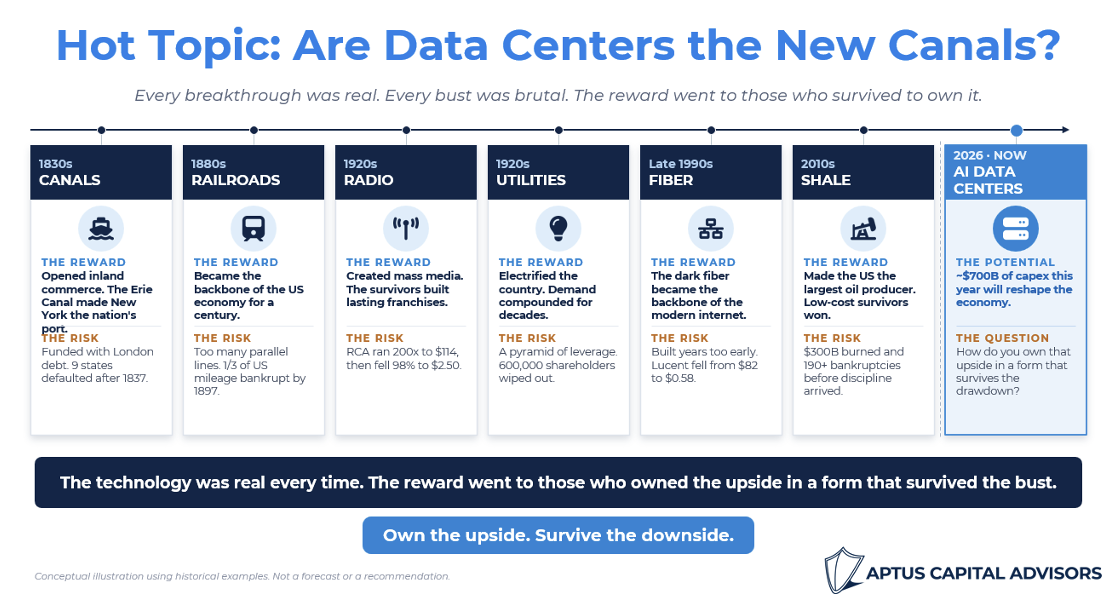

Three boom and bust stories from American capital history. None of them is a forecast for AI. Each is here for what it says about how a portfolio survives whichever outcome arrives.

In the 1830s, every state legislature in America agreed that canals were the future of commerce. The Erie Canal had made New York rich, and the obvious next move was a national water grid. States borrowed heavily in London and spent future federal land sale revenue before a dollar of it had been collected. By 1840, the country had more than 3,000 miles of mostly uneconomic canals, built at a cost of $125 million, nearly twice the federal debt that already existed.

Then the Panic of 1837 hit. British credit tightened, the land boom collapsed, and nine states defaulted. By the time the economy recovered, the railroads had arrived. They were faster, they didn’t freeze, and they could be built almost anywhere. Many half-finished canals were paved over and used as rail beds. The 468-mile Wabash and Erie Canal, the longest ever built in North America, was sold to the Nickel Plate Railroad in 1881.

The railroads then ran the same play. Through the 1880s, they laid track furiously, financed by high coupon bonds and European capital, well beyond what traffic could support. The Philadelphia and Reading collapsed in February 1893. The Northern Pacific, Union Pacific, and Atchison, Topeka, and Santa Fe followed inside a year. By 1897, companies owning about a third of US railroad mileage had passed through bankruptcy. The track kept running. The equity didn’t. The capex from each boom became salvage value for the next.

You don’t have to go back two centuries. My first job out of undergrad was at Lucent. My tenure lasted seven months. At its 1999 peak, Lucent was the most widely held stock in America, with 5 million shareholders and a $250 billion market cap. Lucent, Nortel, and Cisco lent money to their customers, mostly telecoms and dot coms, so the customers could buy their gear. Revenue looked great until the customers went bankrupt and couldn’t pay back the loans. Lucent fell from $82 to $0.58. Cisco wrote down $2.2 billion of inventory in a single quarter and lost 85% from its peak. Most of the fiber laid during the boom went dark for a decade.

All three rhyme with what’s happening now in data centers. The questions worth asking are how loudly and whether it matters for a portfolio.

The Setup Today

The five largest US hyperscalers plan to spend roughly $700 billion on capex in 2026, about a 60% jump from 2025. Capital intensity measures how much a company spends on physical assets relative to revenue. At these companies, it has passed 50%, which is utility territory, not software. The Mag 7 has now redirected essentially all of its operating cash flow into AI infrastructure, with buybacks down 64% from a year earlier.

Cash flow has funded much of it, but not all of it. In 2025, hyperscalers raised more than $100 billion in debt to bridge capex against operating cash flow, with analysts projecting roughly $1.5 trillion of issuance over the coming years. Oracle alone carries over $100 billion in debt against negative free cash flow to fund its $300 billion contract with OpenAI. NVIDIA has committed up to $100 billion to OpenAI, which uses that capital to pay Oracle, which uses the revenue to buy chips from NVIDIA. Bulls call it a virtuous circle of locked-in supply and demand. Bear’s note that vendor financing has a history.

The Parallels

Three echoes are worth taking seriously.

-

- The certainty of the projection. No state legislature in 1836 wrote down a probability distribution for canal returns. The future was canals. Today, nearly every hyperscaler earnings call frames capex as “supply constrained, not demand constrained.” Both bets require the assumed end state to arrive roughly on the assumed schedule.

-

- The asset life problem. The buildout assumes 5 to 6-year depreciation schedules for GPUs that Nvidia is refreshing annually. Microsoft’s CEO put it plainly: “I didn’t want to go get stuck with four or five years of depreciation on one generation.” The bull rebuttal is that older GPUs cascade down to inference. The bear rebuttal is that the cascade only works if there are buyers at each step.

-

- The financing structure. State canal debt was secured by future tax receipts not yet collected. Northern Pacific bonds were secured by land grants and freight that hadn’t yet materialized. Lucent’s revenue was secured by loans to customers not yet creditworthy. Today’s capex is mostly funded by operating cash flow at strong companies, but the marginal dollar, including Oracle’s bonds and the Nvidia to OpenAI to Oracle loop, takes on the structure of forward commitments collateralized by demand that hasn’t yet arrived.

Where the Parallel Breaks

A canal had no alternative use. A terrestrial data center has reusable inputs (power, fiber, land, cooling) that can host whatever ground-based compute comes next. The wrinkle is whether the next computing generation stays on the ground. Bezos, Musk, and Google are all funding exploratory work on orbital data centers, where solar is constant, cooling is free, and none of the terrestrial inputs apply. The economics are likely a decade or more from competitive, and plenty of credible voices think they will never close.

The valuation backdrop is the bigger break. Earnings underneath the buildout are growing at roughly 13%, and the forward P/E on the index has contracted rather than expanded over the past year. That is not the shape of a bubble. Today’s price growth is backed by real profitability, not narrative. Lucent’s revenue depended on financing customers who couldn’t otherwise buy. Most of today’s capex is funded by companies whose existing cash flow can absorb the spend.

Does it Matter?

For a portfolio, in my opinion, “Is AI a bubble?” is the wrong question. The data doesn’t look like a bubble to us, but that is almost beside the point. The right question is whether the portfolio is built to survive either outcome. If the buildout pays off, you don’t want to have missed it. If multiples on the debt-funded names compress when capex growth slows, you don’t want that to be the thing that breaks the structure.

The lesson inside each of these episodes is the same. The canals got built. The railroads got built. The fiber got laid. What did the damage to investors wasn’t the buildout. It was a concentration in the wrong piece of the capital stack at the wrong point in the cycle. The people who came out of 1842 or 1897 or 2002 with their compounding intact weren’t the ones with the highest conviction call. They were the ones whose portfolios were built to absorb the drawdown (reach out if you’d like to read up on JD’s perspective).

That kind of portfolio doesn’t require knowing which outcome arrives. Our belief is that it requires owning the upside in a form (ie, options-based, not just long equity) that doesn’t blow up on the downside, and a defensive sleeve (uncorrelated, not just bonds) that actually defends rather than leaning on the same factors as the offensive sleeve. The call gets made by other people. The portfolio has to be ready either way.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2606-6.