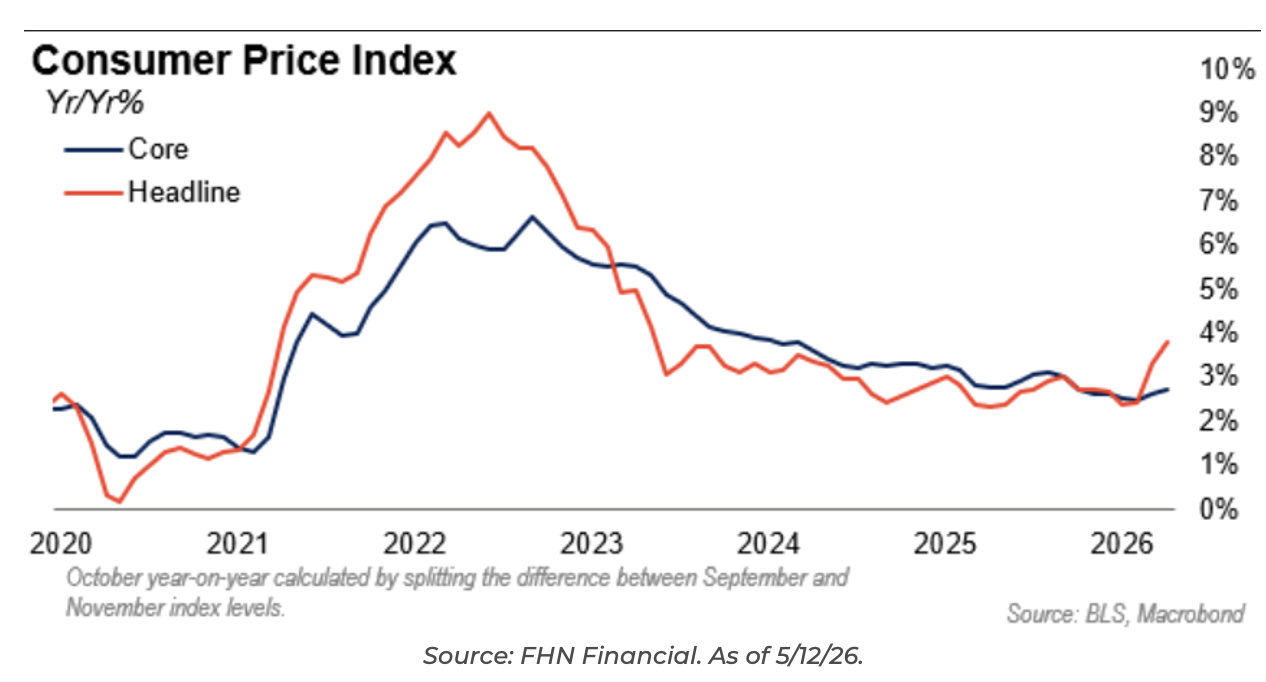

Core CPI (ex-food and energy) rose 0.38% in April after rising 0.20% in March. The Year over Year (YoY) Core rose from 2.60% to 2.74%. Headline CPI was up 0.64% on the heels of a 0.87% increase in March, both months elevated by higher fuel prices. YoY CPI inflation rate rose from 3.29% to 3.78%, hotter than expected.

A few key details from the report:

-

- Energy prices rose 3.80% in April, including a gasoline price rise of 5.44%. Gasoline is up 28.4% year-on-year.

-

- Food prices rose 0.50% in April and 3.22% year-on-year.

-

- Within the core, shelter rose 0.61%, even more than the Owners Equivalent Rent (OER), which rose 0.53%. This appears to be a technical correction from the missing readings registered during the 4Q govt shutdown.

-

- New vehicle prices fell 0.16%, and used vehicles were unchanged.

-

- Airfares rose 2.81% and are up 20.71% year-on-year.

April CPI was not as bad as it could have been. Energy inflation lifted the headline inflation rate to 3.8%, responsible for 40% of the increase, but energy price spikes have always been transitory. Of course, as learned after the pandemic, there are different speeds of transitory. The lack of a quick resolution to the stalemate in the Strait of Hormuz is stretching out the period of high prices.

The food increase is also notable, and when combined with energy, may start to impact discretionary spending as the US / Iran conflict continues. Shelter was an upside surprise, but Core categories were somewhat muted and trending lower. Looking ahead, if we see next month’s print accelerate higher, then the bond market may stop looking through the inflation print, which can already be seen in bond yields and Fed policy expectations.

Caveat of the Report

While Core CPI rose from 2.6% to 2.8%, it partially reflected the reversal of bad math from last October’s report, which caused the Core rate to be understated for six months. Several data lines, especially homeownership costs, were set to zero last October, which corresponded to a four-tenths drop in the core inflation rate from 3.0% to 2.6% between the September and November CPI releases. There was no October release due to the shutdown. Keep in mind that the data was bad for six months, making the inflation reports during November through March artificially low. Most will focus on the pop-up in the chart, showing inflation accelerating higher. Bear in mind, it increased from a low that was built around bad data.

Fiscal Response Could be Dicey

Central banks that are worried about inflation are likely to be hesitant to support their local economies with fiscal policy. Moves such as gas tax suspensions or checks to consumers risk exacerbating the inflationary impulse. The root cause of the current shock is the supply-chain problem due to the conflict in the Middle East. Stimulus can cushion the growth impact, but not the price consequences. On a positive note, inflation does appear to remain anchored, whether it be longer-term expectations or wages.

Rate Impact

The FOMC is mostly united in thinking the best course for policy is no change in rates. If core inflation keeps creeping higher due to sustained energy inflation, the fringe of members supporting possible hikes will grow. Market odds of a rate hike next April have increased to 70%, reflecting traders’ fears that inflation will be sustained.

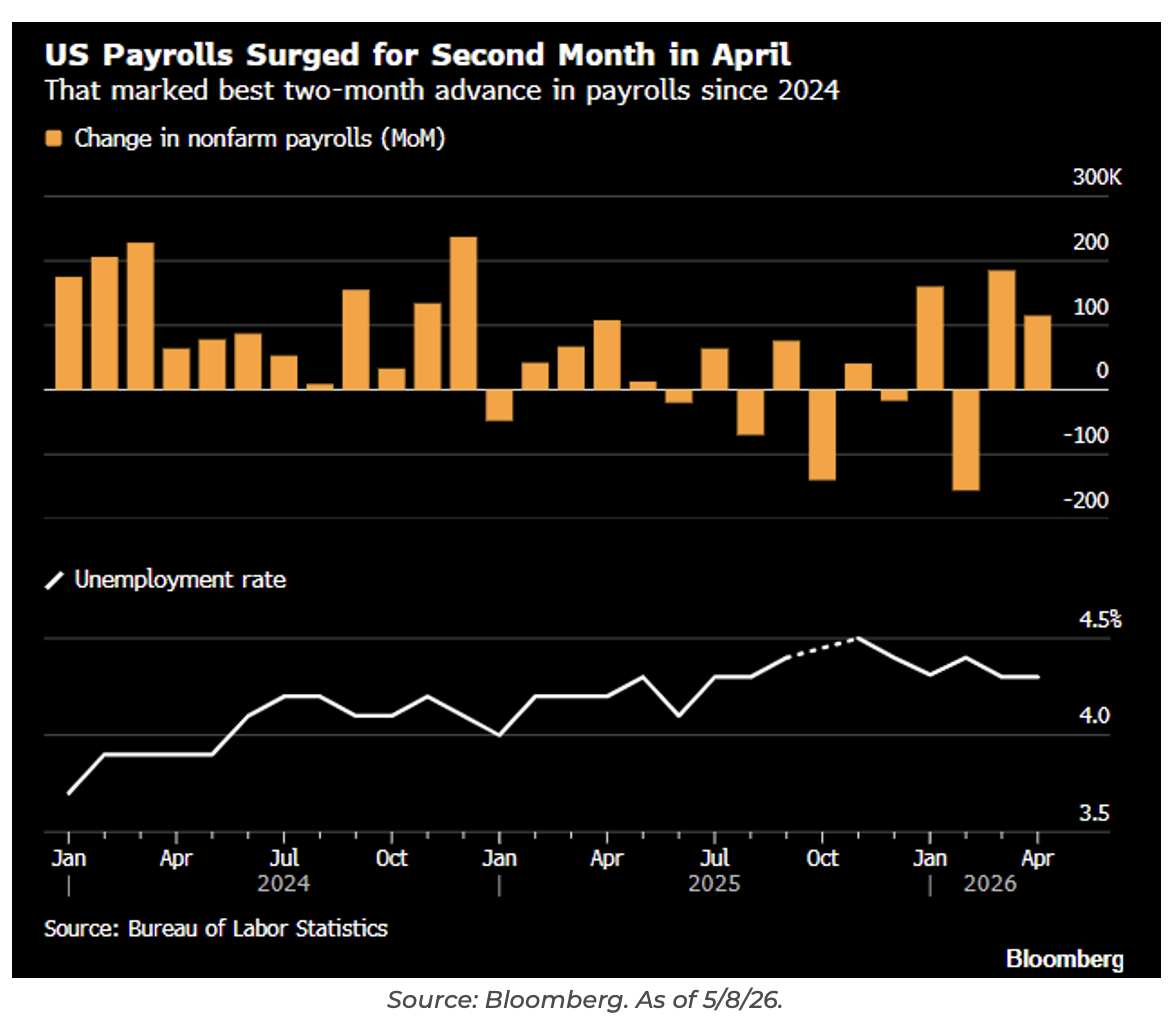

Employment Update

Nonfarm payrolls for April rose by 115,000, well above the 65,000 increase expected in a Bloomberg-compiled survey. Private payrolls growth slowed to 123,000 in April from 190,000 the month prior, the BLS reported, surpassing the consensus estimate for a 75,000 gain. The unemployment rate was unchanged at 4.3% in April, in line with Wall Street’s estimates.

Key details from the report:

-

- Average Hourly Earnings MoM (Apr) 0.2% vs 0.3% est/0.2% prior

-

- Average Hourly Earnings YoY (Apr) 3.6% vs 3.8% est/3.5% prior revised to 3.4%

-

- Labor Force Participation Rate (Apr) 61.8% vs 61.9% est/61.9% prior

-

- Underemployment Rate (Apr) 8.2% vs 8.0% est/8.0% prior

Another solid print aligns with the underlying thoughts that the US economy is chugging along just fine. Looking at the Middle East Conflict, if the situation is resolved soon, it could be another catalyst for lower inflation, lower oil, lower yields, and higher stock prices.

This report should give investors confidence that stagflation or recession fears are unfounded, especially if the Iran conflict is nearing resolution. Ultimately, this is a strong report showing some signs of breadth and momentum in the labor force/hiring sectors after a stagnant job growth environment in 2025.

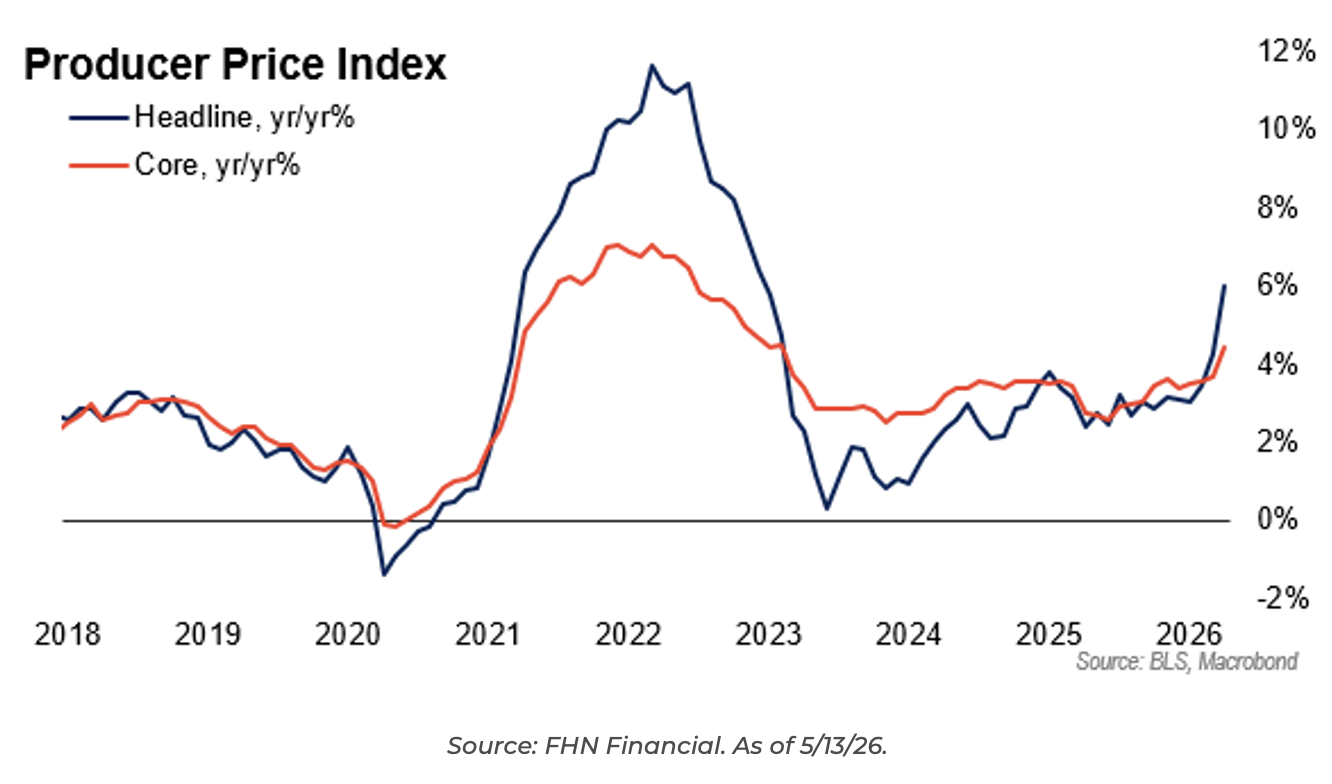

Producer Prices Surprise Higher

The PPI rose much more than expected in April. The PPI rose 1.4% in April, almost three times the 0.5% rise expected and the biggest monthly increase since a 1.7% rise in March 2022. The PPI rose 1.0% ex-food and energy, and the core PPI (ex-food, energy, and trade services) rose 0.6%.

Energy was up another 7.8% last month, now up almost 18% over the last two months. Even excluding food, energy, and trade, core PPI still rose 0.6% versus expectations for a 0.3% increase. Core goods prices rose 0.7% MoM, the second-largest increase in four years. Services prices spiked 1.2% MoM, almost eclipsing the largest increase from the ’21-’22 inflation cycle.

Contributing to the outsized gain in services were a 2.7% surge in trade services, reflecting wholesaler and retailer margins, and a 5.0% spike in transportation and warehouse services, reflecting higher costs to transport goods.

PPI Translation to PCE (Fed’s Preferred Measure)

The specific components from the PPI report that feed into PCE inflation were generally cool, with one exception: a 3.0% spike in passenger airfare PPI, a sixth-consecutive increase for the category.

Combining the CPI and PPI inputs, headline PCE is poised to rise 0.4% MoM, and core PCE to rise 0.2% MoM. This would bring both year-over-year rates to their highest levels since ’23.

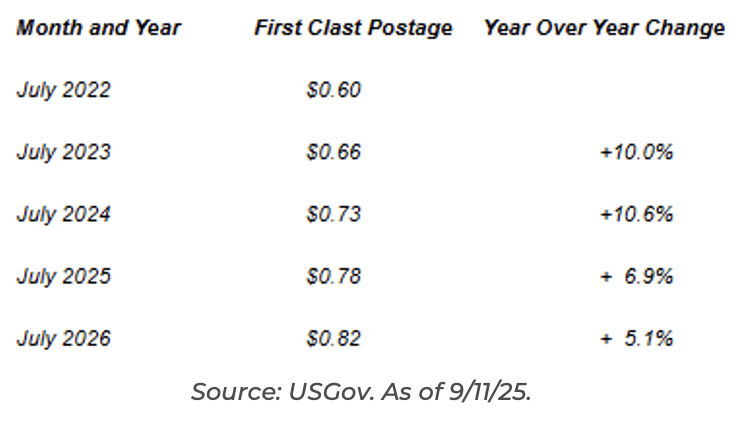

Another Measure of “Real Inflation”

CPI, PPI, PCE, “Breakevens”, Truflation… which one tells the real story? How about a simple one, the cost of stamps? Stamp prices have seen an 8.1% compound increase over the past four years to mail a letter (37% cumulative). This does not include the 8% fuel surcharge the U.S. Postal Service imposed starting April 26, 2026.

Warsh Confirmed

Kevin Warsh was confirmed to be the Head of the Federal Reserve yesterday. The 54-45 vote on Wednesday was the slimmest confirmation margin ever for a head of the central bank. Split politics in Congress and Democratic fears that Warsh will bend to President Donald Trump’s demands to rapidly lower interest rates remain fears.

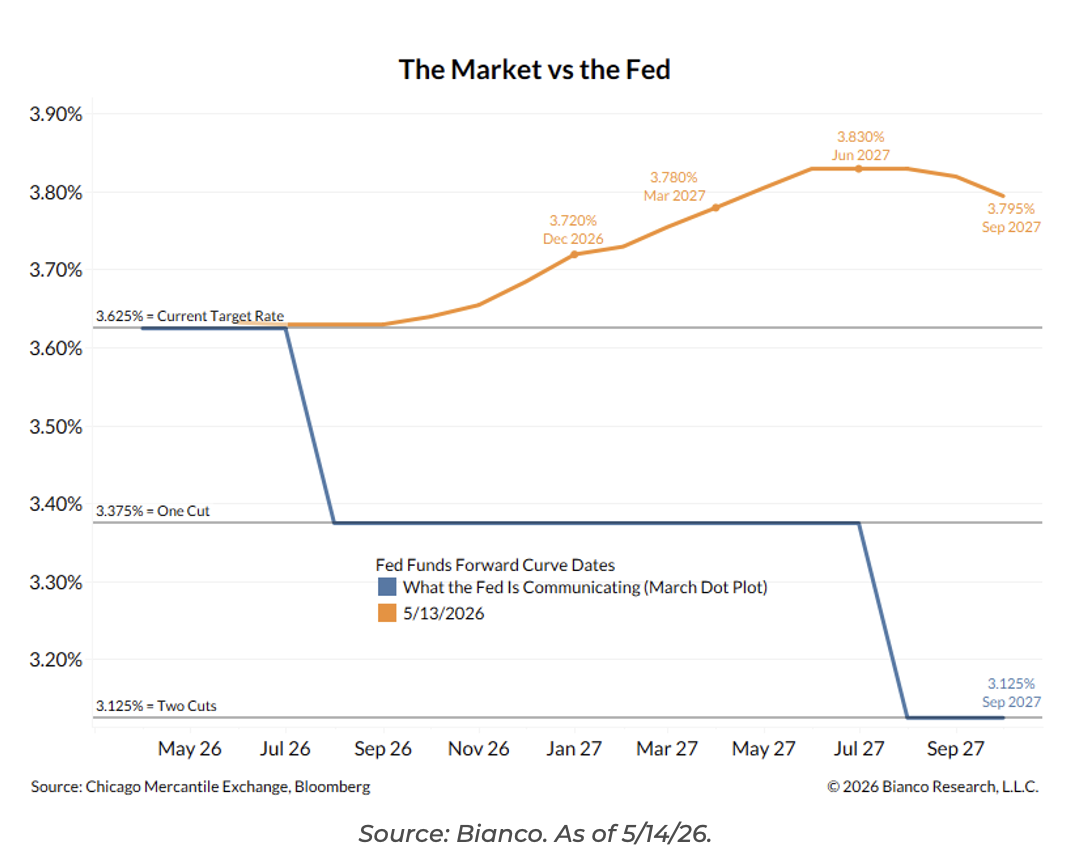

Warsh will face a series of immediate challenges as inflation rears its head following the Iran conflict, causing soaring gas prices. Additionally, there is a large divide in thought amongst the Fed committee, given the current backdrop. The difference between market expectations for future Fed policy and the Fed’s March Dot Plot (although dated at this point) is stark. Markets keenly await Warsh’s first FOMC as chair, which comes in roughly a month, on June 17th.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2605-14.