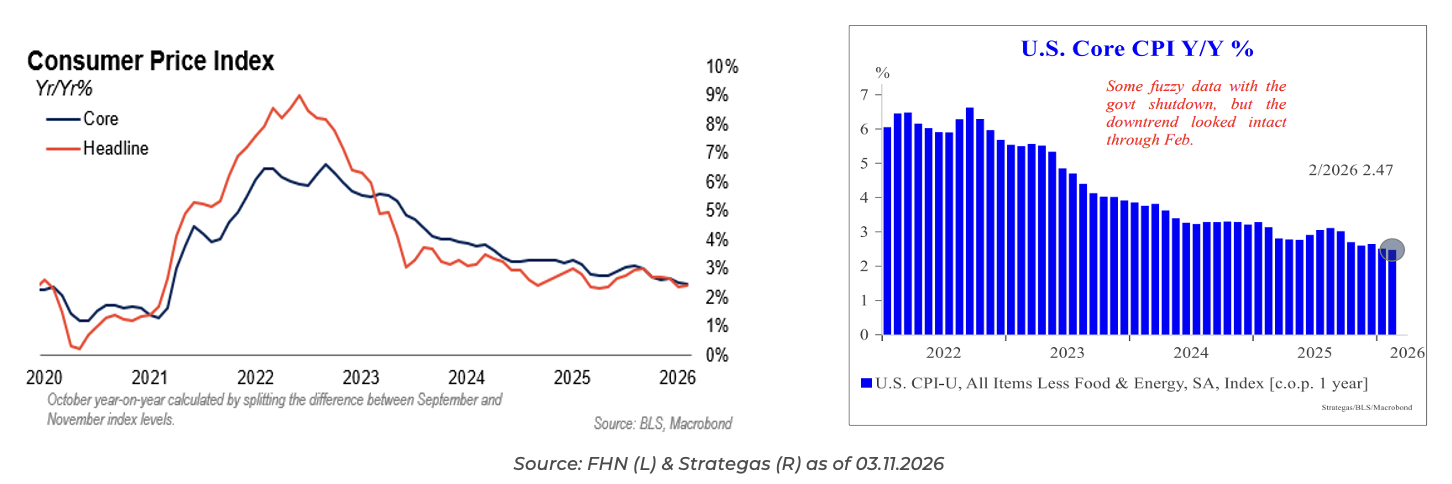

February CPI: As Expected

In February, the CPI rose 0.267% headline and 0.216% core, effectively matching the consensus of 0.3% and 0.2%. Year-on-year, the headline index was a tad higher, from 2.39% to 2.43%, while the core slipped a bit from 2.51% to 2.47%.

Food and energy inflation accelerated. Food, which rose just 0.18% in January, was up 0.39% in February. As for energy, it fell 1.46% in January but rose 0.63% in February. Gasoline prices rose 0.8%. Keep in mind this increase pre-dates the first Iran strikes and the higher oil prices we’ve experienced to start March.

In the core, shelter inflation was modest again. It rose 0.2% in both January and February, as did the owners’ equivalent rent. Shelter inflation is back to its pre-pandemic 2.5% annual range, with further improvement from here still possible. New vehicle prices were unchanged. Used vehicles fell 0.4%. Airfares rose 1.4%.

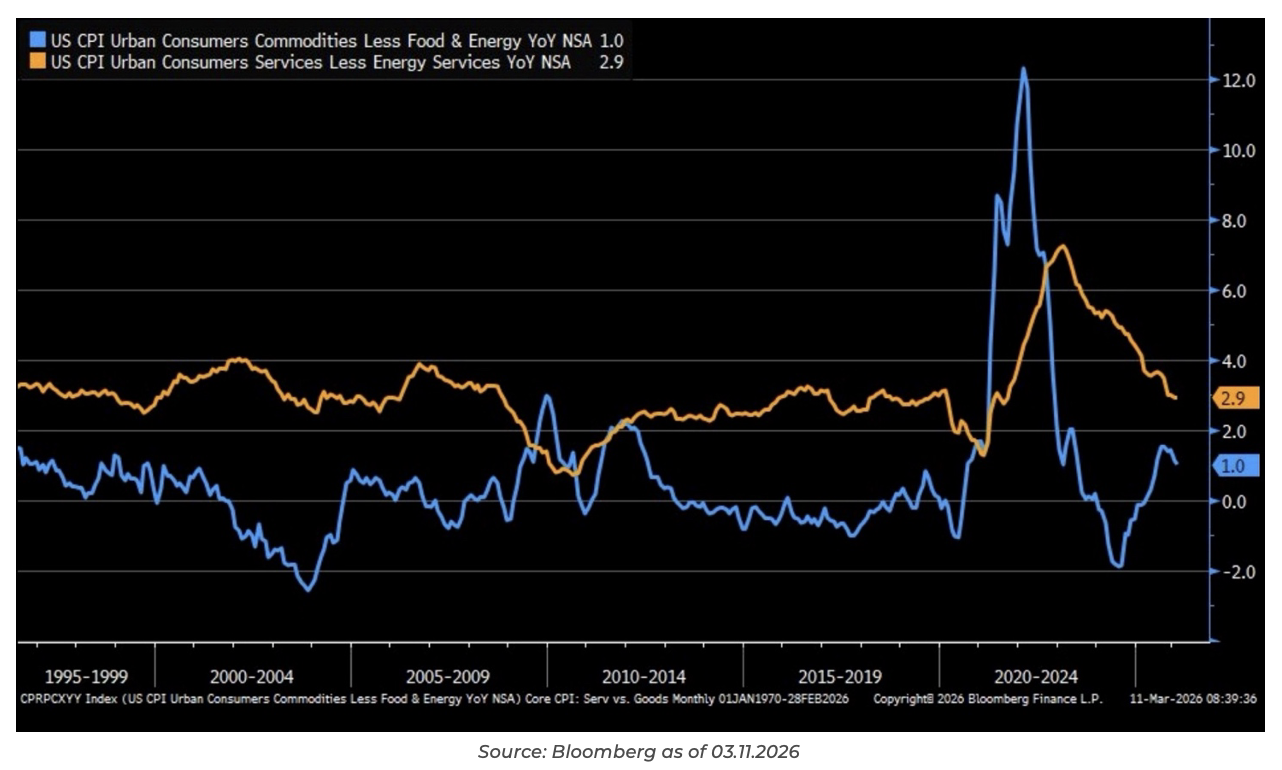

Core Goods / Core Services

Core services have been sticky high of late. For February, core services rose 0.3% vs. 0.4% in January. YoY the level is 2.9%. With a combined weighting of 61% in CPI, we need to see services decline to the 0.2% monthly range for headline inflation to continue trending towards 2.0%. Core goods eased slightly to 1% YoY, indicating the passthrough of tariff costs remains modest.

The Personal Consumption Expenditures (PCE) deflator data comes on Friday and is more relevant to the Fed. The PCE deflator has diverged from the CPI in recent months (CPI inflation falling while PCE inflation rising, due to PCE’s much smaller shelter component), so improvement in the core CPI just does not carry as much weight when the PCE deflator is expected to continue pushing higher.

These two indices rarely diverge and have never stayed divergent for long. In the past, re-correlation usually involved each moving toward the other, but sometimes it is just one. As a result, until they converge, it’s difficult to predict where inflation will end up.

Debunking Today vs the 1970s

While higher oil prices might bring back fears of the 1970s inflation, we believe the outlook and position of the USA today is quite different. Back then, CPI rose from a low of 5% to nearly 15% between 1976 and 1980. A couple of things contributed to the 10% increase in inflation:

1. The US was very dependent on imported oil, so oil-rich regimes were quick to exploit that situation with further supply constraints. Today, we internally supply our oil.

2. Unions had much bigger influence then, with most having cost-of-living adjustments (COLA) built into employment contracts. Unions now hold less sway in US labor markets.

In that environment, we saw that higher inflation led to higher wage adjustments (wage-price spiral), where markets expected that the inflationary cycle would persist (hence the spiraling).

That was a period of “unanchored” inflation expectations; this is not the case today (the starting point for inflation today is mid 2% vs 5% back then). Between anchored inflation expectations and fundamental differences in the oil and labor markets today, we believe there is a fundamental limit on price increases.

Lastly, there is a big difference between cutting monetary policy to neutral (still lower than where we are today) and taking a stimulative policy. Even through the commodity-related noise following the Iran attacks and ensuing spikes in oil, we tend to see the Fed look past supply-related shocks.

All in all, the CPI release was good, as core inflation has declined to its lowest level since 2021 for a second consecutive month. Following the report, stocks had a relatively muted response while the 10yr is yielding 4.19%, up 5bps, and the 2yr is yielding 3.62%, also up 5bps on the day.

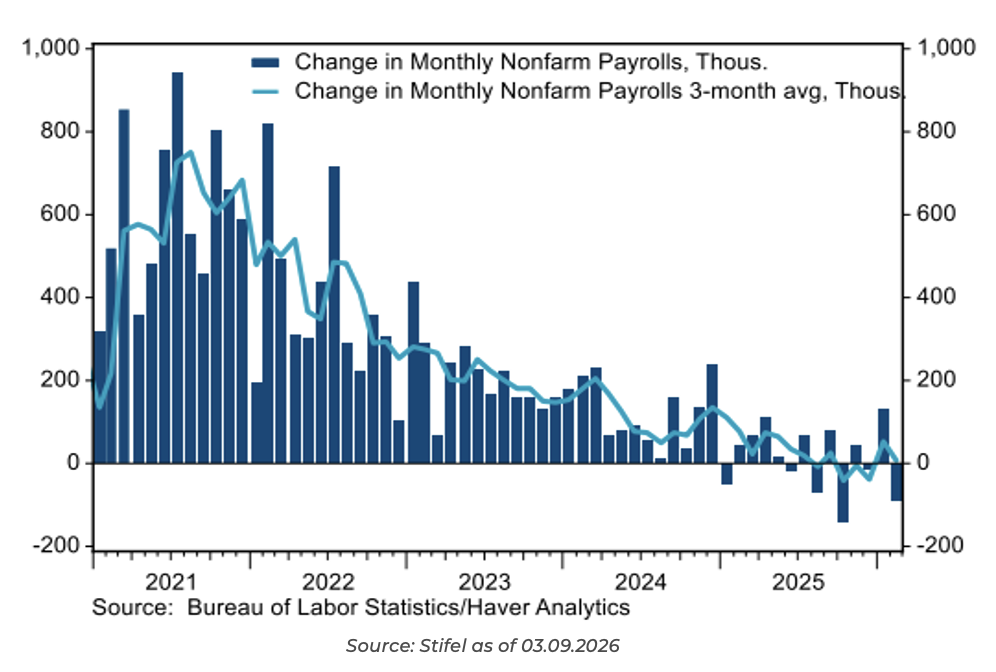

Weak February NFP

Nonfarm Payrolls declined -92k in February, which was well below forecasts for a +60k reading. January was also revised slightly down to +126k from +130k. The Labor Force grew by +18k while the Household Employment figure fell -185k. The headline U3 Unemployment Rate inched up to 4.4% as the broader U6 rate declined to 7.9%. Notably, the Participation Rate dropped to 62.0% as those not in the labor force increased by +72k. Wages were up +0.40% month over month.

The weaker-than-expected February employment report, following a stronger-than-expected rise in January, keeps uncertainty high on the underlying trajectory of labor market conditions. The lack of clarity will intensify the divide at the Fed between officials concerned about a weaker labor market and those focused on still elevated inflation. Bottom line is the three-month job creation average remains minimally positive, with a still relatively low unemployment rate and solid earnings/ economic growth.

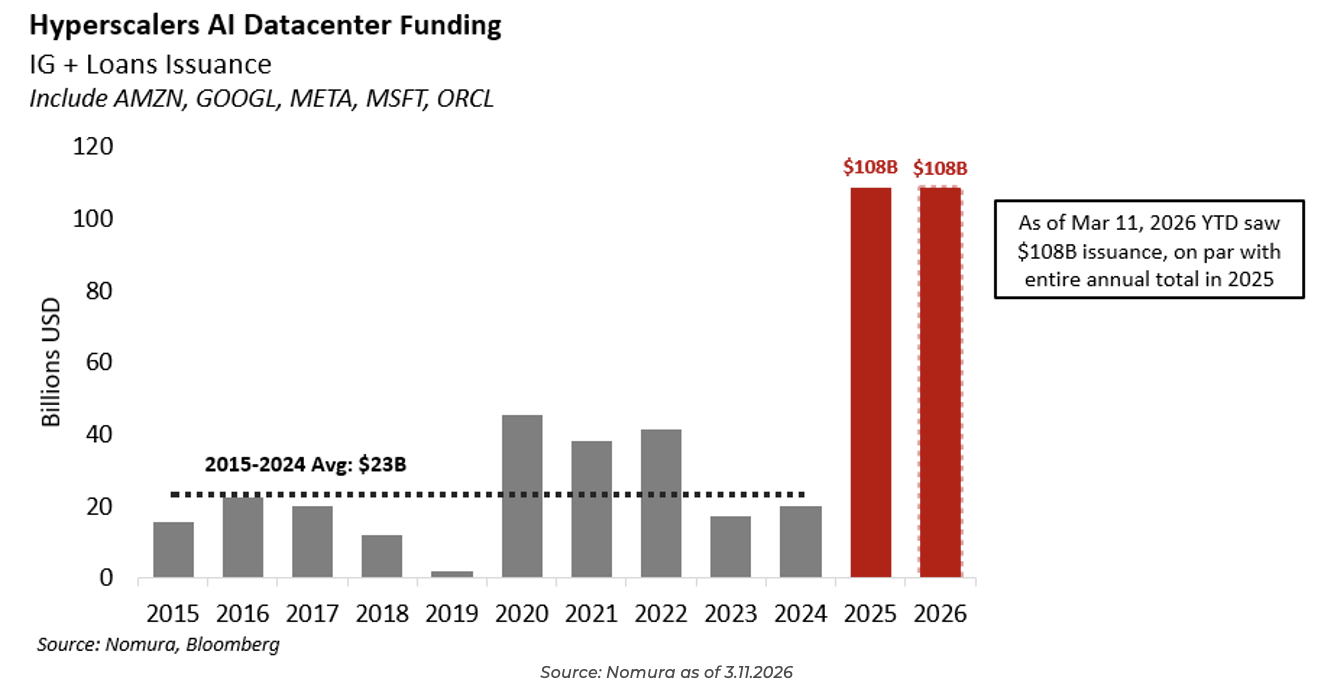

Hyperscaler AI Funding Update

Another pressure affecting rate markets has been the massive hyperscaler bond issuance we’ve seen to start 2026. The good thing is that BofA believes we have already seen 75% of what’s expected for the whole year. As this supply works its way through the markets, we’d expect less upward pressure on yields (at least from the private sector) as supply is absorbed by investors.

The fear from here is the crowding out effect of the private sector taking money away from Treasury market buyers into the backdrop of massive Treasury issuance. There will be ~$1.9 trillion in issuance from the ’26 deficit + $1 trillion in interest expense + $10 trillion in maturities that will need to be rolled over.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2603-13.