On their own, bonds have been better in 2025 than in recent years. Capital appreciation across the complex may be limited from here, but the bigger story is the support this environment can lend to overall economic conditions. A few key themes that are emerging…

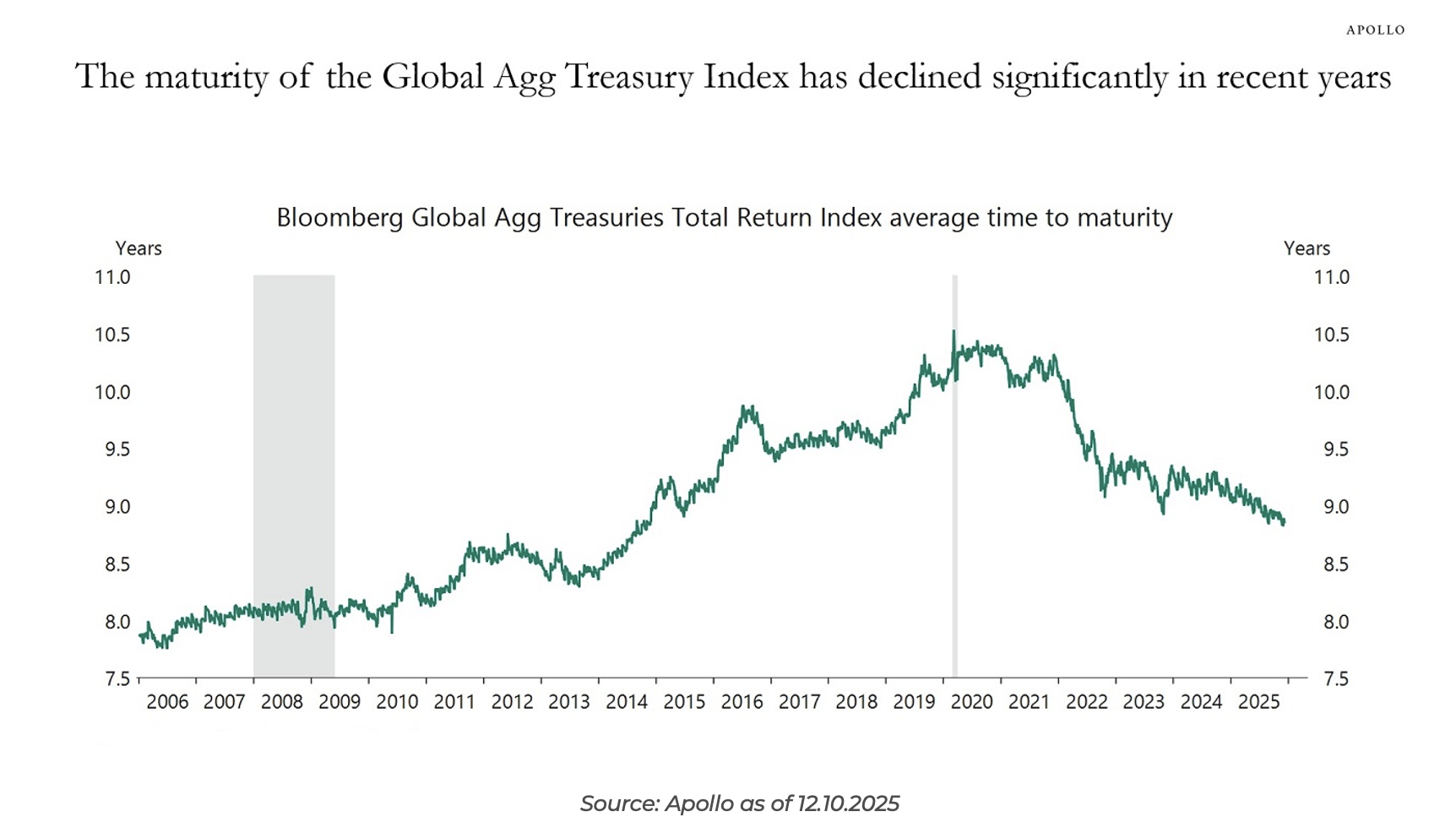

Shorter Duration on the Global Aggregate Treasury Index

With steeper yield curves, governments globally are issuing more short‑dated paper to minimize debt‑servicing costs. As a result, the average maturity of the sovereign bond index has been declining. The consequence is that monetary and fiscal policy have become more tightly linked, because a lower maturity makes government interest expenses more sensitive to central bank rate decisions. As long as interest rates keep moving lower, this is, on net, a good thing as the interest burden should decline.

We imagine many sovereigns learned their lesson back in 2020/2021 (many did not issue long-duration bonds at historically low interest rates), and I’d bet they will try to extend duration if rates get low enough.

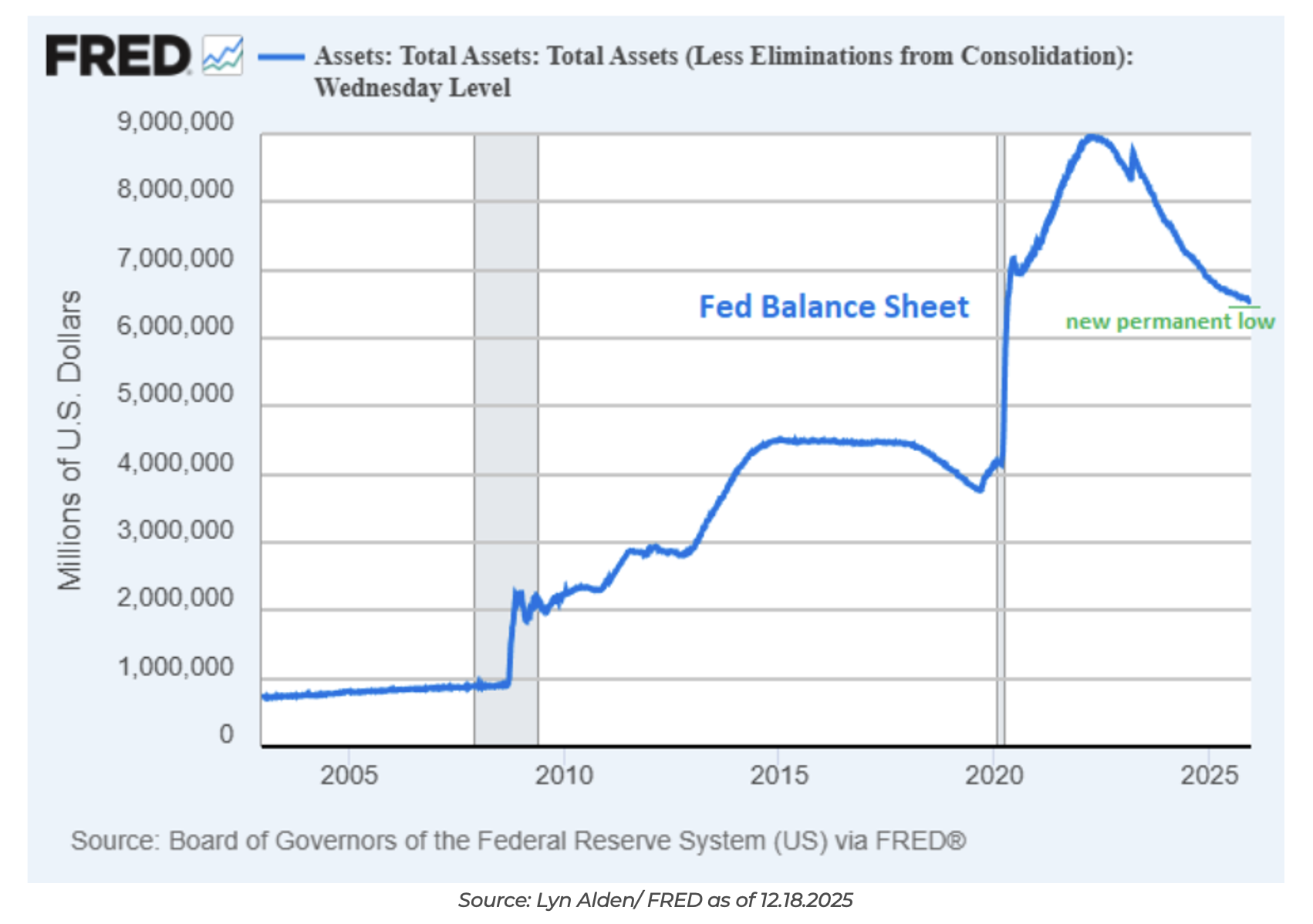

QE is Back. Reserve Management Purchases (RMP)

Over the past two years, GDP has grown by ~$1.5 trillion per year. The Fed’s balance sheet is around 20% of GDP, and they want to keep it around that percentage moving forward. That means roughly $300 billion in net balance sheet expansion per year.

Conveniently, right at the $25 billion per month baseline figure Powell mentioned regarding the Reserve Management Purchases (RMP), once the temporary $40 billion per month surplus liquidity period ends. Considering the Treasury’s stated goal is to issue between 15-20% of total debt via T-Bills, and a $2T deficit, that would imply $300-400bn of net new T-Bills per year. Assuming the Fed purchases $25bn T-Bills per month ($25bn x 12 = $300bn), Fed purchases could consume the bulk of new T-Bill issuance.

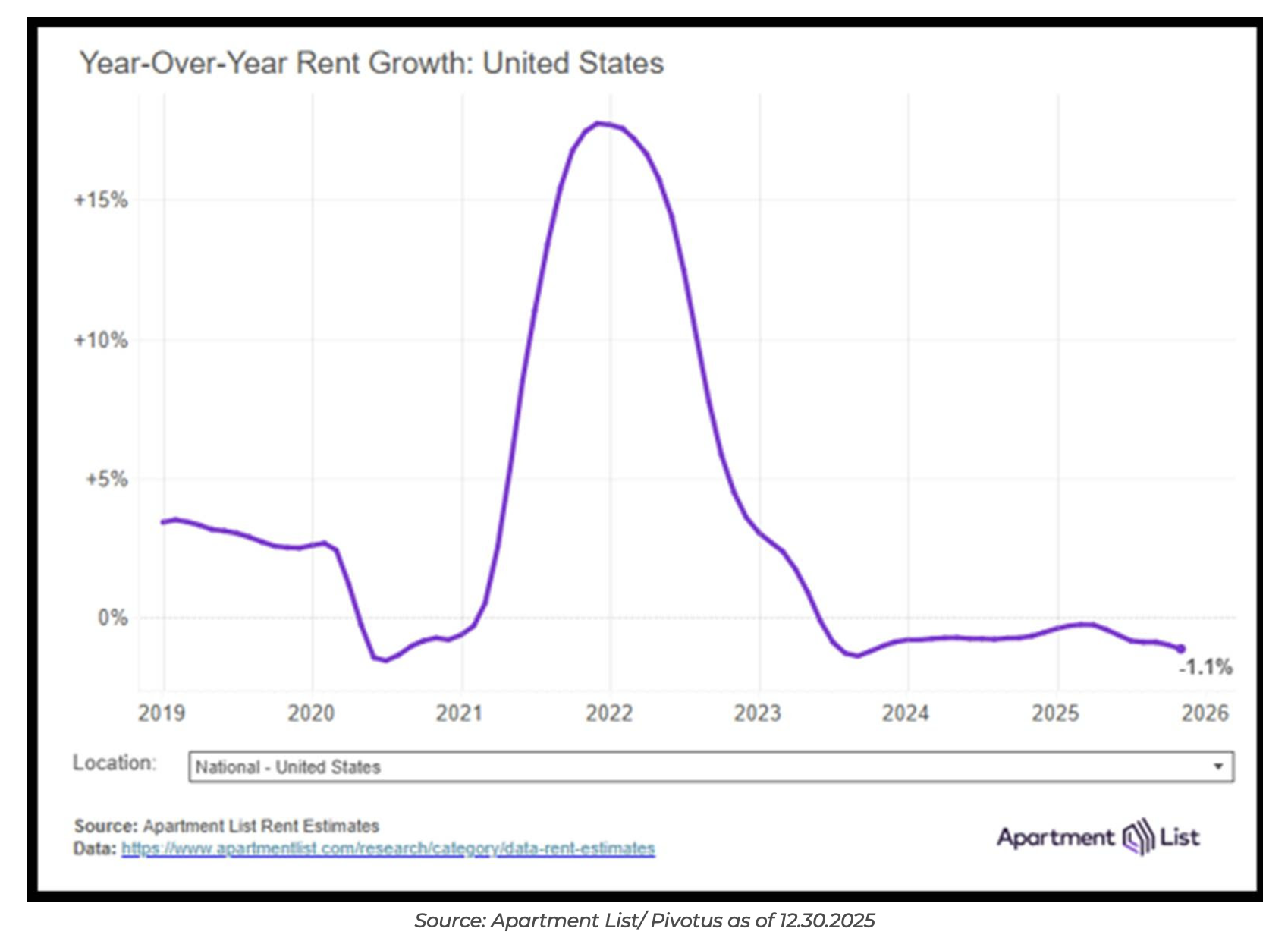

Housing Inflation Turning Negative

The Shelter component comprises 36% of CPI. This is broken into several categories: Rent, Owners’ Equivalent Rent, and Lodging Away from Home.

These factors tend to correlate, but with various lags, even as much as three years. According to Apartment List, rental prices have been negative for over two years and are currently -1.1% YoY.

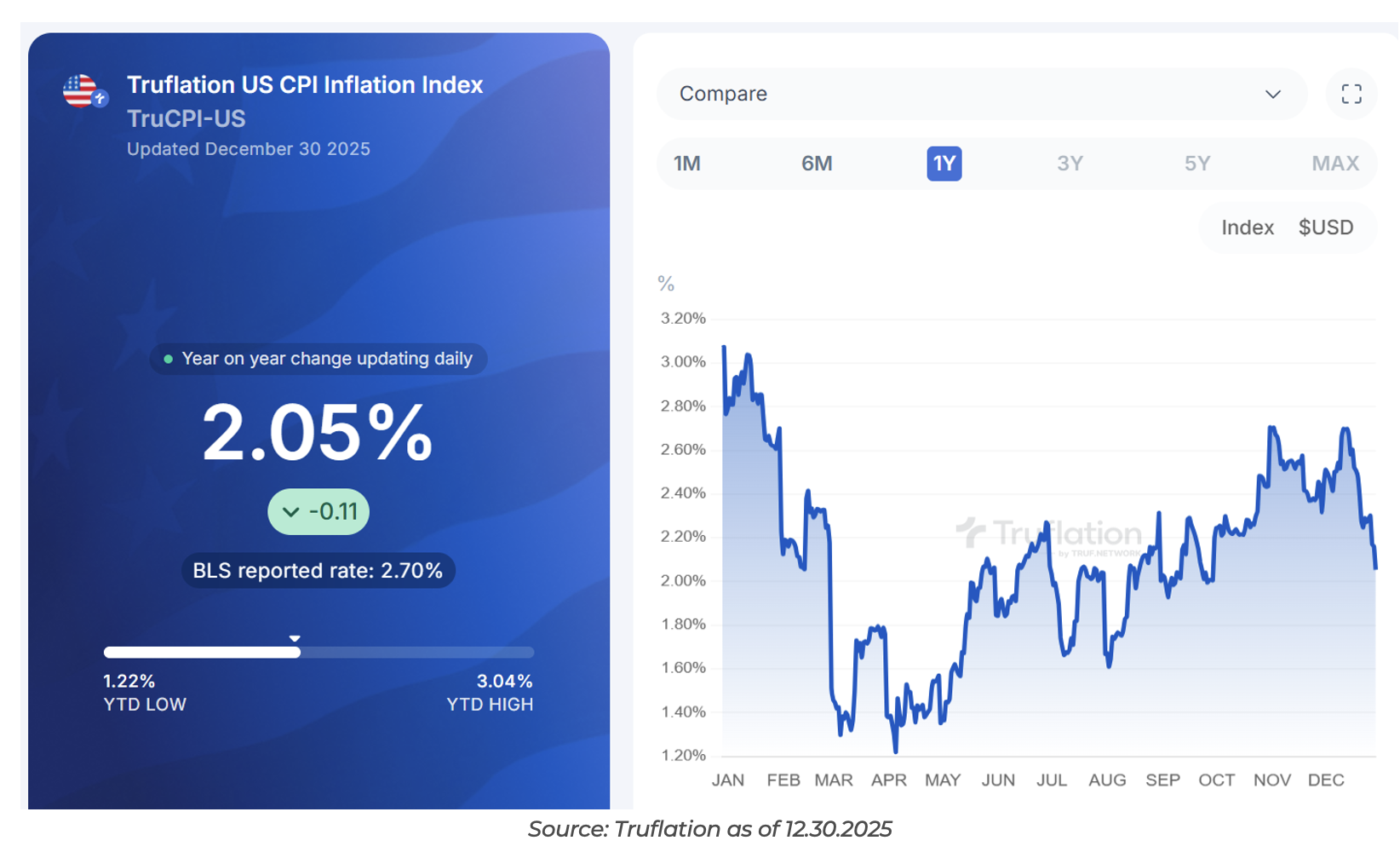

As housing inflation declines, given the large weight in its calculation, it should pull aggregate CPI down with it. While no one is expecting it, there is a possibility of CPI dipping below the Fed’s target in 2026. This could allow for more rate cuts than the market is currently expecting (~2.4 cuts, or ~60bps in 2026). In fact, Truflation US CPI Inflation Index is currently at 2.05%, 65bps below the most recent BLS reported rate of 2.7%.

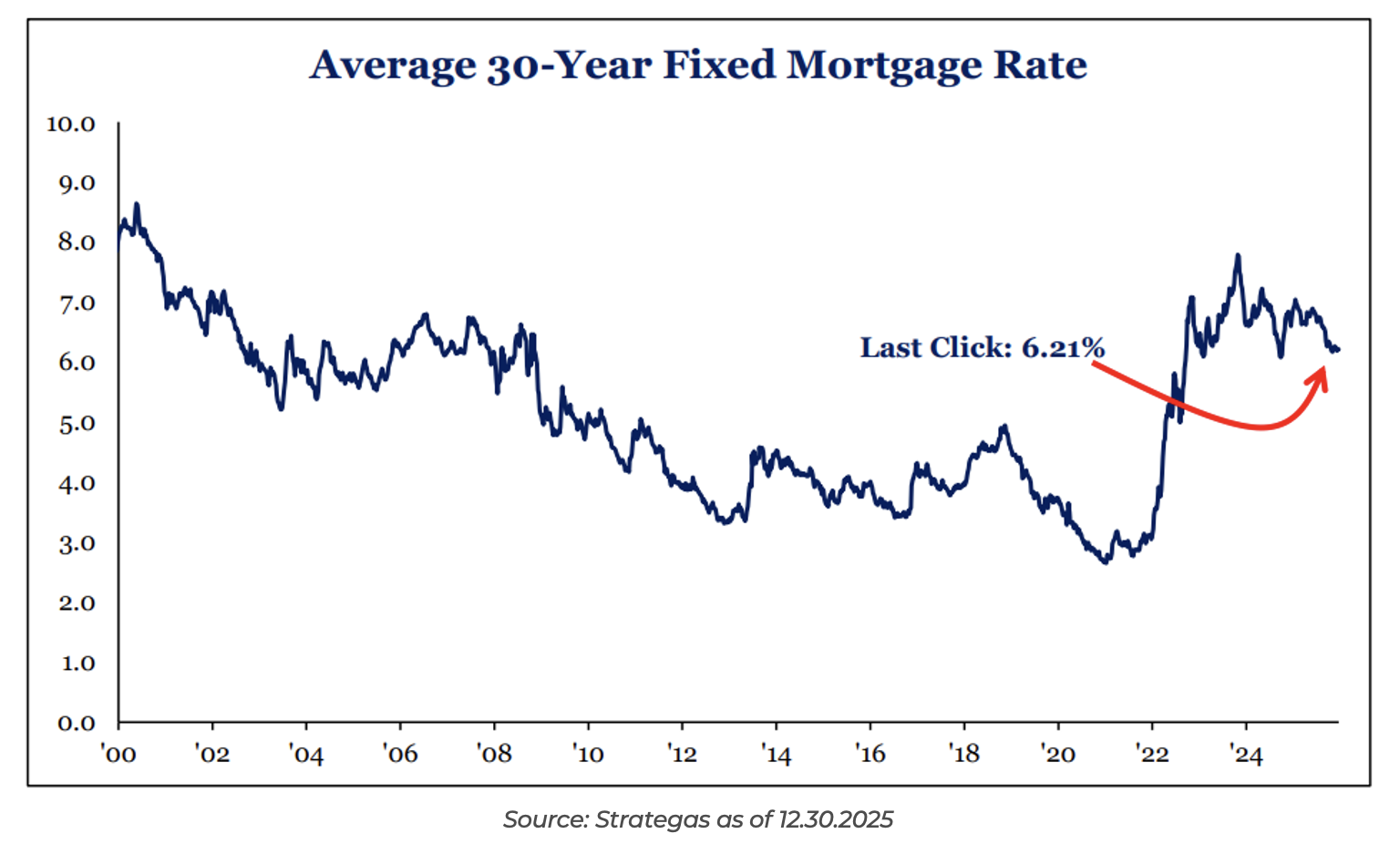

Declining Mortgage Rates: Another Bullish Catalyst for Consumers

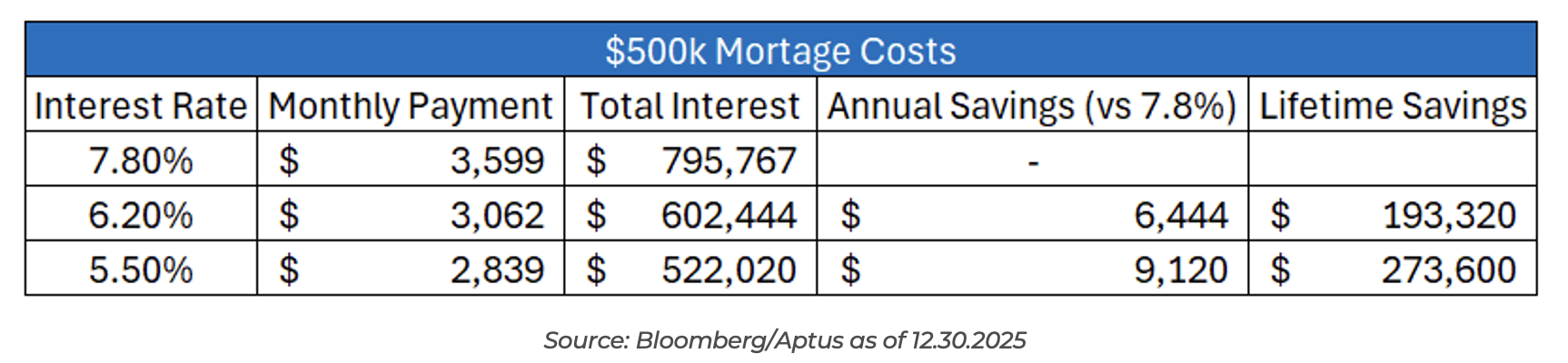

While the “Portable Mortgage” idea could be the next iteration of housing market financing, we won’t have clarity until next year. In the meantime, lower mortgage rates could help keep more cash in consumers’ pockets as they potentially save thousands annually by refinancing their mortgages. As the Fed has lowered interest rates, the long end of the yield curve has declined, dragging 30-year mortgage rates from ~7.8% in November 2023 to ~6.2% today. We believe there could be room for further decreases.

A person who holds a $500k mortgage with a 7.8% rate can save $537 a month to refinance their mortgage at today’s rate (6.2%). Taking that thought a step further, if mortgage rates were to decline to 5.5%, that same person could save $760 a month. Add that up over the life of the mortgage, and it’s hundreds of thousands of dollars (see lifetime savings column). I think 2026 could be a busy year for mortgage refinance activity.

In addition, for the potential buyers on the sidelines, a lower mortgage rate (coupled with stagnating home prices) could be just the push needed to make an offer on the home they’ve been eyeing on Zillow. All in all, a set of helpful catalysts for consumers, corporations, and investors.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2512-30.