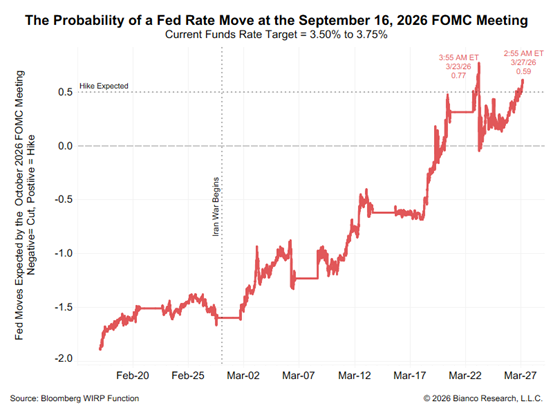

Market Pricing Fed Hikes?

The probability of a Fed hike in September has risen to nearly 60%. The 2-year Treasury topped 4% and is trading ~39bps above the target Fed funds rate (3.63%). Typically, you only see the 2 year this far above the fed funds rate when the Fed is hiking interest rates.

Data as of 3/27/26

The 10- year Treasury yield has popped above 4.46%, it’s highest level since last May, rising >50bps since the Iran conflict began. It appears at a minimum the Fed will be at an extended pause, as they assess the impact on inflation (and growth) from the spike in oil prices and general volatility in markets given the war.

While we do not see the Fed lifting rates into this commodity driven supply shock, we could see other central banks (i.e., the BoE, the ECB) with a single mandate of stable inflation being tempted to do so.

Market Impact

The current environment puts the Fed in a tough position in terms of setting their short-term interest rates. Shortages of raw materials combined with some economic weakness, along with large fiscal deficits, is a hard combo for them to address, given both sides of their dual mandate (maximum employment and stable prices) are simultaneously challenged.

We’d note that the markets are mostly treating the backdrop as a supply-driven inflation shock, not necessarily a significant growth shock. However, the longer things drag on, the more vulnerable the economy becomes to a more real growth scare. On a positive, if tensions wrap quickly, we could see a resumption of status quo (growth resumes, rate cuts priced back in, oil price stability).

Listening to Fed speak, you get mixed signals. There is a (shrinking) mix of officials that want to reduce interest rates to address weakness in the labor market, while other Fed officials want to hold rates steady and some even raise rates to try to combat inflation. While the “2 point something” inflation was likely acceptable given our 2% inflation target, “4 point something” likely is not. Keep in mind this oil shock comes in the wake of the Fed having well overshot its 2% inflation target for five straight years.

In our opinion, if either the US Treasury market or overnight financing market run into severe liquidity problems, the Fed will provide liquidity regardless of what inflation levels are at. The Fed has options available such as continuing the RMP policy ($55bn of monthly Reserve Management Purchases) beyond April, Treasury buybacks (soft QE), or upsizing bill issuance where buyer demand is still strong.

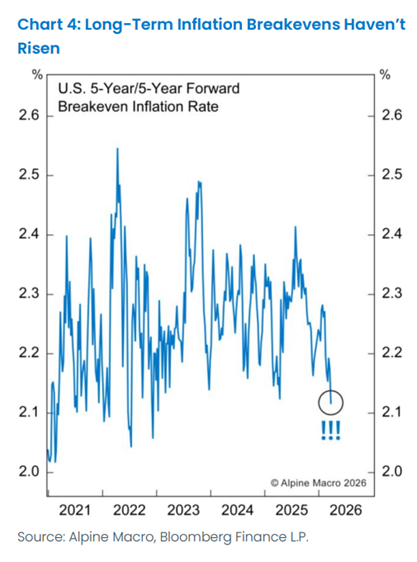

Longer Term Breakevens Appear Anchored

The 5-year/5-year forward inflation breakeven in the U.S. has not budged since the war started, and is holding near the lows of the past five years. The current 5-year/5-year forward breakeven rate of 2.1% is consistent with inflation running slightly below the Fed’s 2% target.

Data as of 3/26/26

Keep in mind inflation breakevens are based on CPI, while the Fed targets the PCE deflator. Historically, annual CPI inflation has outpaced the PCE deflator by about 0.4%. Therefore, roughly speaking, the CPI-based breakevens need to be around 2.4% to be in line with the Fed’s 2% target for the PCE deflator. TLDR: Markets are mostly treating the backdrop as a short-term, supply-driven inflation shock that will fade as tensions fade.

Bond Market Volatility is Elevated

Traditional diversifiers have been struggling during the recent market volatility. Since 2/26, TLT (Long Term Treasuries) is down -4.3% while GLD (Gold) is down -15%.

Source: Strategas. As of 3/27/26.

As we’ve noted for some time, bonds (duration) aren’t working as a hedge, as we are in a higher inflation regime, specifically one caused by a commodity price shock. Markets have repriced from presumed dovishness (2-3 cuts at beginning of the year) to impulsively hawkish given inflation cost pressures given the spike in oil prices.

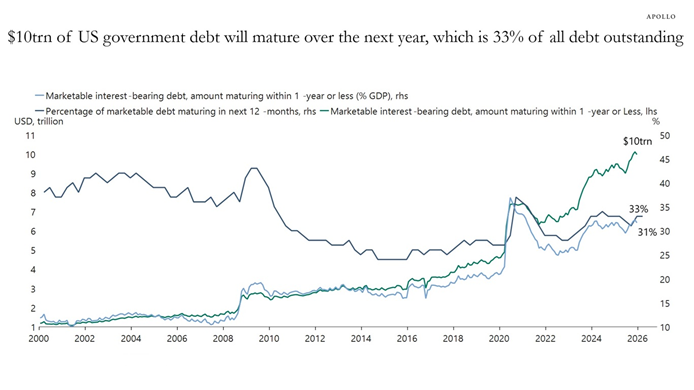

US Gov’t has a lot of Debt to Refi

Between US Treasury debt maturities, fiscal deficits, and interest expense, the US government will be selling about $12 trillion of new bonds over the next 12 months. This comprises about 33% of all the Treasury debt outstanding.

Source: Apollo. As of 3/27/26.

While most of this debt will rollover as investors replace their maturities, the nominal number is huge. In addition, there is a new competitor for capital from the corporate space that is expected to raise another $2 trillion due to hyperscale/AI buildout.

Deregulation efforts from the Trump administration are likely to be key to increasing investor capacity to take down all the supply. This factor could contribute to pressure yields higher across the yield curve.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2603-25.