We are witnessing a monetary regime change. I’m not sure investors fully appreciate what that means. I know we talk about a lot of stuff, but I’m focused on this single concept below as it strikes me as the single most important thing I could point out to long-term investors.

Reserve Assets

Central banks hold things on their balance sheet that serve as an emergency savings account for a country. You tend to see reserves that are made up of things that everybody trusts. (Think gold, dollars, euros, etc.)

These reserves can be grabbed quickly to help pay for things the country may need. In short, reserve assets tend to be liquid and universally-trusted assets where central banks park funds to help back up their economy and currency.

For a long time, gold was THE neutral reserve asset used around the world on central banks’ balance sheets. Pre-1971, gold backed new money issuance, as money was redeemable for gold. Meaning, you could trade gold for dollars and vice versa. For every piece of paper money, there was gold in a vault, backing it to some extent.

Then, in 1971, we abandoned this gold-backed system and went to a fiat world where dollars can be freely printed and are backed by nothing and are redeemable for nothing.

I know, I know, some will say our military backs the dollar, but with our reliance on China for the manufacturing of equipment, that argument is less compelling than it used to be.

I’m simplifying things, but the deal was kinda like this: We’d export dollars to countries all over, and then those countries would bring those dollars back to us through the buying and holding of our Treasuries. For 50 years, we exported dollars while hollowing out our ability to build things, and that’s becoming a weakness in our negotiating power.

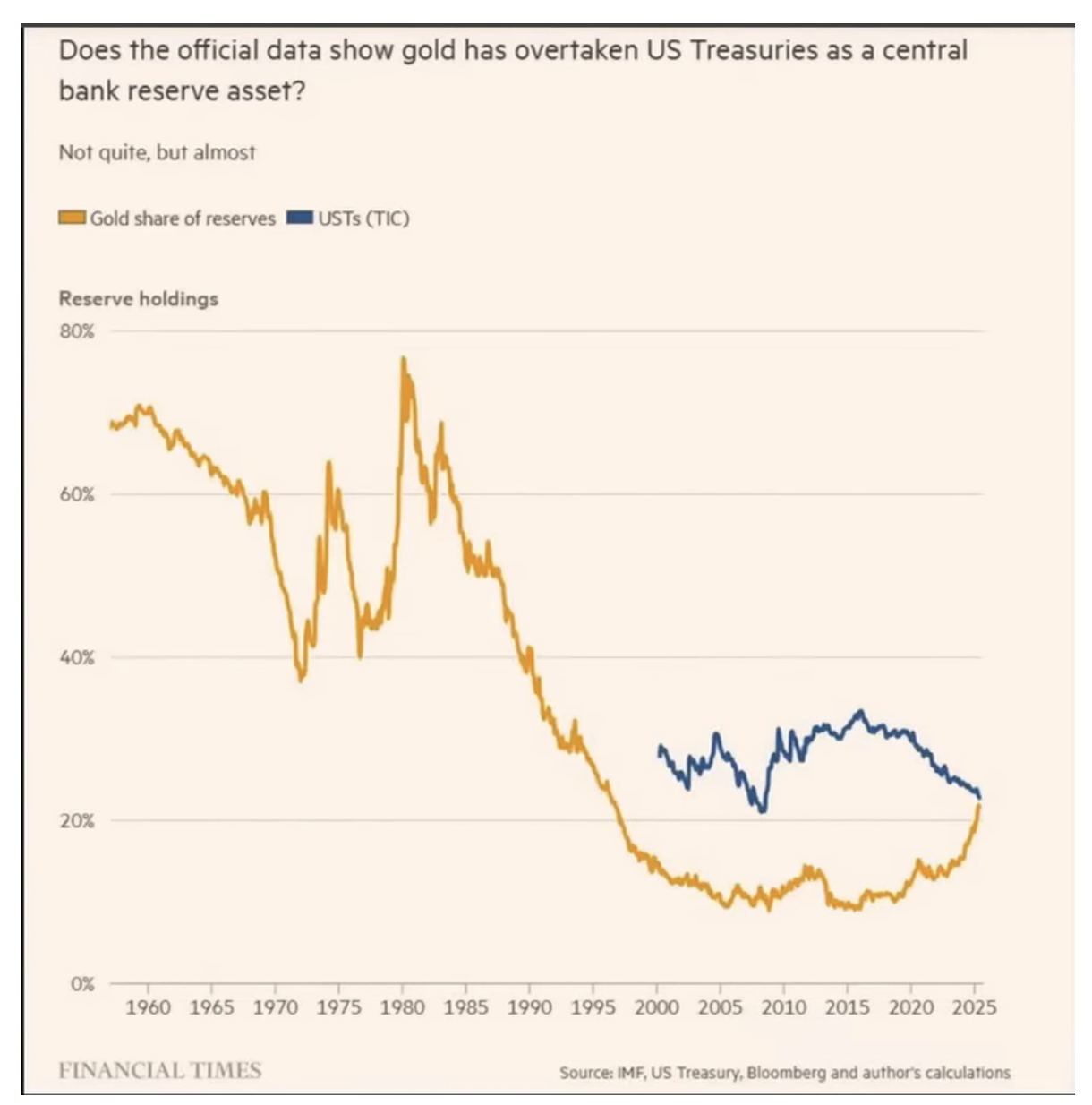

Now to the chart. In the early days of post-1971 fiat land, gold on central bank balance sheets dropped from a big number to high single digits. 20 years ago, it would have been a stretch for anybody to say gold would replace Treasuries as the number one central bank reserve asset. Well, it doesn’t look crazy now, as we are months away from that happening.

The image below is a chart showing the reserve holdings of central banks. You can see Treasuries dropping and gold rising rapidly. This is from a combination of central banks accumulating gold and the price of gold rising relative to Treasuries.

Data as of September 2025

Data as of September 2025

For the first time in a long time, we are reverting to the old ways. A neutral reserve asset is going to overtake U.S. debt as the preferred reserve asset. I believe the writing is on the wall, and central banks seem to agree.

Supply and Demand Issue

Two things are happening simultaneously:

1. We are going to need more Treasuries than ever before

2. Less buyers are to be found

Who will buy the bonds? If that answer is, “I’m not sure,” then at what interest rate can we find buyers? If that answer is higher, then is that interest expense sustainable?

You see the issues here? Lyn Alden calls it fiscal dominance. It’s when debt becomes an issue, and the easiest path out is to continually print money or suppress rates to keep the government solvent. In other words, the easiest path out is to inflate the debt away.

Bond holders, you’ve been warned.

I said it a couple of months back, but maybe now you can see why stablecoins are being championed by our government through the Genius Act.

This train is not stopping, and that’s why we urge investors to think clearly about the definition of ‘safe’. Central banks around the world sure seem to be.

The Battle at Hand

Free markets and capitalism are deflationary forces.

Productivity, efficiency, and competition lower prices. True free markets would create money that is constantly increasing in purchasing power. We are living through, just maybe, the most powerful deflationary force we’ve ever seen with the technological changes happening every day.

Meanwhile…

Fiat systems are built on debt, where new money is created through new lending. That means, fiat systems are debt-based, and rising inflation makes it easier and easier to service yesterday’s debt. They must have inflation.

This, in my opinion, is the battle we are witnessing: A system that needs inflation vs technological forces of deflation.

The Post-1971 inflationary system is trying to hold on and will not go down without a fight. Investors need to allocate accordingly.

Fiat Reminder

President Nixon addressed the country on August 15th, 1971, to announce a ‘temporary’ suspension of dollar-gold convertibility. He finished the address with this assurance, “Your dollar will be worth as much tomorrow as it is today.”

Since then, the dollar has lost roughly 88% of its purchasing power.

For a different perspective, gold traded for $35 an ounce in August of 1971. Today, an ounce of gold costs ~$3,800. I’ll let you do that math on the value the dollar has lost in gold terms, hint, it’s close to 99% and that’s not a typo.

The system that has led to this loss of purchasing power is arguably worse off than it has ever been. Real growth is a path out, and maybe AI creates it. Inflating the issues away is another path out. Maybe it’s one or the other, or maybe it’s a combo.

Either way, central banks are no longer as trusting in the safety of US bonds, and I don’t think you should be either.

Your Allocations

Asset allocation is ultimately what matters most. Given the backdrop, we prefer to own more stocks and less bonds.

For most investors, this shift can improve a portfolio’s ability to protect against eroding purchasing power. We expect stocks to do fine, and bonds to struggle. Therefore, let’s own more stocks, and avoid bonds as much as possible.

Our offset to address increased stock market risk is simply stock market hedges. We like hedges because of the convexity they carry, and the timing of that convexity paying off. Their presence allows us to own more stock market risk, because we’re prepared for left tail events. We believe this can lend itself to portfolios that are better in the tails. More participation in right tail (positive) environments, while avoiding the nasty part of left tails.

We continue to think risk assets go higher from here, but we will hold hedges just in case we’re wrong. Our goal is to compound capital, and think being better in the tails positions us to do just that.

As always, thank you for your trust. Please don’t hesitate to reach out with any questions at all.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.This should not be construed as tax advice. You should always consult with your tax professional with regard to specific tax questions and obligations. Outcomes can and will vary based on individual financial circumstances.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2510-7.