

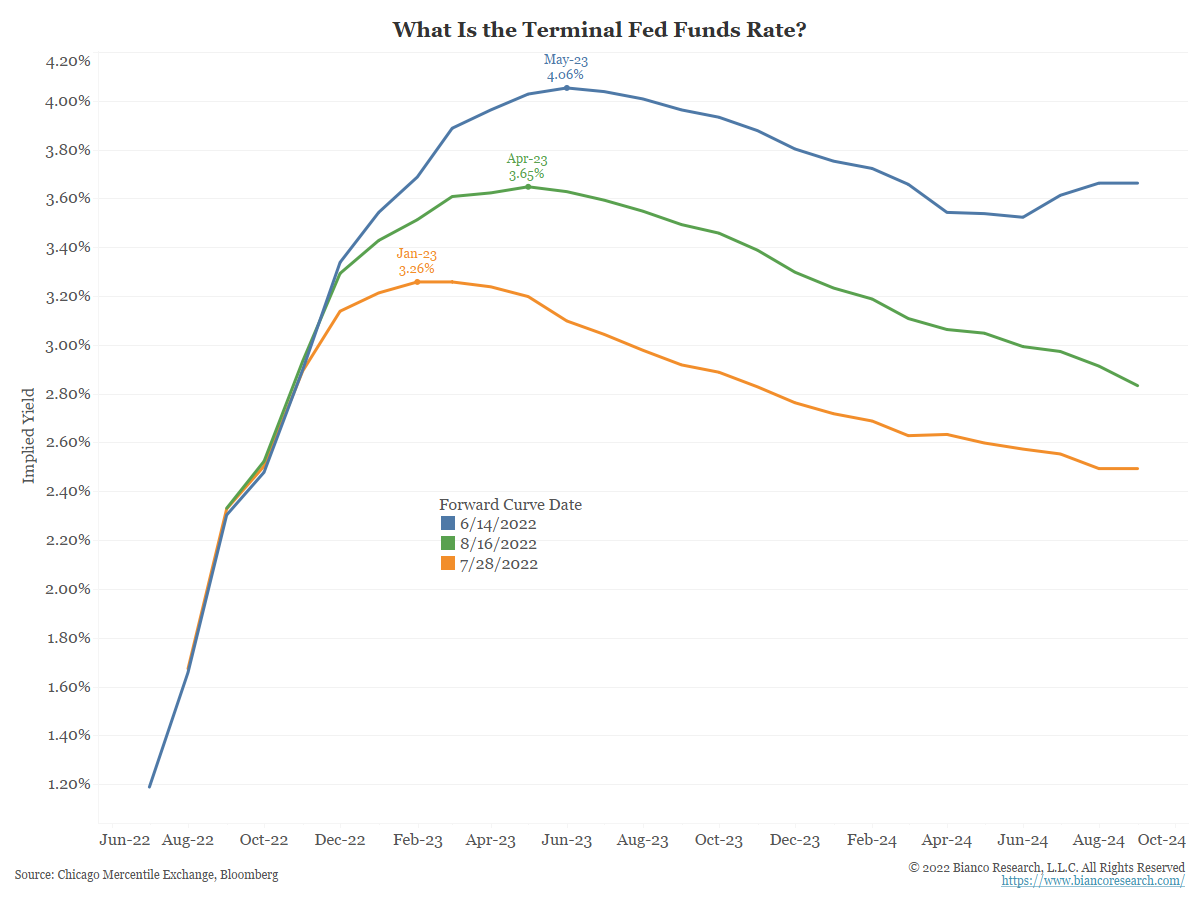

The “peak inflation” story has provided relief for risk assets since early July. Coming into Jackson Hole, if the Fed wants to change the narrative of a pivot to easier policy, the communication Friday and over the next month will be critical. The slowdown in month over month inflation (“peak inflation”) means the pace of rate hikes does not need to continue at the +75bp clip of the past two FOMC meetings, especially considering QT is ramping up (look for a blog next week on this topic). In saying that, we believe monetary policy still needs to continue tightening to bring down inflation…markets are pricing in cuts but our opinion is that we see the Fed Funds rate approach 4% by early 2023).

Data as of 8.16.22

Data as of 8.16.22

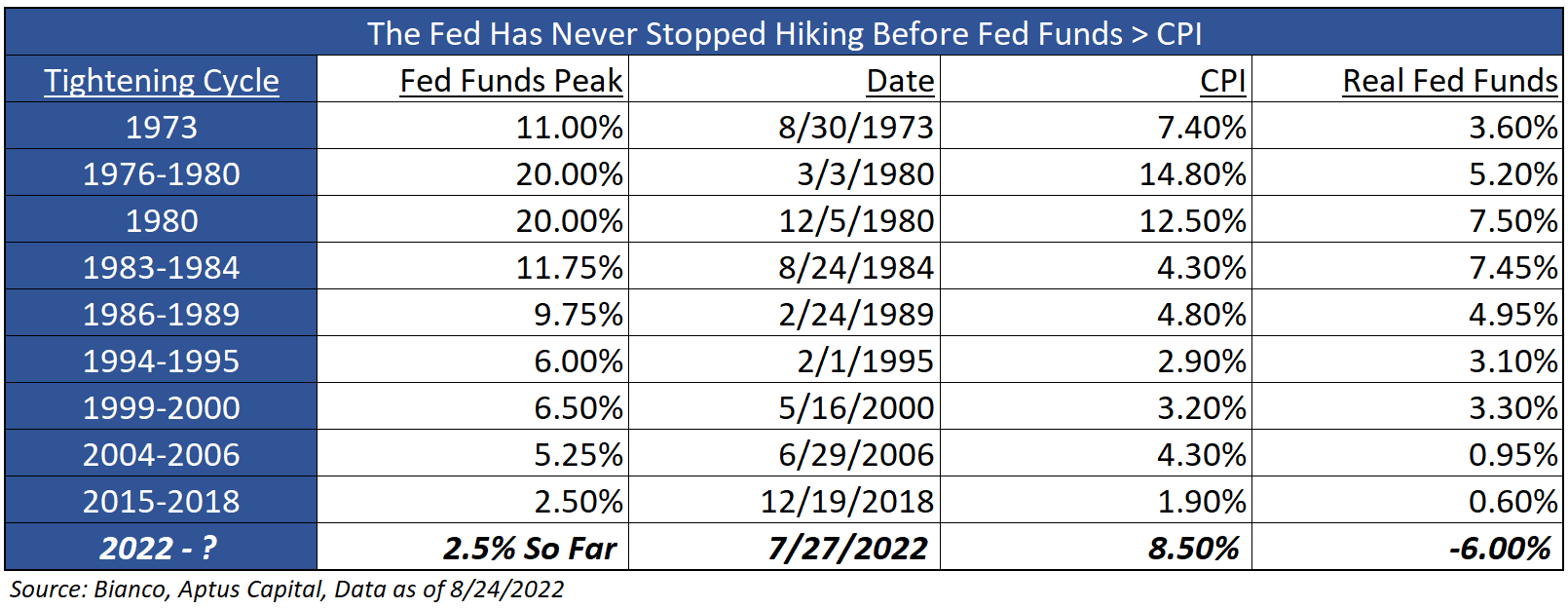

Regarding monetary policy, we think the Fed will likely avoid pursuing a stop-and-go strategy – this was a mistake in the 1970s that did not work out well (i.e., it led to stagflation). The FOMC knows this. A policy “pivot” could be slower rate hikes in September through December. However, when it comes to rate cuts, the bar is quite high given the macro backdrop. An important question now is where will core inflation settle out. The inflation problem hasn’t receded, as we still have the situation of demand in excess of supply. This has generated inflation and is threatening to become entrenched.

Bill Dudley’s Comments

We are always interested in former Fed officials’ commentary as they are often the best people to listen to if you want an honest assessment of the economy or markets. They are uninhibited by their post and can speak honestly.

Former New York Fed President Dudley does not disappoint with his comments. In a recent op-ed, he noted how off base Powell’s assessment was at last year’s Jackson Hole meeting. But on Friday, traders will undoubtedly obsess over The Chair’s every word; keep in mind he was touting how temporary inflation would be at last year’s speech.

The gist of Mr. Dudley’s commentary was that he expects Powell to emphasize three themes during Friday’s speech:

- The economy still has forward momentum with an extremely tight labor market and unacceptably high inflation.

- The Fed must tighten monetary policy further to restrain the economy and ease pressure on the labor market.

- The Fed won’t relent until it’s sure it has done enough, for long enough, to achieve its 2% inflation target.

We agree with Mr. Dudley. And unless Chair Powell is willing to risk being remembered as the new Arthur Burns, the Fed is not done yet!

Bottom Line

We must go back to the Fed’s first principles: restoring price stability is key. This has not been accomplished yet, so the FOMC is still looking to slow down demand. It remains tough to believe policy is overly tight given real interest rates are still historically low/negative. Some softening in the U.S. labor market (unfortunately) looks necessary, though this slowdown has not registered yet in the nonfarm payrolls data.

The U.S. economy is trying to look like 2019, but without a 2019-balanced labor market (and MUCH higher inflation). Labor force participation remains lower & we are running into a demographic wall as time goes by. Even with “peak inflation,” pressure from sticky components remains firm, and central banks are focused on this risk… we think Powell will reiterate this on Friday.

There isn’t much doubt in our mind that the FOMC will have to slow down from the aggressive +75bp rate hikes. The U.S. economy is weakening (i.e., weak real GDP in 1H of 2022, terrible productivity, money supply shrinking). The U.S. 2yr/10yr yield curve remains inverted. Housing (interest rate sensitive) is weakening. The labor market is showing some signs of cracks (i.e., weekly jobless claims trending up).

But we don’t want to mistake a slowdown to +50bp or +25bp hikes for a full Fed pivot (i.e., rate cuts). Anchoring inflation expectations remains a process, which is not yet (near) complete. Peak inflation remains different from mission accomplished. There’s evidence demand is slowing but until supply catches up, restraint is what is necessary to bring inflation under control – tight policy must persist.

.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2208-23.