Another Cool-ish Inflation Report

The CPI rose +0.3% m/m and 2.7% y/y in Dec. The core (ex-food & energy) measure was +0.2% m/m and 2.6% y/y.

Source: Stifel as of 01.13.2026

Source: Stifel as of 01.13.2026

Details of the report:

-

- Transportation services prices were flat, despite a 1.1% decline in used car and truck prices. New vehicle prices, meanwhile, were also unchanged.

-

- Airline fares jumped 5.2%, marking the largest monthly increase since August.

-

- Shelter prices rose 0.4% with a 0.3% gain in the Owners’ Equivalent Rent (OER) in December, marking an acceleration from the 0.2% rise in October.

-

- Commodities prices increased 0.2%

-

- Medical care prices rose 0.4% in December.

-

- Apparel prices climbed 0.6% in the final month of 2025, following a 0.7% increase in October

-

- To Note: There are some caveats with the data collection process on the OER regions due to the government shutdown, although they will be corrected later this spring.

If you want more details on the specifics, get in touch!

Supercore Inflation

Supercore inflation (defined as core services, excluding housing) rose 0.3% in December, marking the largest monthly gain since September. But over the past 12 months, the index has declined from 4.05% to 2.74%. This offers some of the most compelling evidence of a significant improvement in inflation in areas escaping the direct effect of tariffs, and therefore, should be a good indication of what to expect in the year ahead, when tariff impacts fall out of the CPI and PCE.

Diffusion Index

Source: TS Lombard as of 01.13.2026

Source: TS Lombard as of 01.13.2026

Another indicator we like is the diffusion index from TS Lombard, which looks at the % of CPI sub-indexes where the 3M percent change is > 12-month percent change. This clearly shows a disinflationary trend taking hold.

Core Goods and Services YOY Prices are Moderating

The graphic below is another good visual showing the improvement in Services inflation and a “leveling off” of Goods inflation.

As shown in the last bond market update, Shelter inflation is showing similar progress. The three horsemen of inflation (Goods, Services, and Shelter) appear encouraging into 2026 as the fear of tariffs, while not entirely bypassed, appears to be much less threatening than originally anticipated.

Fannie & Freddie to Buy $200bn of MBS

President Trump has ordered Fannie Mae and Freddie Mac to purchase $200 billion in mortgage bonds. This can be viewed as another step in his determination to keep down key market interest rates and, indirectly, apply pressure to the Federal Reserve (affordability will be a key theme of winning the midterms). There are roughly $9 trillion worth of agency mortgage bonds outstanding, so if Fannie and Freddie carry out all the purchases, it would amount to just over 2% of the market. However, it’s not clear what the ultimate impact on housing affordability will be. One big concern is that if there is not an increase in the supply of homes with this new demand push from lower rates, we’re likely to see a rise in home prices that offsets the benefit of lower mortgage rates.

On another topic, the $200bn of MBS purchases are nearly identical to the annual rate of MBS rolling off the Fed’s balance sheet. This is consistent with the view that there is a push to get the Fed balance sheet lower (or at minimum predominantly Treasuries) over the next two years, but use private activity to privatize the Fed’s holdings. Financial deregulation is the center of this initiative.

One caveat to the MBS purchases is that, due to the Government-Sponsored Entities’ (GSEs) legal mandate to be duration-neutral, this means that for every $200 billion MBS duration that they buy, they need to sell $200 billion of Treasury duration, which will be concentrated in the 5-to-10-year portion of the curve. The hedging effect could hamstring the administration’s efforts to flatten the curve and keep long rates down, as there is somewhat of an offsetting transaction to the duration component of the MBS purchases. However, the Fannie and Freddie purchases will (and already have) tightened the spread between mortgage rates and Treasury yields, which certainly helps lower consumer mortgage rates.

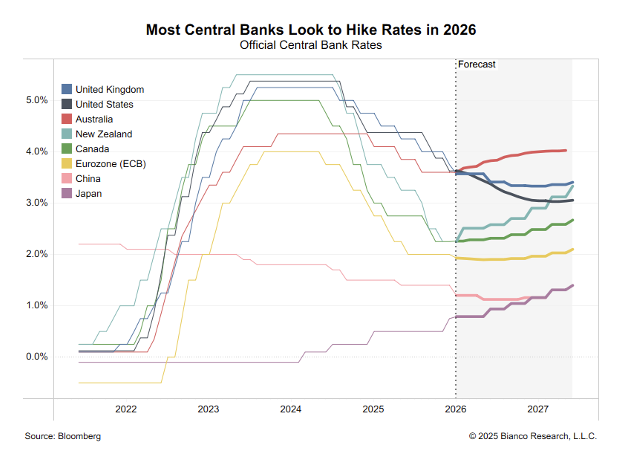

Global Rates Expected to Rise in 2026

While forecasts can be good or bad, most Central Banks across the developed world appear to have completed their cutting cycle and could flip back into a hiking mode later this year.

Source: Bianco as of 01.13.2026

Source: Bianco as of 01.13.2026

If you look at yield curves globally, yields have risen in anticipation. For instance, the Japanese 10-year yield has nearly doubled since the beginning of 2025, currently sitting at 2.15%. A similar could be said of German 10s, which are up ~50bps since the beginning of 2025, currently yielding 2.81%.

This is the opposite of the move experienced in the US, where the 10 year Treasury yield declined by ~40bps in 2025 (10yr currently yields 4.15%). Higher yields globally could pressure yields on the homefront as many foreign investors that have parked capital in US Treasuries can now find better returns at home (especially after currency hedging). Something to monitor in 2026!

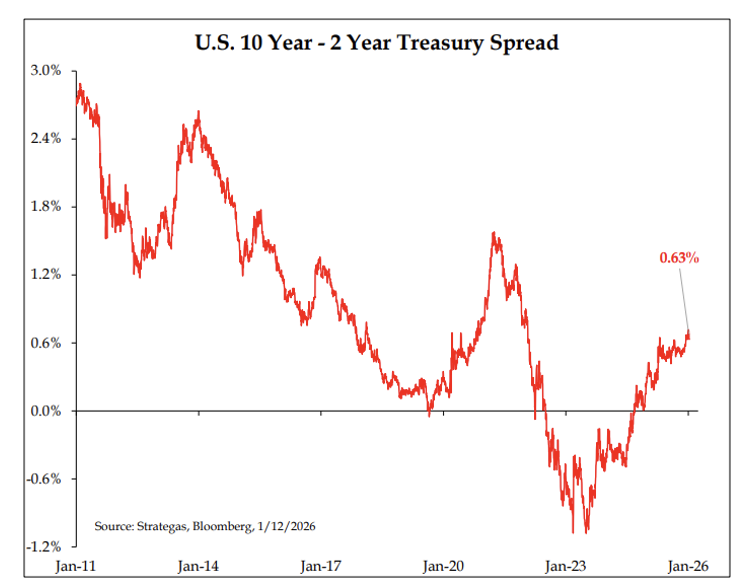

Yield Curve Continues to Steepen

The yield curve in the US has steepened drastically from the deep inversion of 2023, with markets expecting further steepening in 2026.

Source: Strategas as of 01.13.2026

Source: Strategas as of 01.13.2026

We see the following reasons that this is likely to continue:

1) Higher rates in Japan (and globally)

2) Expected economic growth improvements

3) Expected Fed rate cuts

4) Risks to Fed independence (pressuring term premiums)

A steeper yield curve on net is likely very healthy for the real economy, especially if it mostly entails the front-end declining while the long end stays the same or declines marginally (bull steepener). Many portions of the real economy (bank lending, real estate, etc.) have been negatively impacted by higher yields and an inverted yield curve. As the administration continues to focus on deregulation and the real economy, a steeper yield curve should help pass the baton to the private sector and open bank lending capacity.

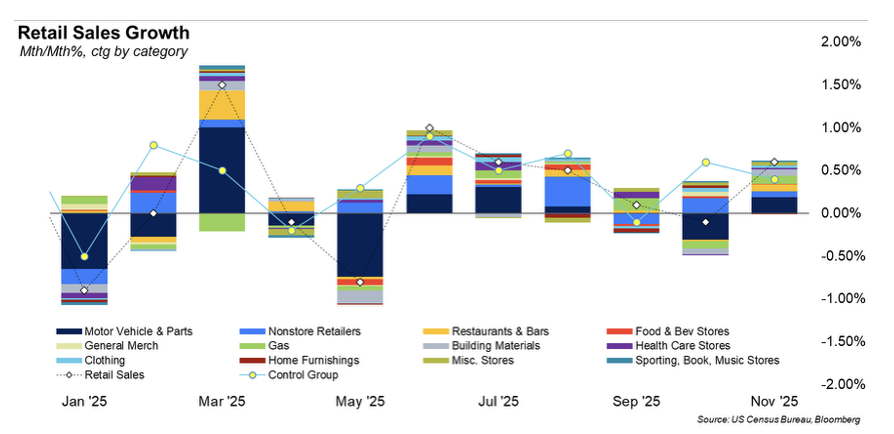

November Retail Sales Strong

The November Advance Retail Sales Report showed overall sales increased 0.6% vs. 0.4% expected, and sales ex-autos and gas rose 0.4% vs. 0.3% expected. The so-called control group, a direct GDP feed, increased 0.4%, matching expectations and providing a nice boost to fourth-quarter GDP.

Source: FHN as of 01.14.2026

Source: FHN as of 01.14.2026

In summary, another solid showing by the US consumer, albeit a bit dated due to the government shutdown. The Census Bureau has yet to confirm a date for December retail sales, but given the clues from December CPI regarding elevated prices on discretionary items like lodging and airfares, we’re going to assume it was a decent to solid month, like November.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2601-28.