The FOMC release was less hawkish than feared (milkshake) with a dovish presser (cherry on top). We view December 10th’s move as a risk management cut given a slowing job market and limited inflation fears (we’re above target, but inflation break-evens show limited worry). The policy rate is now 175bps off the highs, given the 75bps of cuts in ’25. I do think today’s 25bps cut (as well as the lagged impact from past cuts) will make a difference for a large chunk of corporate America, given the size and scope of small and mid-sized businesses in the US economy and their utilization of shorter-dated funding.

The Fed cut rates as broadly expected by 25bps, bringing the fed funds rate to 3.5%-3.75% by way of a 9-3 vote. The target rate now sits “within a range of plausible estimates of neutral”. The Statement of Economic Projections (SEP) was broadly in line with consensus expectations (more on this below). There were three dissents from the committee, the first time since 2019. Chicago Fed President Austan Goolsbee and KC Fed President Jeff Schmid dissented in favor of leaving rates unchanged. Fed Governor Stephen Miran dissented in favor of a 50bp cut.

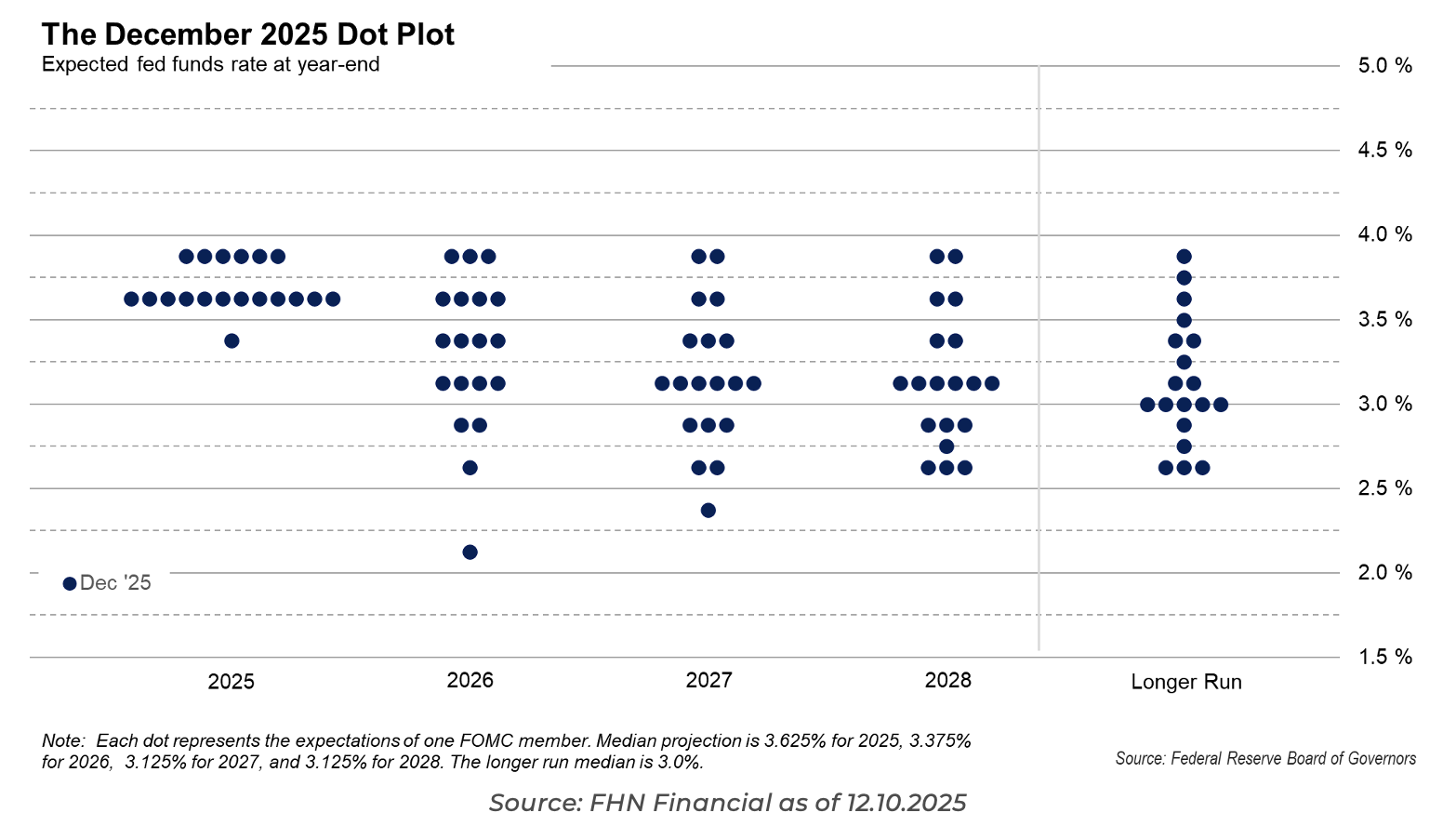

Updated Dot Plot

The dot plot showed six of nineteen FOMC participants submitted “soft” dissents (two of which were Goolsbee and Schmid) by placing their end-2025 dots 25bp higher than where today’s policy announcement moved the fed funds rate. Governor Miran also submitted a soft dissent (lowest dot).

The median rate in today’s dot plot reflects one 25bps rate cut in 2026 to finish the year at 3.25% – 3.50%, essentially unchanged from the September forecast. The elephant in the room is that we will have a new Fed Chair in May, and given Trump’s very vocal desire for lower rates, the market is pricing in an additional rate cut compared to the Fed’s projections. This is not surprising.

The FOMC statement noted that committee members are debating the “extent and timing of additional adjustments”. We now await three months of new payroll data and two months of new CPI data released before the January meeting. The committee appears to be content with pausing while they gather more data.

Reserve Management Purchase = Balance Sheet Expansion

As far as the Fed’s Balance sheet goes, the policy statement noted that as “reserve balances have declined to ample levels”, the Fed will begin buying up to $40bn of T-bills (up to 3-year notes) the first month, starting on Friday. Per Powell’s press conference, we can expect these purchases to continue for the next couple of months and then proceed as needed after that based on market conditions. We’d note that while the purchases are not officially Quantitative Easing (“QE”) and are merely a move to improve liquidity in reserves, they are on net, likely accommodative to liquidity.

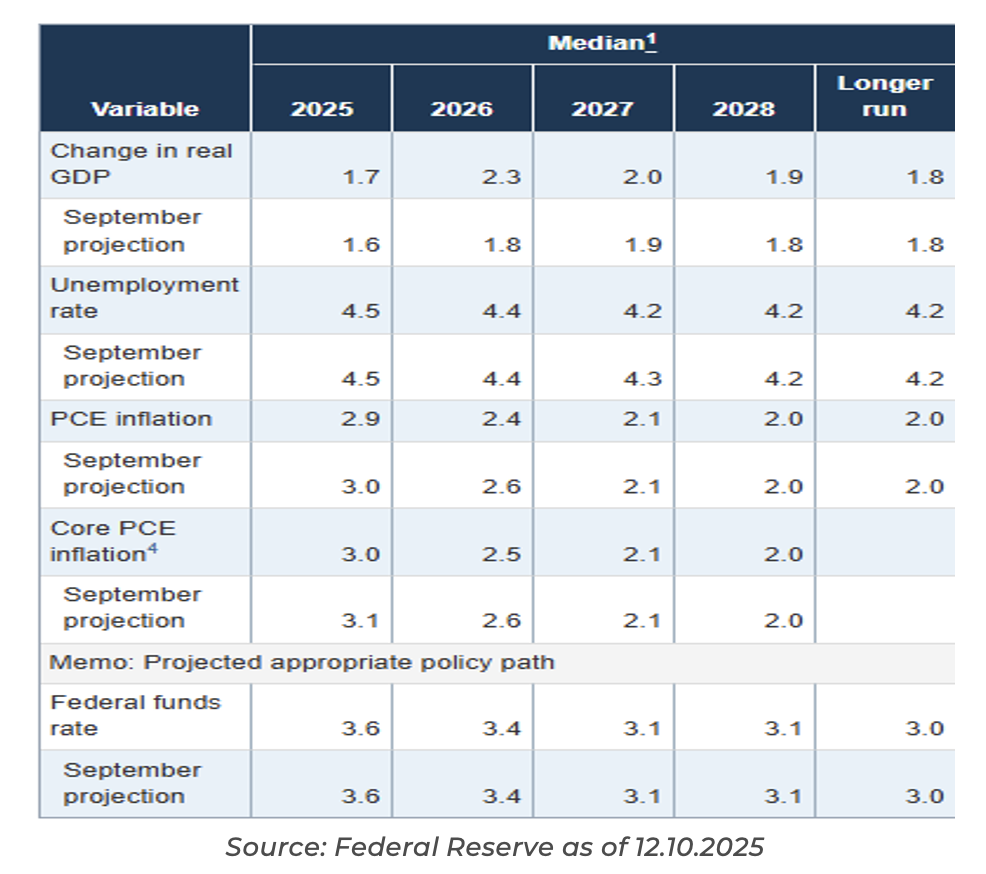

Statement of Economic Projections

Median GDP projections increased between this year and next from 1.7% to 2.3%, although Powell noted that about 0.2% moved from ’25 to ’26 due to the government shutdown. Median projection for PCE inflation is expected to fall 0.1% by end of year 2026. Median projection for unemployment rates in ’26 and ’27 declined by 0.1%. There were green shoots in regard to productivity increases, which helps the case for continued economic growth and moderating inflation.

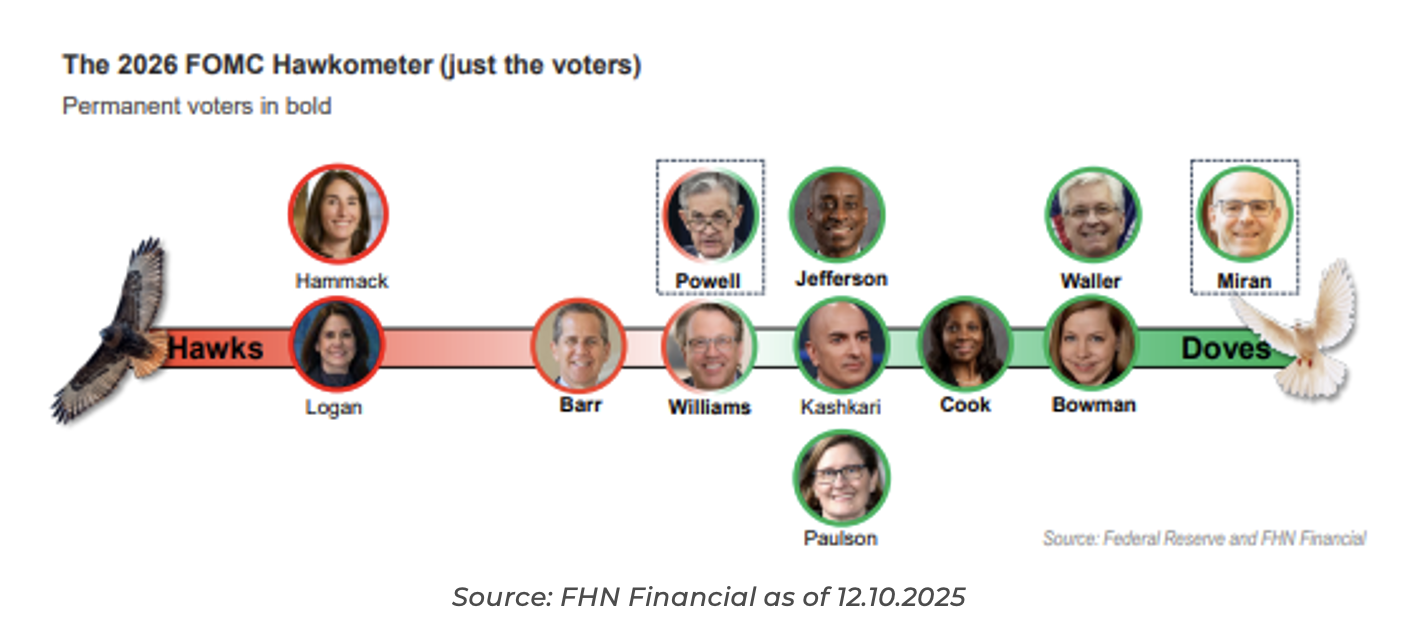

2026 FOMC Voters

The composition of FOMC voters will change over the first half of next year, so the nuances of today’s guidance won’t mirror the nuances of the Committee’s views in just a few months. With President Trump expected to announce his pick for the new Fed Chair before the January meeting, I think Chair Powell’s press conference will be a somewhat weaker indicator of the future FOMC point of view. In my opinion, it’s safe to say that next year’s FOMC voters will be more focused on the job market and less focused on inflation than this year’s voters.

Closing Thoughts

One area that we think could currently be overlooked is that, as the Fed cuts rates, the impact on the deficit could be more powerful on the way down than it was on the way up, given we are basically a floating rate borrower (huge amount of recent issuance has been on the front end of the yield curve). This could prove another bullish potential catalyst for 2026.

As rates fall, nominal GDP should feel a boost (or at least remain elevated) as lending increases, given that a steeper yield curve and lower rates aid growth. Between lower interest expense and higher tariff revenues, the debt concerns could be moving in the right direction, which could keep the long end from rising sharply.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2512-15.