Developments over the Past Month:

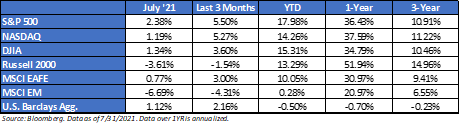

- Stocks continue to see the path of least resistance being up. For the sixth time this year, the S&P 500 bounced off its 50-day moving average. Still, year-to-date, the market has not seen a decline greater than 5.0%.

- Year-to-date, the 10-Yr Treasury yields have marched higher (0.93% on 12/31/2020), though took a breather over the last four months, continuing to drive daily movements in the market, and closed the month much lower around the 1.25% level.

- The Fed promised that rates would remain in the 0% – 0.25% range through 2023, with the goal of stoking inflation to moderately exceed 2% for some time. Fed Chair Powell seemed more dovish in the July press conference vs. the relatively hawkish committee projections. He opened the door to a discussion on QE tapering, but noted that the U.S. is still not at the “substantial further progress” standard that would allow policy normalization. It doesn’t appear that they are worried about the Delta variant at the moment. The Fed dots (forecasts for future fed funds) rose from the zero bound in 2023, but Powell noted that there is a large amount of uncertainty over the next 2 years.

- 5-YR Breakevens (market estimated inflation over the next five years) is 2.10%, well below its highs, but above the Fed’s desired 2% threshold. Remember, Powell said the Federal Reserve would let this run hot for a bit, i.e., above 2%. Ultimately, the yield curve is pricing in higher inflation expectations. However, we believe that the market is pricing in a normalization of rates, as the U.S. remains the only country still below its pre-COVID 10-Yr interest rate level.

- The G-7 made an agreement to impose a minimum tax deal on multinationals of 15%. This deal is being pushed by Treasury Secretary Janet Yellen. Implementation though is no guarantee. We expect other countries will simply wait and let the U.S. take the lead. In summary, we believe the odds of a tax hike occurring this year have substantially declined since April.

- Jobs data, much like all the current economic data, continues to be mixed. The market will get more clarity when all of the unemployment benefits roll off and we see schools starting to reopen.

- Infrastructure Bill – As of writing this, we are almost there. Bipartisan negotiators announced an agreement on the details of their $1.2 trillion bipartisan infrastructure bill, which includes $548 billion of new spending. The bill must go through the House and the Senate – Nancy Pelosi is still lobbying for a larger $3.2T bill. It looks like we are still a month away before something gets finalized. I believe that Washington tends to overpromise and underdeliver.

- From our perspective, earnings season for Q2 2021 has been strong to quite strong. The overall S&P 500 earnings growth rate jumped to 72.3% from 46.3% for the first quarter. All eleven sectors saw earnings growth strengthen, with energy growth flipping positive. From a top-line perspective, revenues have climbed +19% YoY.

- 2019 S&P 500 operating earnings = $165. Bottoms-up for 2020 = $142 (was as low as $125 in June). 2021 = $197!

- S&P 500 fwd. P/E is at 22x. CAPE Ratio is 35x. EAFE is 16x forward P/E, while EM is at 13x. Russell 1000 Value is 17x v. 1000 Growth at 31x.

Client Talking Points – August 2021

- President Biden outlined the biggest expansion of the federal government matched with the largest tax increase since 1968. Biden senses the post-COVID era is a once-in-a-generation opportunity to massively restructure US fiscal, monetary, and social policy. In our opinion, this is a big experiment. We’ll wait to see how infrastructure and taxes pan out.

- We have expected bond yields to reflate as the pandemic improves and economic activity begins to normalize. The spread on the 2s and 10s has historically expanded as wide as 300 bps (~100bps as of July month-end)

- Thanks to continued vaccine developments, we believe that there is light at the end of the tunnel, and markets are pricing in a recovery in 2021 propelled by low interest rates. Still, we believe that the best fiscal stimulus the economy can have is an open economy.

- This is not a normal economic cycle, which is caused by financial excesses. This may help explain the stealth recovery in asset prices (along with the Fed flooding the markets with liquidity).

- Should a successful vaccine allow for the resumption of normal economic activity, our expectation is that rates will continue to rise, and market leadership will shift away from Tech Growth into more downtrodden components of the market.

- We feel it will be worth watching the general trend of economic and fundamental data, and when it will begin to decelerate. It’s tough to get better than the best. Are we already at peak growth, and what happens after peak growth?

- Longer-term, we believe valuations and bond yields will eventually matter, and both will lower expected returns for balanced portfolios.

Disclosures

Aptus Capital Advisors, LLC is a Registered Investment Advisor (RIA) registered with the Securities and Exchange Commission and is headquartered in Fairhope, Alabama. Registration does not imply a certain level of skill or training. For more information about our firm, or to receive a copy of our disclosure Form ADV and Privacy Policy call (251) 517-7198 or contact us here. Information presented on this site is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy.

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 11.2 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 4.6 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security’s U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities.

The Dow Jones Industrial Average® (The Dow®), is a price-weighted measure of 30 U.S. blue-chip companies. The index covers all industries except transportation and utilities.

The Russell 2000® Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000® is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries*around the world, excluding the US and Canada. With 902 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 Emerging Markets (EM) countries*. With 1,387 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities and collateralized mortgage-backed securities. ACA-2108-1.