Flashing back a year, when bonds felt a bit more alive than dead. Originally posted in our Content Hub last March but the concepts remain important…

Rates Are Moving

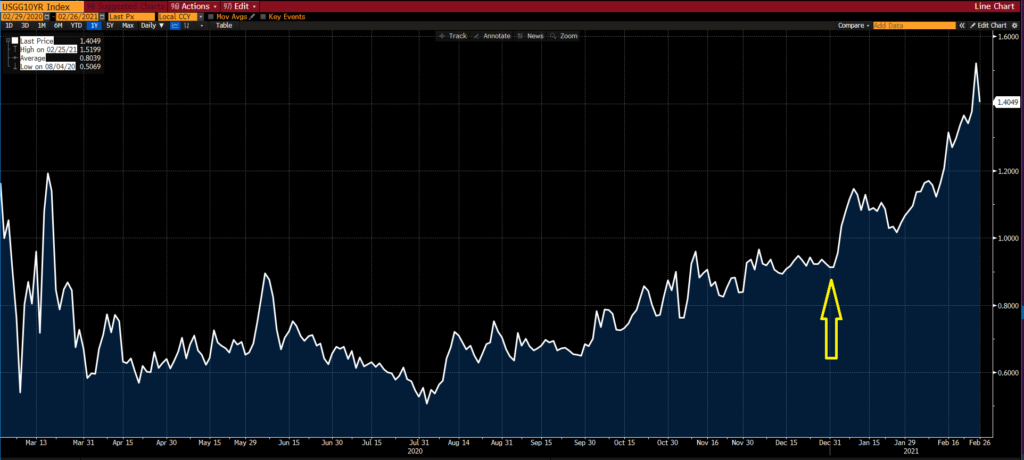

Interest rates – just look at what the yield (the interest rate) of 10-year government bonds has done recently. The arrow is pointing to the start of 2021, starting below 1% and spiking over 1.5%.

Source: Bloomberg. Data as of 02.26.2021

Bond prices and interest rates carry an inverse relationship. Meaning, when rates go up, bond prices go down. Take a look at the table below showing total return of three types of bonds: Corporate bonds (LQD), the aggregate bond market (AGG), and long-term treasury bonds (TLT) have struggled year to date.

Source: Bloomberg

Bonds rely on these simple things to generate returns:

- Yield – the interest a bond pays.

- Interest rates falling – this lifts the market price of a bond

Yes, we’re ignoring credit here, but want to make a point. Both #1 and #2 seemingly offer little to be excited about. Despite the recent rise in rates, we are still looking at historically low rates across the board. This translates to minimal yield on bonds. Given that, the potential positive contribution of rates dropping lower to bond prices is not all that great.

Anybody that knows us has heard us screaming about this environment. The drag of traditional bonds on investors’ portfolios is real. We said it throughout 2020, we thought 2021 was shaping up to be negative return year for the AGG.

There is a chance that this rise in rates is just getting started. Knowing that, we are considering the current and potential impact on stocks.

Growth vs Value Stocks

We still see the path of least resistance being up for stocks, with two key drivers:

- The amount of monetary and fiscal stimulus in the markets could act as a buoy for the equity markets.

- Relative opportunity set is still heavily skewed towards stocks. If the 10-year yield gets high enough, this point may change, but until then, the best-looking option for dry powder is still the equity markets.

We do believe growth stocks will be impacted by rising rates differently. Why?

The stock price of a company is simply the value of future cash flows discounted using some rate. Think about the math of that…a series of cash flows that extends way out into the future (the numerators), divided by an interest rate (the denominator), is a simple formula for discounting future cash flows back to today to give us a price.

For simplicity and to hammer home the next point – let us take one future cash flow of $100 coming to us in 10 years, and discount it back to today. Let us do this twice…first using 0.50% as our denominator, and secondly using 5.00%.

Using 0.50%, today’s value of that future cash flow is roughly $95.13.

Using 5.0%, today’s value would be roughly $61.39.

Hopefully, our point is jumping out at you. The rate used to discount these cash flows is incredibly important.

The lower the discount rate, the higher the value attributed TODAY to future cash flows of TOMORROW – and vice versa.

Considering that arithmetic again, think about the market we have been in. It has been dominated by growth stocks. These are stocks that trade at premium valuations. Some have fast-growing business that are expected to produce more and more income. Some have really cool concepts with no income at all (see our Greg Oden post). Either way, the market has valued future cash flows for these names at insanely low rates (some may say artificially low) which has translated to high valuations.

Considering that arithmetic again, think about value stocks in the market we have had. They have been demolished by growth stocks to a point that value investors can look pretty foolish not to jump on the bandwagon of these high-flying companies.

Rising rates should impact growth more negatively than value. We are seeing that play out as the QQQ’s are lagging the SPY in recent months. In addition, we’ve seen a few more ‘growthy’ names come out with incredible earnings reports that the market has not treated favorably.

What We Are Watching

Rising rates are a concern as they could rise to a point that impacts markets everywhere.

The 10-year US Treasury Note’s recent run has a component of rising inflation expectations. The Fed has said they would let inflation run a little hot, but it’s not something they want to get out of hand. Remember, their mandates are a) low unemployment and b) low inflation.

We are paying close attention to the difference between the 10-year and 2-year Treasuries’ yield. The Fed is fully in control of the short end (the 2 year) now, and they are pegged about as low as they can go. The market is controlling the 10-year more and more, and you see what it’s doing.

The difference in yield, and rising inflation, could lead to the Fed losing control to the market. If markets begin to lift the short end of the curve (2 year), it could be the catalyst for the Fed to tighten (raise rates). Equity markets may not love that.

Will it happen…who knows, but we are paying attention. Either way, we still don’t want to own bonds and will take our over-allocation to stocks with a nice dose of long volatility for protection.

As always, thank you for your trust.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2204-17.