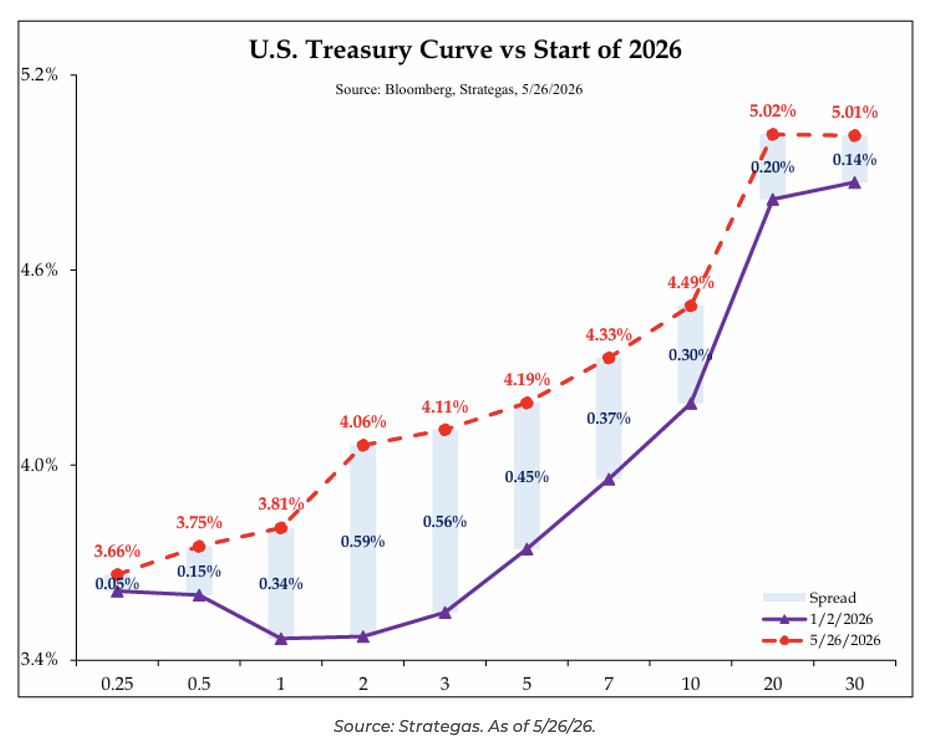

Treasury Curve Movements

The yield curve today looks drastically different than the beginning of the year. The largest increases have occurred in the belly of the yield curve, with 2s rising the most at a 59 bp increase since the start of the year, with lesser increases on the tails. Despite all the concern about rate hikes, the 3-month and 6-month yields have risen by just 5 and 15 bps. The fear of runaway inflation as well as government debt issues appears unfounded, given a mere 15bps rise in the 30-year Treasury.

The bulk of the Treasury curve repricing has been due to the energy price shock driven by the conflict abroad. The increases in the belly of the curve probably indicate that inflation will remain sticky in the intermediate term, forcing the Fed to hold rates unchanged or even potentially take them modestly higher. Ultimately (and maybe most importantly), if markets were truly seeing a second wave of inflation, rather than just sticky (slightly above target) inflation, we would expect to see significantly larger increases across the curve, especially on the backend.

Brookings Financial Outlook

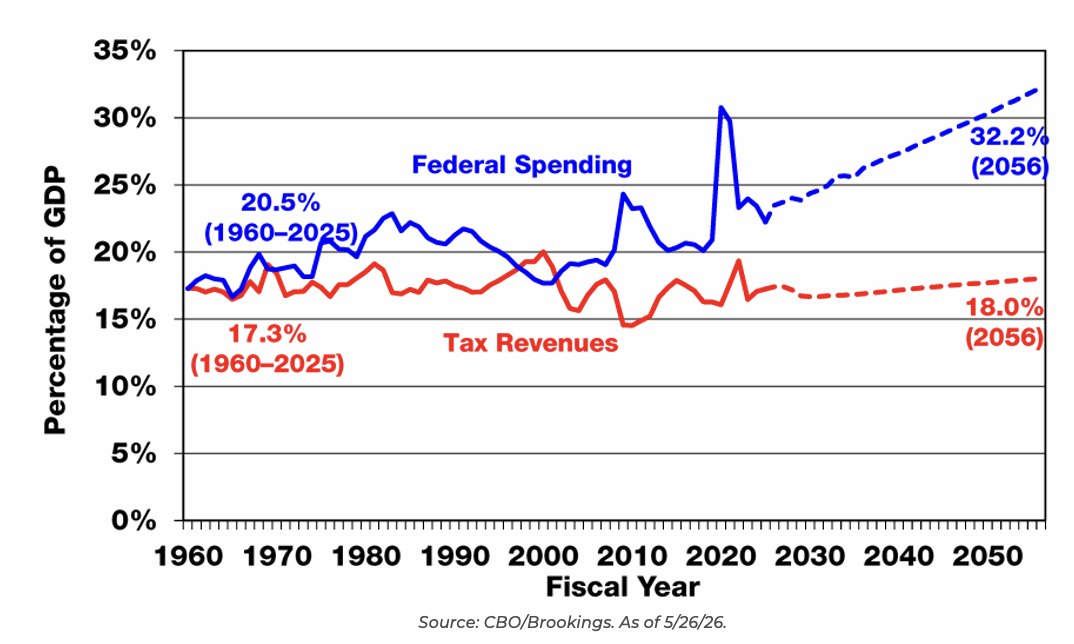

I came across an excellent outlook presentation from Brookings, which walked through financial projections for the US economy looking ahead over the next 30 years. The key thesis of the presentation is that the government debt load is here to stay and worsening. We are outspending our tax revenue base by a wide (and growing) margin.

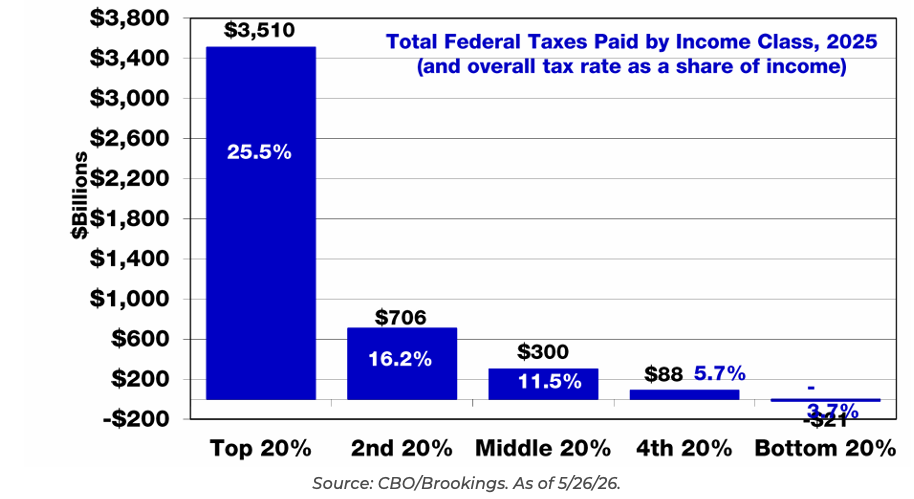

As shown, this isn’t a revenue problem but a spending one. The top 20% of taxpayers pay over 75% of the taxes. Higher taxes often prove counterproductive and don’t appear to be a viable solution. It appears cuts to entitlements could be the only potential solution; however, it will likely be political suicide if attempted.

It’s no secret that the US is running one of the largest budget deficits in the developed world. We continue to spend like it’s going out of style. This comes at a time when our debt load outstanding is growing quickly, and is further compounded by higher interest rates on our borrowing. While the current budget deficits are elevated, almost all future projections anticipate that there is no slowing down.

Even under the “rosiest” of scenarios (no wars, recessions, lower interest rates), the debt levels (compared to GDP) are projected to nearly double over the next 30 years. Throw in the unexpected, and it could be even worse, especially if it comes from higher interest rates, where the CBO estimates that each percentage point in rates higher will cost $3.3 trillion over the decade. Interest Expense is expected to become the largest Federal Expenditure by 2040, and within 10 years, they expect more than 30% of tax revenues to go towards interest on the debt.

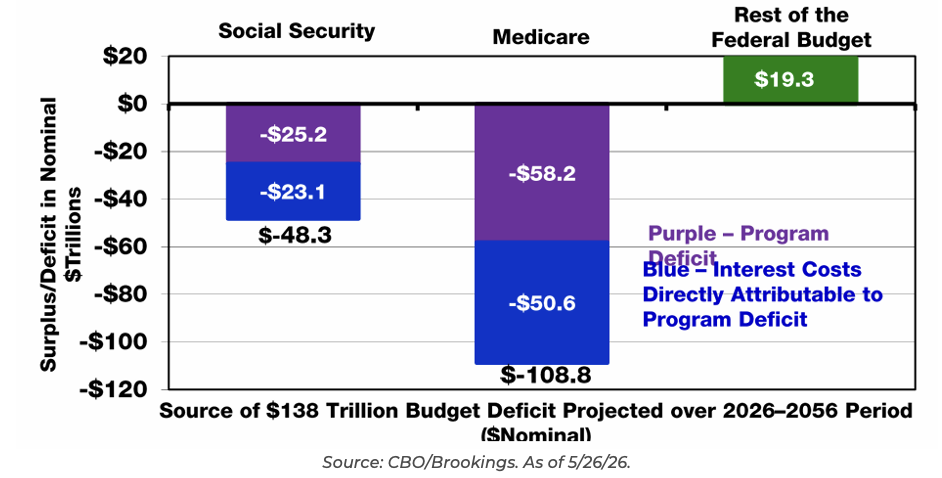

Social Security and Medicare Sucking the Government Dry?

CBO projects that by 2056, the budget deficits will be entirely driven by Social Security and Medicare shortfalls. Increases in financing costs only worsen this outlook.

Top 20% Pay Lion’s Share of Taxes

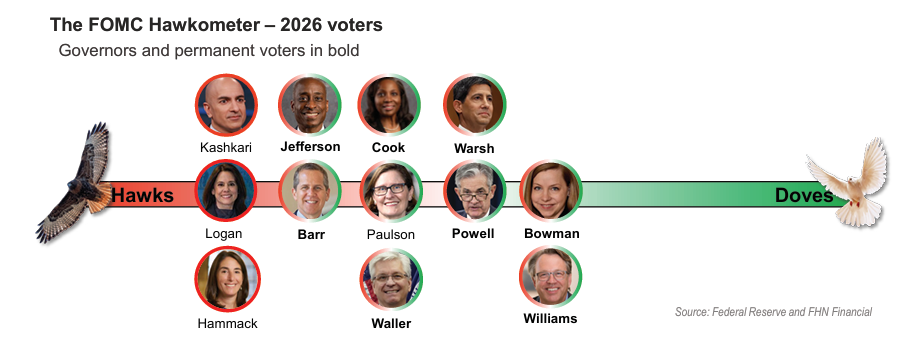

Warsh Confirmed: Challenges Likely Ahead

Kevin Warsh was officially sworn in as Chairman of the Federal Reserve, in a seat formerly filled by Stephen Miran on the Board of Governors. Warsh’s first FOMC meeting is on June 17. Kevin Warsh is known to be well-experienced and an effective communicator. That said, even by his own characterization, it’s much easier to call policy “from the bleachers” than in the hot seat.

History has shown that new Fed Chairs are often tested by the market. Both Bernanke and Yellen had early flubs. Bernanke’s first meeting was in March 2006, and Core PCE was right at the 2% target. Yellen took the reins in January 2014 with PCE Core inflation at 1.5% and non-emergency QE still running. There were no dissents at either Bernanke’s or Yellen’s first meeting.

Source: FHN Financial. As of 5/26/26

Source: FHN Financial. As of 5/26/26

Those were easier positions to begin with than what Warsh is taking over. And yet, both stumbled on communication, moving the market in a way they didn’t intend. Between a divided Committee, the inflation backdrop (5yrs above target and counting), the uncertainty around energy prices, Trump (and Bessent’s) meddling, Warsh’s plan for reforms, and the fragile fiscal circumstance are all complicating factors that Mr. Warsh must face head-on.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2605-24.