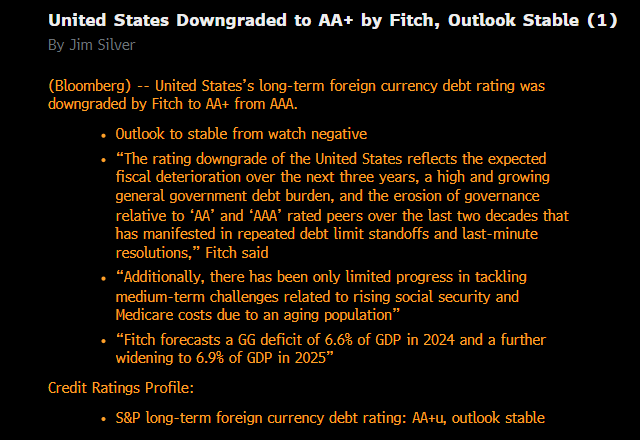

We’ve all seen the news that Fitch downgraded the US Government’s credit rating from AAA to AA+. Fitch’s move follows a similar cut by S&P about 12 years ago.

Source: Bloomberg as of 08.01.2023

Source: Bloomberg as of 08.01.2023

Moody’s continues to rate the US AAA (wonder where the lobbyist dollars are going now).

Talking Heads Highly Criticized the Downgrade

Larry Summers called it “bizarre and inept”, Jason Furman says it’s “absurd”, Mark Zandi argues it’s “off base”, Mohamed El-Erian calls it “a strange move” while Janet Yellen said, “I strongly disagree with Fitch’s decision,” adding that the change announced was “arbitrary and based on outdated data” while stressing that Treasury securities remain the world’s “preeminent safe and liquid asset.”

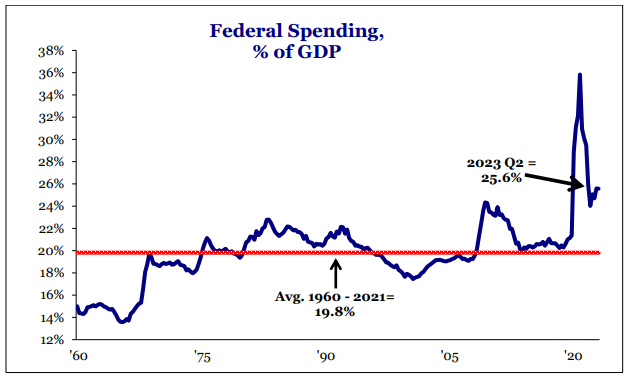

The US Government is Spending like Drunken Sailors

Source: Strategas as of 08.02.2023

Source: Strategas as of 08.02.2023

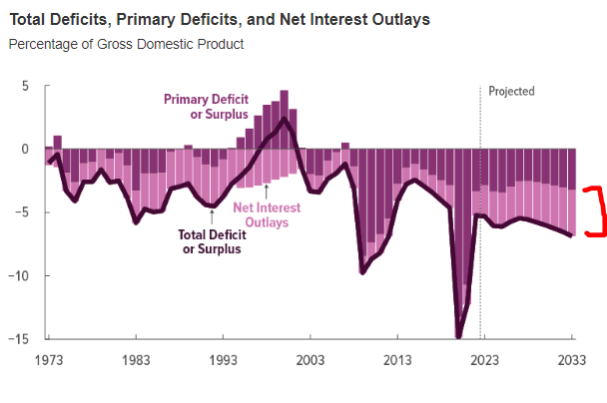

Fitch projects “general government deficits,” which include state and local governments as well as the federal government, will rise from 6.3% of GDP this year to 6.9% by 2025. We think there is a lot more upside (bigger deficits) than downside risk to this forecast. Remember the CBO assumptions from back in February?

Source: CBO as of 02.16.2023

Source: CBO as of 02.16.2023

Our Thoughts

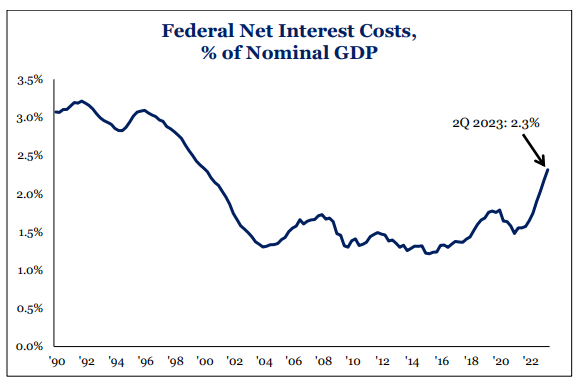

While the downgrade itself is important, the timing is what concerns us. The US has hit its fiscal inflection point of net interest costs hitting 14% of tax revenue, and debt servicing costs are rising for the first time in 35 years.

The rating agencies are not going to force austerity on the US, but we are nearing the point at which investors have historically imposed that discipline. We’ve mentioned right tail risk & bond vigilantes in recent commentary, and here we are.

Treasury Heavily Issuing on the Front End of the Curve

It appears the Treasury is doing gymnastics to raise debt, recently issuing $1 trillion of T-Bills at a 5.3% rate, when issuing debt on the long end of the curve would have been cheaper. This is all likely because the Treasury wanted to minimize liquidity disruption.

Source: Strategas as of 08.02.2023

Source: Strategas as of 08.02.2023

Taking it a step further, the Treasury is abandoning their duty of maximizing efficiency of taxpayer dollars, issuing on the front end vs. the long end despite the yield curve’s current inversion.

Federal Debt Uncomfortably High

Source: Strategas as of 08.02.2023

Source: Strategas as of 08.02.2023

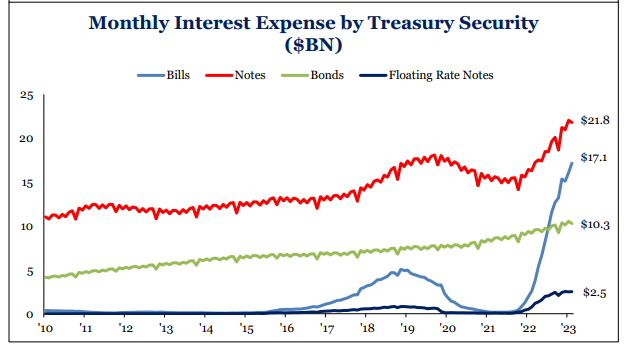

Cost of Debt is Rising

Source: Strategas as of 08.02.2023

Source: Strategas as of 08.02.2023

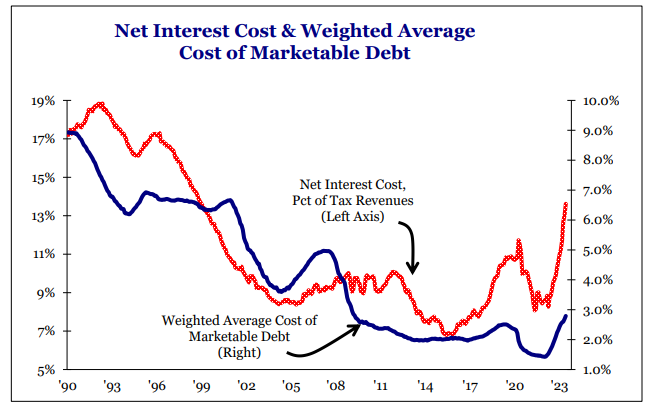

It’s just simple math that the cost of the debt, and in turn interest expense, is rising as rates rise. The one positive is it’s a slow-moving train and will take time to fully set in. In my opinion, the Treasury is hoping for enough economic weakness to attract flows to risk free assets but not enough to destroy tax receipts.

They also eventually want to cut rates to lower the interest expense burden. The ultimate question is how much longer will rates have to stay “up here” because the longer they do, the more pressure it will put on the fiscal situation.

Historically, once the US government’s net interest cost hits 14% of tax revenues (above graphic, red line on the left axis), financial markets impose austerity on policymakers. Net interest costs as a percentage of tax revenues surged in 2023, hitting the 14% number.

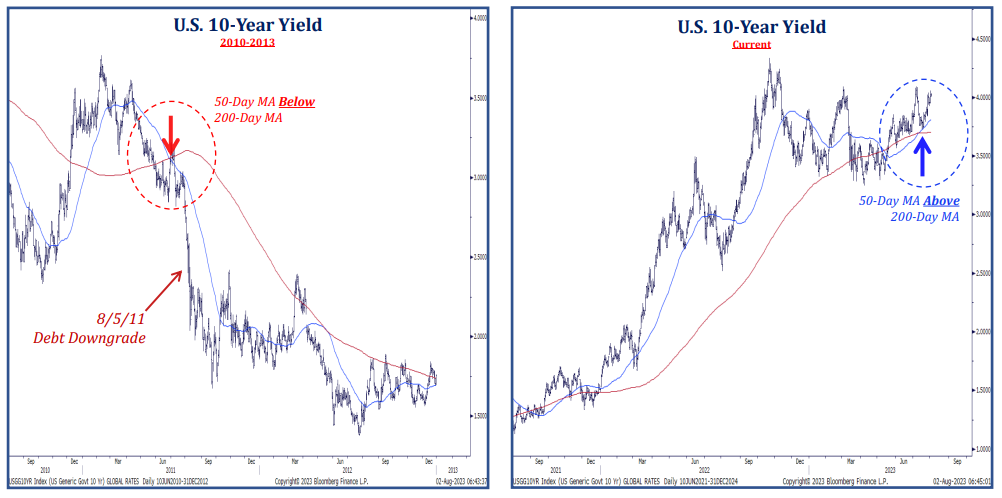

Rates Rallied After the 2011 Downgrade, What About This Time?

The trend for rates in 2011 was down and is different than the upward trend for rates today, making for a key difference between yesterday’s U.S. debt downgrade vs. August 2011.

Source: Strategas as of 08.02.2023

Source: Strategas as of 08.02.2023

Back in early 2011, yields had already peaked and were trading below the 200-day moving average and making 52-week lows at the time of the downgrade. It was a surprise to consensus, but in the direction of the trend.

Yields continued to fall sharply following the August 2011 S&P downgrade and ultimately bottomed out in mid-2012. Today it’s a different picture, 10s are flirting with cycle highs and the 50-day is above the 200-day (trend is up). It’s tempting to dust off the 2011 playbook here, but trend argues against it.

Will there be Forced Selling Due to the Downgrade?

We don’t believe there will be meaningful forced selling of Treasuries due to the downgrade. S&P downgraded the sovereign rating in 2011, and while it had a meaningfully negative impact on sentiment, there was no apparent forced selling at that time (rates actually went lower).

Because US risk-free assets are such an important asset class to the global financial system, most investment mandates refer to them specifically as “US risk-free debt”, rather than “AAA-rated government debt”.

Conclusion

We’ll leave you with a statement from a research partner, Piper Sandler’s Head Economist Andy Laperriere, who said it better than we could have ourselves:

“The United States is in the worst fiscal position in the history of the country with the possible exception of immediately after its founding. If anything, Fitch likely understates the severity of the medium-term and long-term deficits and the dysfunction of America’s political system. The leading presidential candidates in both parties have said in no uncertain terms they have no intention of addressing the nation’s long-term budget problems and their policies would make them worse. Both parties have shifted away from free-market economic policies conducive to maximizing economic growth (and being able to pay the bills). The budget process is completely broken, and neither party makes much of an effort to even try to fund the government the way mandated by law.

What’s worse, both Joe Biden and Donald Trump, the leading contenders for their respective party’s nominations, have steadfastly refused to address the nation’s long-term budget problems while President. Both promise if re-elected they won’t touch entitlements, the primary driver of higher long-term deficits. If President Biden wins re-election, he is promising to spend trillions more. And like during the last two years, he is likely to spend substantially more than he generates in tax hikes. The Democratic Party is increasingly dominated by progressives and even socialists whose policies would reduce potential GDP. The GOP is drifting away from its historical free market and limited government principles toward an ill-defined economic nationalism that is protectionist and anti-business. Even an historical great strength of the US cited by Fitch, the rule of law, is under attack in both parties. Finally, we search in vain for any evidence America’s voters are interested in an elevated conversation about addressing the nation’s long-term fiscal problems.”

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2308-4.